Definition & Meaning

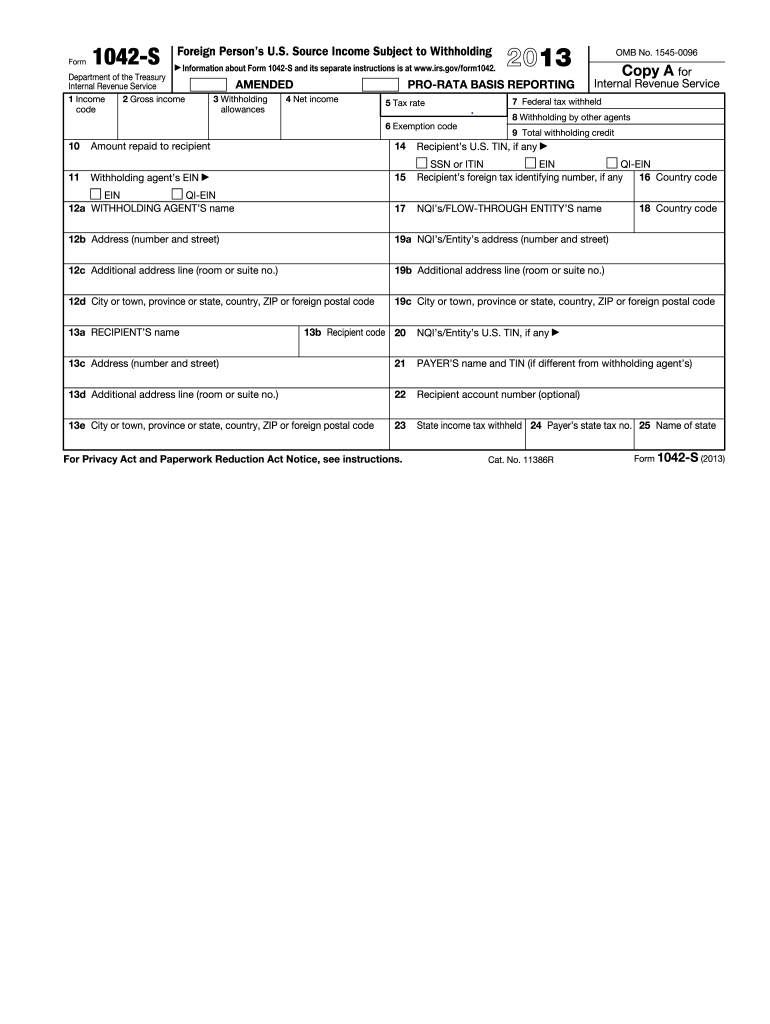

The 2013 Form 1042 is used by the Internal Revenue Service (IRS) to document withholding tax on U.S. source income paid to foreign persons. This form is crucial for ensuring compliance with U.S. tax laws, capturing information on income types, applicable tax rates, and withholding amounts. Unlike other IRS forms, Form 1042 specifically addresses tax responsibilities related to foreign individuals or entities receiving income from U.S. sources. By utilizing this form, taxpayers help the IRS maintain accurate records of international income and taxation.

How to Use the 2013 Form 1042

Using Form 1042 involves several detailed steps. The primary purpose is to report any U.S. source income paid to foreign entities or individuals subject to withholding tax. Here is a general procedure:

- Identify all foreign persons who received U.S. source income during the tax year.

- Determine the amount of income each individual or entity received, noting any applicable treaty exemptions.

- Calculate the withholding tax required based on the specific income type and recipient.

- Complete the form by entering the information accurately in designated sections, including withholding amounts and total income.

- Submit the completed form to the IRS, ensuring that all required supplemental documents are attached.

Steps to Complete the 2013 Form 1042

Completing the 2013 Form 1042 correctly ensures compliance and minimizes errors. Follow these steps:

- Gather Necessary Information:

- Collect details of all income paid to foreign persons, including amounts, recipient information, and applicable tax rates.

- Enter Income Details:

- Fill in the total gross income subject to withholding, recording each recipient's details and the corresponding income amounts.

- Calculate Withholding:

- Apply the appropriate tax rates, considering any treaty provisions that may reduce withholding liabilities.

- Add Supplemental Information:

- Include any additional forms required, such as Form 1042-S for each recipient.

- Review and Submit:

- Carefully check all entries for accuracy and completeness before sending to the IRS.

Important Terms Related to 2013 Form 1042

Understanding specific terminology related to Form 1042 can aid in accurate preparation:

- Withholding Agent: This is the entity responsible for filing Form 1042 and withholding taxes on U.S. source income paid to foreign persons.

- U.S. Source Income: Any income derived from activities within the United States, including interest, dividends, rents, and royalties.

- Effective Tax Rate: This is the rate at which withholding applies, which can vary based on tax treaties and specific income types.

Key Elements of the 2013 Form 1042

Form 1042 is composed of several critical sections:

- Payer Information: The details of the withholding agent or payer, including identification numbers and contact information.

- Aggregate Gross Income: Total U.S. source income subject to withholding.

- Withholding Tax Information: The specific withholding amounts calculated for each foreign entity or individual.

- Recipient Data: Details of each recipient, including names, addresses, and taxpayer identification numbers.

Filing Deadlines / Important Dates

Timely filing of Form 1042 is essential:

- Annual Due Date: The form is typically due on March 15 following the close of the tax year for which the withholding was made.

- Extensions: In certain cases, a withholding agent may request an extension using Form 7004, which must be submitted before the original due date.

Penalties for Non-Compliance

Failure to properly file Form 1042 can result in penalties:

- Late Filing Penalty: A percentage of the unpaid tax for each month the form is late, up to a maximum penalty.

- Failure to Withhold: Additional penalties apply if taxes were not withheld accurately or timely from payments to foreign persons.

IRS Guidelines

The IRS provides specific guidelines for Form 1042:

- Instructions for Form 1042: Detailed instructions are available to aid taxpayers in properly completing the form, explaining terms, and calculating taxes.

- Publication 515 (Withholding of Tax on Nonresident Aliens and Foreign Entities): This publication offers comprehensive support, including information on treaty benefits and withholding requirements.

By understanding the purpose and requirements of the 2013 Form 1042, individuals and businesses can ensure compliance with U.S. tax laws while effectively managing obligations related to foreign income and withholding.