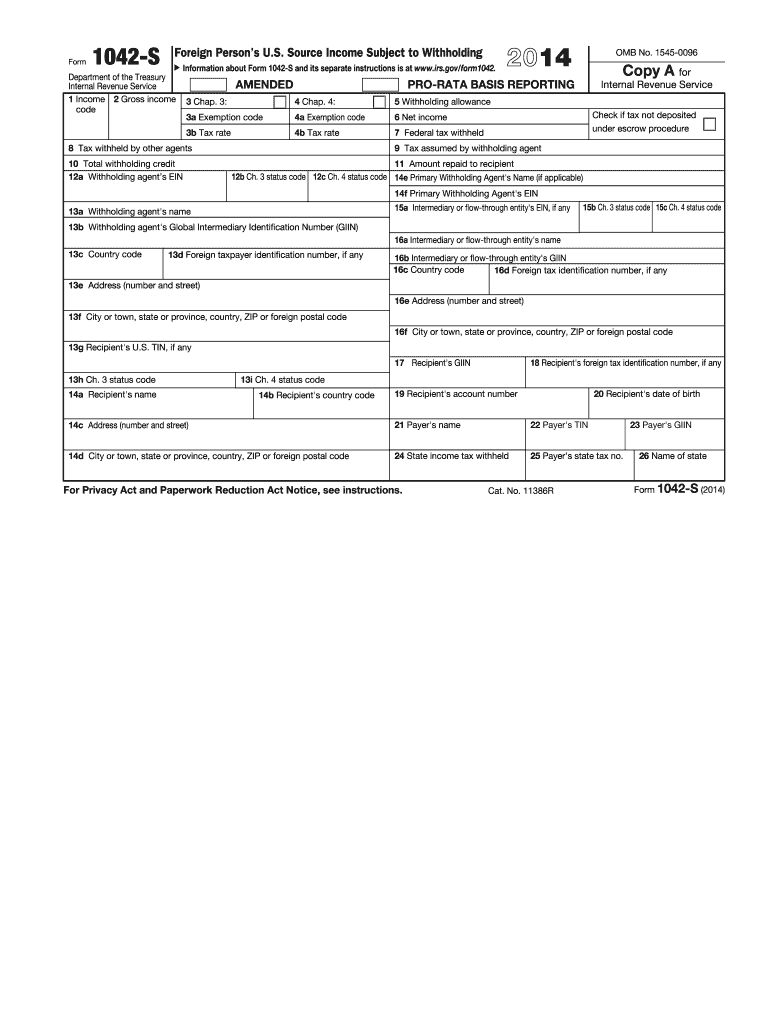

Definition and Purpose of Form 1042-S

Form 1042-S is an IRS tax form used to report income derived from U.S. sources that is paid to foreign persons, including nonresident aliens, foreign corporations, or partnerships, by a U.S. withholding agent. It details income types subject to withholding, such as interest, dividends, or royalties. Form 1042-S includes critical information such as withholding rates, exemption codes, and income amounts. Withholding agents must use this form to document their compliance with U.S. tax withholding obligations.

Use Cases

- Nonresident Aliens: Individuals living outside the U.S. receiving income like scholarships, wages, or royalties from U.S. sources.

- Foreign Corporations and Partnerships: Foreign business entities doing business with or within the U.S.

- Withholding Agents: U.S. entities responsible for withholding taxes on income paid to foreign persons, such as financial institutions or employers.

How to Obtain the 2014 Form 1042-S

Download and Access Methods

- IRS Website: The form can be directly downloaded as a PDF from the IRS official website. Navigate to the "Forms and Publications" section.

- Tax Software: Many tax software platforms provide access to Form 1042-S, facilitating electronic filing and record-keeping.

- Professional Preparers: Tax professionals often supply the form for clients who fall under its purview.

Alternative Formats

- Digital Copies: Ideal for those who prefer filing online and maintaining digital records.

- Paper Copies: For individuals or businesses that require hard copies for manual completion and mailing.

Steps to Complete the 2014 Form 1042-S

-

Gather Required Information: Obtain all relevant personal and income information for both the withholding agent and the foreign recipient, including names, tax identification numbers, and addresses.

-

Identify Income Amounts: Precisely document each type of income paid to the foreign entity or individual, making sure to utilize the IRS income codes to specify different types of earnings.

-

Determine Withholding Amounts: Calculate withholding tax based on applicable tax rates and exemptions. Use exemption codes where eligible.

-

Fill Out Each Section: Complete all sections of the form, ensuring accuracy in recipient and withholding agent details.

-

Review and Submit: Double-check all information for mistakes or omissions before submission. Ensure the form is submitted via preferred methods by the filing deadline.

Who Typically Uses the 2014 Form 1042-S?

Primary Users

- Educational Institutions: Universities paying scholarships or grants to foreign students.

- Financial Institutions: Banks handling interest and dividends payments to international clients.

- Corporations: U.S. companies that pay out royalties, salaries, or other compensations to foreign employees or stakeholders.

Key Elements of the 2014 Form 1042-S

Essential Sections

- Recipient's Details: Includes the foreign person's name, address, and tax identification number.

- Withholding Agent's Details: The U.S. entity responsible for reporting and withholding taxes.

- Income Information: Detailed breakdown of income types, amounts, and corresponding tax rates.

- Exemption and Withholding Codes: Indicate the nature of any exemptions applied and the basis for withholding amounts.

IRS Guidelines for Form 1042-S

Compliance Requirements

- Withholding agents must accurately report income types and amounts paid to foreign entities.

- Proper documentation and accurate record-keeping are essential to meet IRS compliance expectations.

- The IRS outlines strict penalties for late filings or misreporting, emphasizing the importance of timely and accurate submissions.

Filing Deadlines and Important Dates

- Annual Filing Date: Generally, Form 1042-S must be filed by March 15 of the year following the tax year when the income was paid.

- Extensions: Withholding agents may apply for an extension, if necessary, using IRS Form 8809.

Penalties for Non-Compliance

Common Infractions

- Late Filing: Not submitting Form 1042-S by March 15 can result in financial penalties.

- Incorrect Information: Providing inaccurate information may incur additional IRS penalties.

- Underreporting: Failure to report all applicable income types or understated withholding amounts could lead to significant sanctions.

Businesses and individuals must ensure proper adherence to IRS guidelines to avoid punitive measures and secure accurate tax withholding and reporting status.