Definition & Meaning

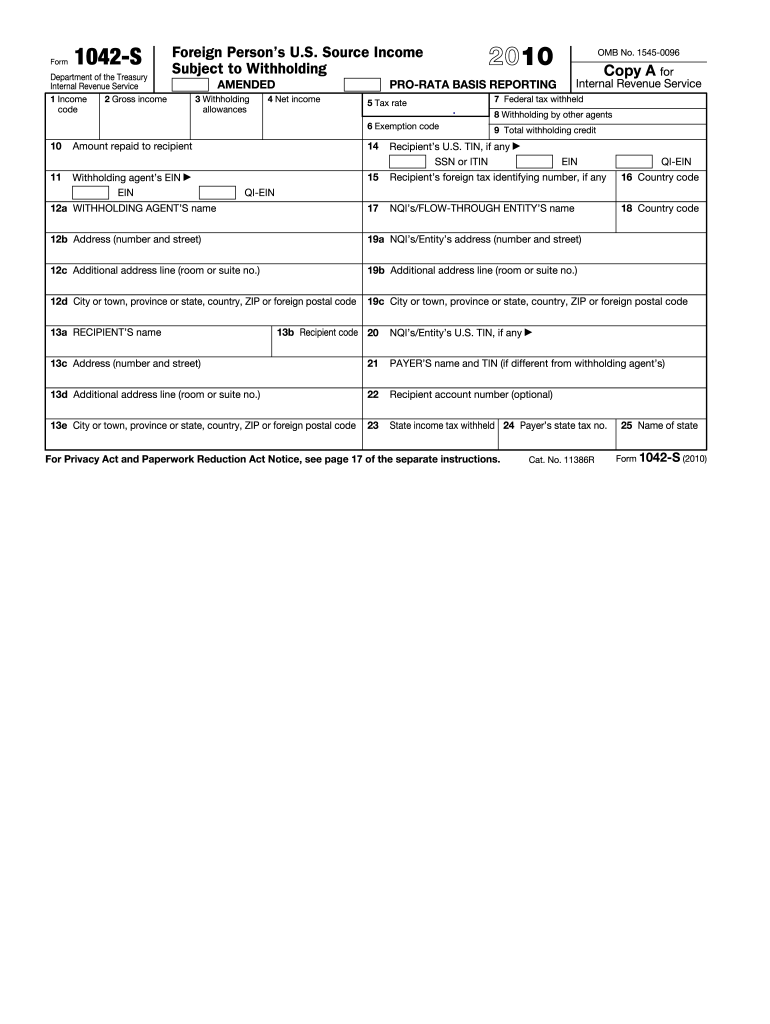

Form 1042-S is a reporting form used by the Internal Revenue Service (IRS) to document U.S. source income paid to foreign individuals and entities that are subject to withholding. This form is primarily used by nonresident aliens and foreign corporations that have earned income from U.S. sources, such as dividends, interest, and royalties. It outlines key details about the income received, including the tax withheld and the basis for withholding. The form is essential for both the payer, often a U.S.-based company or financial institution, and the payee, ensuring compliance with tax regulations related to reporting foreign income.

How to Use the 2010 Form 1042-S

Using the 2010 Form 1042-S involves several steps:

-

Reviewing the pre-filled form: Individuals or entities who receive Form 1042-S should first verify that all pre-filled information is accurate. This includes checking details such as the income amount, the withholding rate, and the payer identification details.

-

Understanding form sections: Familiarize yourself with the different sections of the form, which include income code descriptions, exemption codes, and details on tax treaty benefits if applicable.

-

Filing with taxes: Use the details from Form 1042-S when filing your tax return to ensure proper credit for withheld taxes. The form must be attached to your U.S. tax return for it to be processed accurately.

-

Retaining for records: Keep a copy of the form for your personal records as it can be essential for future tax audits or compliance queries.

The form is designed to streamline the reporting process for foreign income, reducing errors and ensuring correct reporting for tax purposes.

Steps to Complete the 2010 Form 1042-S

Filing the 2010 Form 1042-S involves several critical steps:

-

Identify the Payer: Begin by completing the payer’s details, which is usually the U.S. entity that made the payment. This includes the Taxpayer Identification Number (TIN) and address.

-

Input Recipient Information: Enter details of the recipient, which typically includes their name, address, and identifying number.

-

Report Income Amounts: Specify the income amount paid and the type, using appropriate income codes as per IRS guidelines.

-

Specify Tax Withheld: Enter the amount of tax withheld on the income and any applicable exemptions using IRS codes.

-

Check for Treaty Benefits: If the recipient is eligible for any income tax treaty benefits, ensure these are correctly applied and documented on the form.

-

Sign and Date: The form must be signed by an authorized person to validate it. Ensure all the data entered is accurate to prevent issues with IRS compliance.

These steps are crucial for accurate reporting of foreign income and for meeting the IRS’s compliance requirements.

Important Terms Related to 2010 Form 1042-S

Familiarity with certain terms is essential when dealing with Form 1042-S:

-

Nonresident Alien: An individual who is not a U.S. citizen or resident and who has income from U.S. sources subject to taxation.

-

Withholding Tax: The amount withheld from the payment made to a foreign entity, reflecting the taxes owed to the IRS.

-

Income Codes: These codes specify the type of income received, such as dividends or interest, and are essential for correct form completion.

-

Exemption Codes: Codes that signify why certain incomes may not be subject to withholding, often due to treaty provisions.

Understanding these terms helps ensure the form is completed accurately, avoiding potential compliance issues.

Who Typically Uses the 2010 Form 1042-S

The primary users of Form 1042-S include:

-

Foreign Individuals: Nonresident aliens earning income from U.S. sources need this form to report their earnings and taxes.

-

Foreign Corporations: Entities with U.S. source income are required to use this form to disclose earnings and taxes paid.

-

U.S. Payers: Entities like banks or corporations that make payments to foreign entities must generate this form to comply with withholding tax regulations.

-

Tax Preparation Professionals: Accountants or tax advisors dealing with international clients often handle these forms to ensure compliance and accurate tax filings.

These groups rely on Form 1042-S to manage and report U.S. source income effectively.

IRS Guidelines

The IRS provides specific guidelines for completing Form 1042-S, including:

-

Instructions for Payers: Details tasks like calculating withholding, completing form sections, and adhering to reporting deadlines.

-

Filing Requirements: Stipulations about who must file the form, and under what conditions filing is necessary.

-

Publication 515: A comprehensive IRS guide offering detailed explanations of withholding of tax on nonresident aliens and foreign entities.

These guidelines help ensure compliance and reduce errors when handling international income reporting.

Filing Deadlines / Important Dates

Key deadlines for Form 1042-S include:

-

Payment Year: Forms must be completed for all payments made during the calendar year.

-

Due Date to Recipients: The form must be furnished to the recipient by March 15 of the following year.

-

IRS Submission Deadline: Generally, the form must be submitted to the IRS by March 31 if filing electronically or by the same date if filing a paper version.

Missing these deadlines can result in penalties, so proper scheduling and preparation are crucial.

Required Documents

Completing Form 1042-S necessitates several documents:

-

Form W-8 Series: These forms establish the recipient's foreign status and eligibility for reduced withholding under tax treaties.

-

Income Documentation: Records showing payments made and withholding taxes held.

-

Tax Treaty Documents: If applicable, these verify eligibility for reduced withholding rates based on international agreements.

Assembling these documents ensures accurate and efficient form processing.