Definition and Purpose of Form 1042-S

Form 1042-S, officially issued by the Internal Revenue Service (IRS), is specifically designed to report U.S. source income paid to foreign persons that are subject to withholding. This form applies to nonresident aliens, foreign partnerships and corporations, and even some foreign trusts and estates. Its primary purpose is to document distributions made to foreign entities and individuals, detailing the types and amounts of income, tax withheld, and any applicable exemption codes. It plays a crucial role in ensuring such income is reported accurately for tax purposes, both to the IRS and to the individual receiving the income.

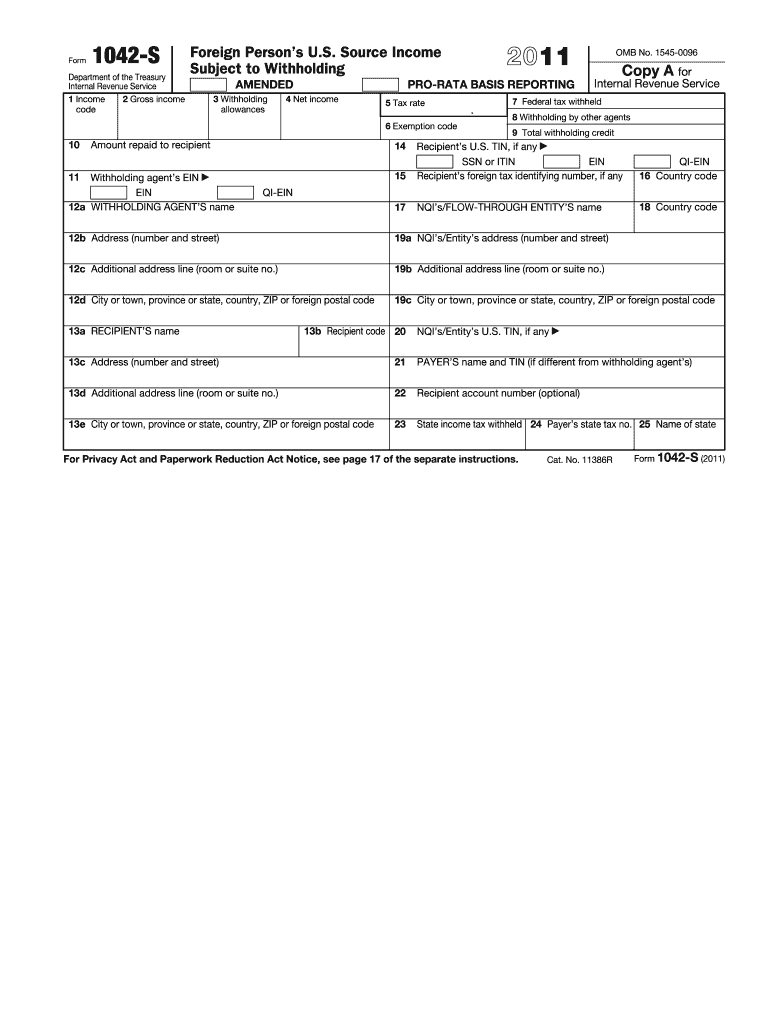

Key Components of Form 1042-S

- Income Information: Captures various types of U.S.-based income paid to foreign individuals or entities, such as dividends, interest, and royalties.

- Withholding Details: Specifies the amount of tax withheld at the source as per U.S. tax regulations.

- Exemption Codes: Lists codes that might exempt the recipient from withholding under certain treaties or conditions.

How to Use the 2011 Form 1042-S

This form is essential for foreign individuals and entities receiving income from U.S. sources. Recipients must use the details on Form 1042-S to comply with U.S. tax obligations. This includes recognizing the income in their country of residence if required and claiming credits or refunds for any withholding taxes paid. It's important for recipients to precisely carry the figures from the 1042-S onto any relevant tax forms they file in the U.S. or their home country.

Step-by-Step Usage Instructions

- Review the Form: Begin by examining the form to ensure accuracy in the details provided, such as income type and the amount reported.

- Record the Withholding: Accurately note tax withheld as this affects potential refund claims.

- File Appropriately: Use the details reported on this form when completing tax returns in the U.S. or the recipient’s country.

Obtaining the 2011 Form 1042-S

Form 1042-S is typically provided by the withholding agent or payer, which could be an employer, financial institution, or other entity that handle the disbursement of funds. It is crucial to ensure receipt of this form by the IRS deadline each tax year to comply with tax filing obligations.

Common Sources for Obtaining the Form

- Withholding Agent: Usually responsible for issuing the form.

- Employers: Offer the form if wages were paid subject to withholding.

- Financial Institutions: Provide the form if there were investments yielding income.

Steps to Complete the 2011 Form 1042-S

Completing Form 1042-S involves several specific steps that ensure all income and withholding are duly recorded and attributed to the correct foreign recipient.

- Filling Basic Information: Enter necessary identification details such as the name and taxpayer identification number of both the payer and recipient.

- Complete Income Sections: Accurately list each type of income along with relevant tax codes.

- Verify Withholding Amounts: Ensure all withholding figures are exact, corresponding to income types.

Tips for Accurate Completion

- Use Correct Codes: Check IRS codes to correctly identify income types and exemptions.

- Double-check Entries: Misreporting could lead to compliance issues or penalties.

Legal Use and IRS Guidelines

The IRS provides specific regulations regarding the completion and submission of Form 1042-S. Following these guidelines helps prevent errors and ensures compliance.

IRS Regulatory Guidance

- Filing Deadline: Generally due along with other tax forms on March 15 following the tax year.

- Correct Reporting: U.S. withholding agents are mandated to use the form properly to report income paid and tax withheld for foreign recipients.

Key Elements of the 2011 Form 1042-S

Some of the crucial elements of this form include the income code, exemption code, and recipient type, which detail why and how withholding was applicable. The income code specifies the type of income paid, while the exemption code might indicate a reduced withholding rate under an applicable tax treaty.

Elements Explained

- Income Code: Determines the kind of income, such as royalties, dividends, or interest.

- Exemption Code: Explains any reducing factors in withholding because of specific treaties.

Filing Deadlines and Important Dates

For the 2011 tax year, the form was typically required to be filed by March 15, 2012. Timely filing is essential to avoid penalties and ensure tax compliance.

Important Considerations

- Late Filings: Can result in significant fines and complicate tax reporting processes.

- Amendments: If necessary, amendments should be processed promptly to correct discrepancies.

Penalties for Non-Compliance

Failing to issue or file Form 1042-S correctly can lead to penalties, including fines for each instance of failing to file a correct form with the IRS and providing a copy to the recipient.

Penalty Breakdown

- Form Filing Errors: Typically results in monetary fines.

- Late Filing: Encounters penalties that could increase the longer the delay in submission remains unresolved.