Definition and Meaning

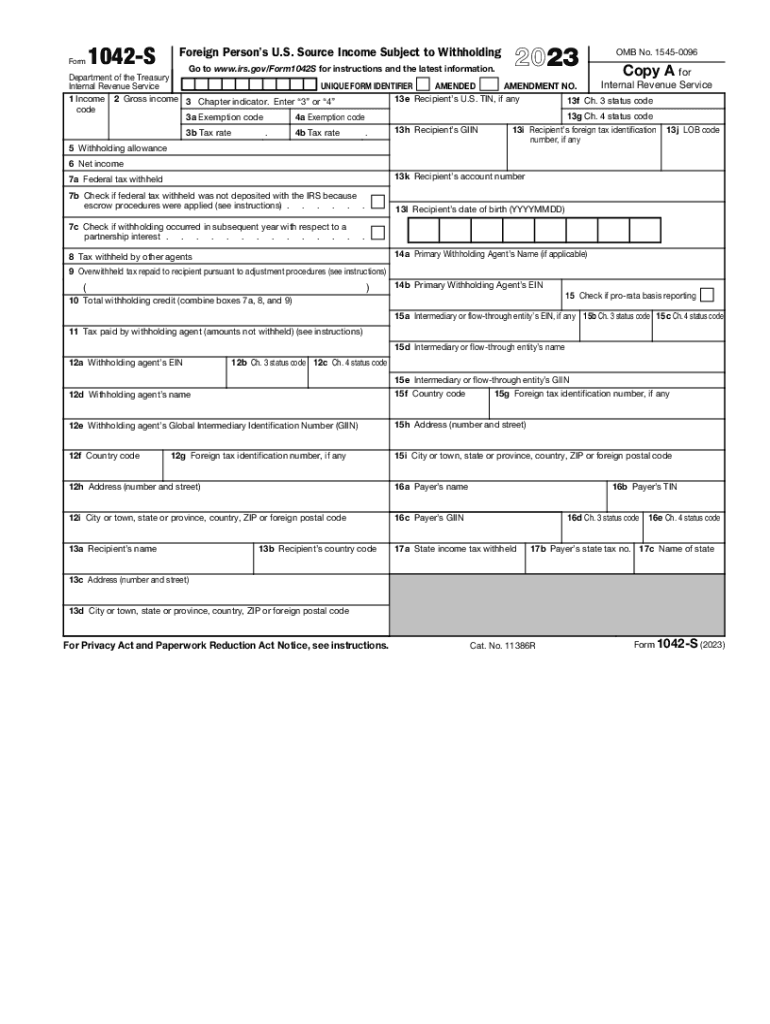

Form 1042, Annual Withholding Tax Return for U.S. Source Income, is a tax document required for reporting U.S. source income subject to withholding tax for foreign persons, including nonresident aliens and foreign corporations. It is crucial for compliance with U.S. tax regulations concerning income paid to foreign entities. The form outlines income amounts, withholding tax rates, and payment details to ensure accurate reporting and withholding.

Examples include payments such as interest, dividends, and royalties made to foreign entities. This form is essential for withholding agents, including businesses and financial institutions, to report amounts withheld on such payments.

Steps to Complete Form 1042

Completing Form 1042 involves several detailed steps. Below is a guide to ensure accurate and compliant submission:

-

Identify U.S. Source Income: Determine the types of income that are U.S. sourced and subject to withholding tax. This includes examining payments such as dividends, interest, rents, and royalties.

-

Determine Withholding Agent: The entity responsible for withholding and reporting the tax, usually the payer of the income, is the withholding agent.

-

Calculate Withholding Tax: Apply the correct withholding rate based on the type of income and any applicable tax treaties that may reduce the standard withholding percentage.

-

Complete Part I: Provide details about the withholding agent, including name, address, and EIN (Employer Identification Number).

-

Complete Part II: Detail total income subject to withholding and the total U.S. tax withheld.

-

Review for Accuracy: Double-check all entries, calculations, and eligibility for reduced withholding under any applicable treaties.

-

Submit Form: File the form with the IRS by the due date, which is generally March 15 following the end of the calendar year for which the return is being filed.

Filing Deadlines and Important Dates

Form 1042 must be filed annually, with a typical due date of March 15 for the previous tax year. If the due date falls on a weekend or holiday, the deadline moves to the next business day. Failure to meet this deadline may result in penalties.

Additionally, quarterly payments of withheld taxes are expected at specific intervals throughout the year. Keeping track of these dates is crucial for avoiding penalties and interest charges.

Who Typically Uses Form 1042

The primary users of Form 1042 are withholding agents in the United States, including financial institutions, corporations, and partnerships, which make payments to foreign persons. Specifically, entities involved in transactions that involve U.S. source income paid to nonresident aliens or foreign businesses must use this form for tax reporting.

For instance, a U.S. corporation paying royalties to a foreign entity for the use of a trademark would be required to file Form 1042 to report and remit the corresponding withholding tax.

IRS Guidelines for Form 1042

The IRS provides comprehensive guidelines to assist in the correct completion of Form 1042. These include instructions on determining U.S. source income, applying the appropriate withholding rates, and identifying eligible tax treaty benefits that may reduce withholding obligations. Essential IRS publications related to Form 1042 include Publication 515, "Withholding of Tax on Nonresident Aliens and Foreign Entities."

Consulting these materials is vital for withholding agents to ensure compliance and accuracy in their filings.

Penalties for Non-Compliance

Failing to file Form 1042 accurately and on time can result in significant penalties. The IRS imposes fines for late filing and underpayment of taxes withheld. Penalties depend on the duration of the delay and the amount of tax underreported or underpaid.

For example, the penalty for failing to file the form on time without reasonable cause is typically calculated based on a percentage of the tax due, which can escalate the longer the delay continues.

Important Terms Related to Form 1042

Understanding key terms is essential for accurately completing Form 1042. Important terminology includes:

- Withholding Agent: The person or entity responsible for withholding tax on payments and reporting them to the IRS.

- Nonresident Alien: An individual who is not a U.S. citizen or resident alien.

- Foreign Corporation: A company incorporated outside of the United States for tax purposes.

These terms establish the framework for determining who must file and how payments should be reported.

Form Submission Methods

Form 1042 can be submitted both electronically and on paper. Many withholding agents opt for electronic submission via the IRS's Filing Information Returns Electronically (FIRE) system for efficiency and speed. However, paper submissions are accepted, provided they follow all IRS guidelines and are mailed to the designated IRS address by the specified deadline.

Choosing the best submission method depends on several factors, including the volume of forms and the technological resources available to the filer.

Taxpayer Scenarios: Examples

Various real-world scenarios necessitate the filing of Form 1042. For instance:

- Corporations distributing dividends to international shareholders.

- Universities paying research grants to foreign scholars not resident in the U.S.

- Financial institutions remitting interest payments to nonresident alien account holders.

These examples illustrate the diverse range of transactions that Form 1042 encompasses, emphasizing its role in maintaining compliance for U.S.-sourced income distributed to foreign entities.