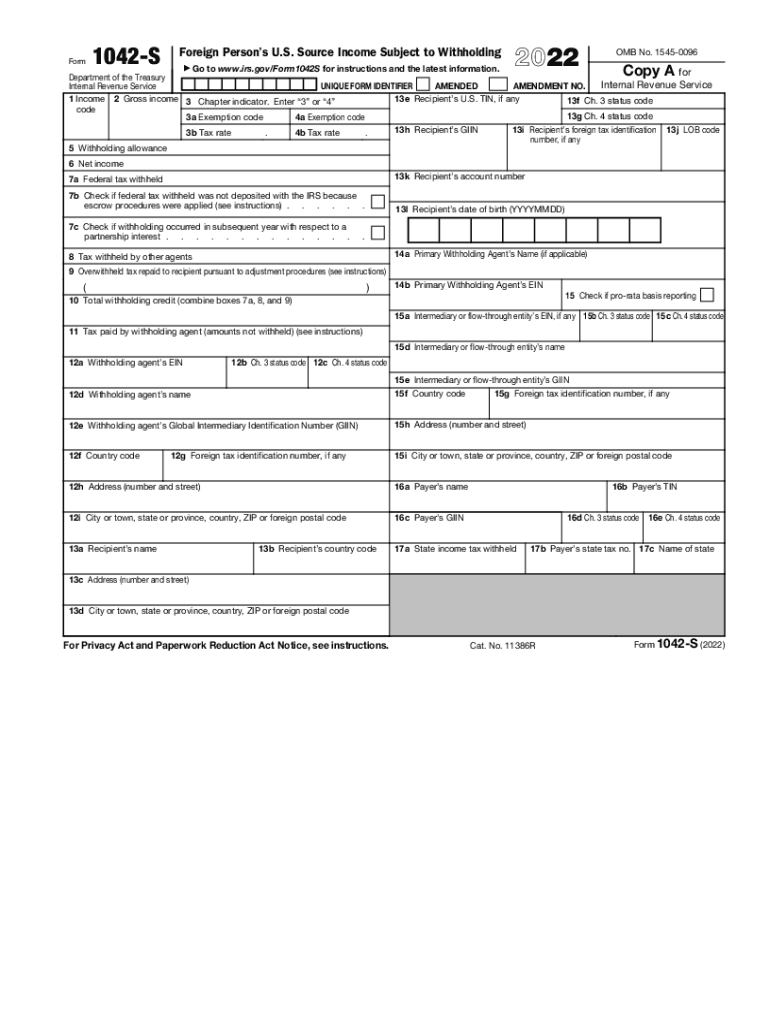

Definition and Purpose of Form 1042-S

Form 1042-S, officially named "Foreign Person's U.S. Source Income Subject to Withholding," is used to report income paid to nonresident aliens and foreign entities subject to tax withholding. This form is an essential part of U.S. tax compliance for foreign individuals and organizations earning income in the United States. Key details reported on the form include income types, tax rates, and withholding amounts. Understanding the form's purpose ensures accurate reporting and compliance with U.S. tax laws.

Steps to Complete Form 1042-S

Completing Form 1042-S involves several specific steps:

- Gather Required Information: Collect information about the income recipient, including name, address, and taxpayer identification number.

- Identify Income Types: Specify the types of income paid, such as interest, dividends, royalties, or services rendered.

- Calculate Withholding Taxes: Determine the correct withholding rate and calculate the enforced tax amount.

- Fill Out the Form Sections: Enter the recipient's details, income amounts, and withholding data accurately on the form.

- Review for Accuracy: Double-check all information for precision to prevent errors or potential compliance issues.

This process ensures the form is completed correctly and submits accurate information to the IRS.

Who Typically Uses Form 1042-S

Form 1042-S is primarily utilized by two groups:

- Withholding Agents: Organizations or individuals responsible for withholding taxes on behalf of foreign persons. Examples include banks, financial institutions, and businesses with foreign contractors.

- Nonresident Aliens and Foreign Entities: Those receiving U.S. source income subject to withholding must be aware of how the form reports their income for tax purposes.

Each party plays a crucial role in the proper execution and filing of the form, ensuring that all withholdings are documented and reported to the IRS.

How to Obtain Form 1042-S

Obtaining Form 1042-S can be done through several methods:

- IRS Website: The form can be downloaded directly from the Internal Revenue Service's official website.

- Tax Software: Many tax preparation programs offer the form and guide users through its completion.

- Professional Tax Advisors: Tax professionals can provide assistance and access to the form, especially if specific guidance is required.

These options offer flexibility in sourcing the form, depending on individual needs and familiarity with tax-related processes.

Filing Deadlines and Important Dates for Form 1042-S

Timely submission of Form 1042-S is critical to avoid penalties. Key dates to remember include:

- March 15: The deadline for submitting the form to the IRS and furnishing a copy to the income recipient.

- Extensions: An extension request can be filed if additional time is needed, but this must be done before the original deadline.

Adhering to these deadlines ensures compliance and avoids the risk of late submission penalties.

IRS Guidelines for Form 1042-S

The IRS provides specific guidelines to ensure the form's proper handling:

- Instructions: Detailed instructions are available on the IRS website, clarifying each segment of the form.

- Tax Tables: Withholding rates and applicable tax treaties are detailed in IRS publications, which should be consulted to ensure accuracy.

- Amendments: If errors are discovered post-filing, amendments must be submitted promptly to correct the discrepancies.

These guidelines assist in maintaining accurate and compliant filings.

Penalties for Non-Compliance with Form 1042-S

Failure to properly file Form 1042-S can result in significant penalties, including:

- Monetary Fines: Incorrect filing or late submission can result in fines per form, which can add up significantly for bulk filings.

- Legal Consequences: Non-compliance can lead to further legal scrutiny and potential investigation by the IRS.

Understanding these penalties emphasizes the importance of adherence to tax regulations and prompts diligence in form preparation and submission.

Key Elements of Form 1042-S

Form 1042-S contains several crucial elements that must be accurately filled, including:

- Recipient’s Information: Name, country, and taxpayer identification number are essential.

- Income Codes: Specific codes that categorize the type of income reported.

- Withholding Data: Amount withheld and the relevant tax rates.

Ensuring these elements are correctly completed is fundamental for accurate tax reporting and maintaining compliance with U.S. tax laws.