Definition & Meaning

Form 1042-S, known as the "Foreign Person's U.S. Source Income Subject to Withholding," is a critical document used by the IRS to report the amount of income nonresident aliens or foreign entities receive from U.S. sources. The form includes details about the type of income, applicable tax rates, and withholding details. It serves as a bridge in tax compliance between foreign income recipients and the U.S. tax system, ensuring that the correct amount of tax is withheld at the source for foreign earners.

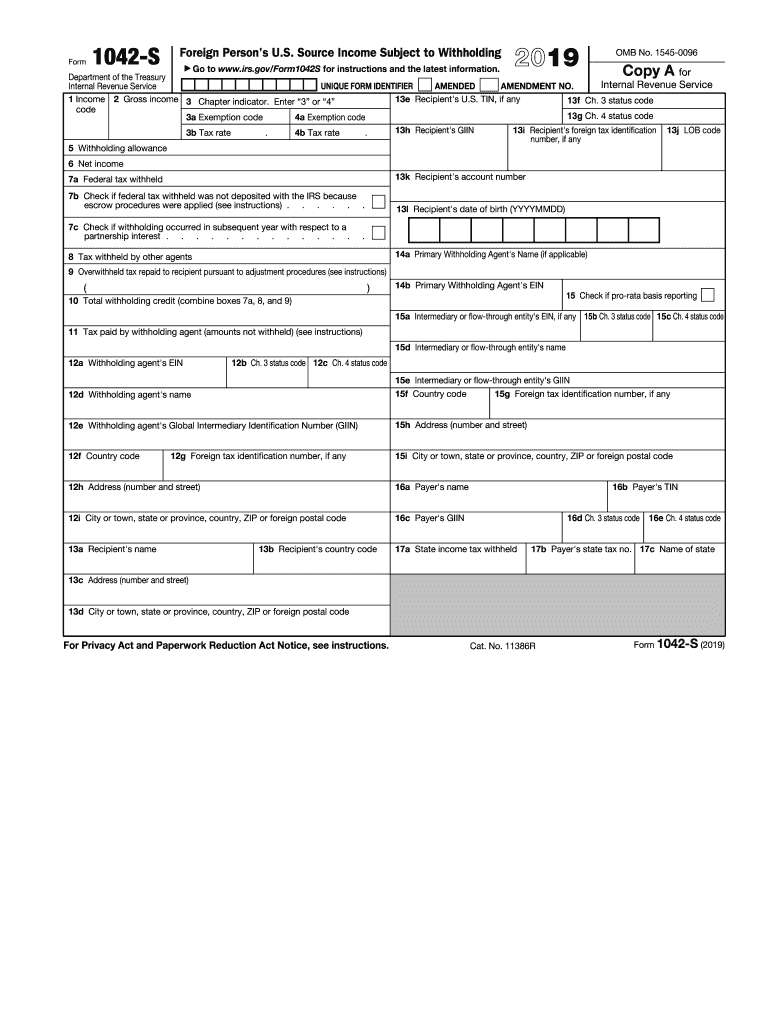

Steps to Complete the 1042

- Gather Necessary Information: Start by collecting all relevant data, such as personal identification numbers, beneficiary details, and income amounts from U.S. sources.

- Determine Income Type: Identify the type of income, such as dividends, interest, or royalty, and select the corresponding income codes.

- Calculate Withholding Tax: Use the correct tax rate, taking into account any tax treaties that might alter the standard rates.

- Fill In Part I: Provide personal information, including name, foreign taxpayer identification number, and address.

- Complete Part II: Detail the income source and type, including any applicable exemptions or treaty benefits.

- Sign and Submit: Ensure all sections are correctly filled, signed by an authorized person, and submitted to the IRS by the due date, typically March 15.

Important Terms Related to 1042

- Withholding Agent: The person or entity responsible for withholding taxes on U.S. source income paid to foreign persons.

- Beneficial Owner: The person who ultimately owns or has rights to the income, regardless of who receives the payment.

- Income Code: A numeric or alphanumeric code that identifies the specific type of income reported on the form.

- Chapter 3 and Chapter 4 Statuses: Designations that pertain to compliance with specific IRS and FATCA (Foreign Account Tax Compliance Act) requirements.

IRS Guidelines

The IRS provides comprehensive instructions for completing Form 1042-S, specifying how withholding agents report income, exemptions, and withheld amounts. It highlights the necessity to differentiate between various types of income and applicable tax treaties. The guidelines stress accuracy and completeness to avoid penalties, and they outline procedures for electronically submitting the form through the FIRE (Filing Information Returns Electronically) system if filing 250 or more forms.

Filing Deadlines / Important Dates

Form 1042-S is due to be submitted to the IRS by March 15 each year, aligning with the reporting of income paid in the previous calendar year. Relevant withholding amounts must be deposited following the IRS’s semi-weekly or monthly deposit schedules to prevent late payment penalties. Inaccurate or late submissions can lead to significant fines, so it is imperative to adhere strictly to these deadlines.

Legally Binding Electronic Signatures

Compliance with IRS requirements allows Form 1042-S to be completed using legally binding electronic signatures, making digital submissions a viable option. The ESIGN Act ensures that electronic signatures have the same legal standing as handwritten signatures, provided they meet specific criteria such as identification of the signer and an electronic consent agreement.

Software Compatibility

Numerous software solutions, like TurboTax and QuickBooks, support the completion and submission of Form 1042-S. These platforms often offer step-by-step guidance, built-in tax calculation tools, and electronic filing capabilities that streamline the process. Choosing compatible software ensures effortless integration of financial data, which is crucial for timely and accurate form submission.

Penalties for Non-Compliance

Failing to file Form 1042-S or incorrectly reporting information can result in penalties from the IRS. These fines can be substantial, scaling up based on the delay duration and the total income involved. Additionally, withholding agents might face increased scrutiny, which can affect relationships with foreign beneficiaries. It is crucial to understand these implications and ensure that compliance with all reporting obligations is met to avoid financial repercussions.

Who Typically Uses the 1042

Form 1042-S is typically used by withholding agents such as financial institutions, corporations, insurance companies, and other entities that process payments to foreign individuals or businesses. Nonresident aliens with U.S. income interests, including students, athletes, artists, or foreign shareholders of U.S. companies, also rely on this form to document their income and tax withholdings when filing taxes in the U.S.