Definition & Purpose of Form 1042-S

Form 1042-S, issued by the IRS, is used to report U.S. source income paid to foreign persons that is subject to withholding. This includes nonresident aliens, foreign corporations, and similar entities. The form captures details like income amount, withholding allowances, tax rates, and recipient information. It is used to ensure compliance with U.S. tax laws by showing that taxes on certain types of income have been appropriately withheld at the source.

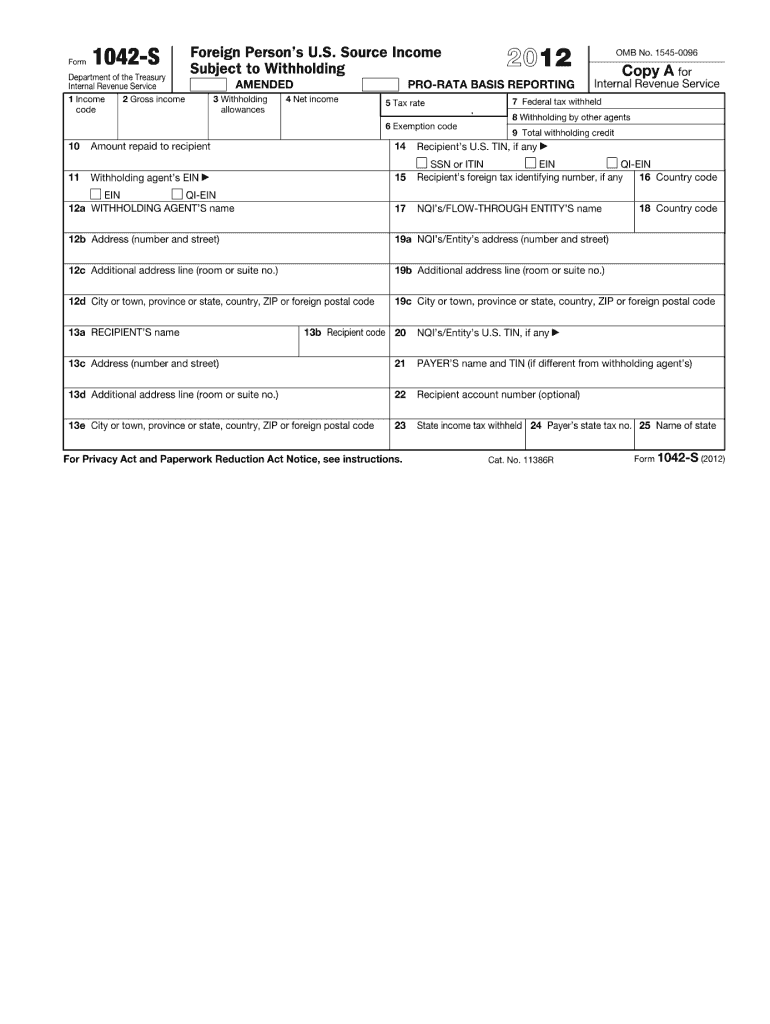

Key Components of Form 1042-S

- Income Details: Information about U.S. source income paid to foreign persons, including the type and amount.

- Withholding Information: The tax rate and the amount of withholding applied to the payments.

- Recipient Details: Information about the foreign recipient, including name, address, and tax identification number.

- Exemption Codes: Codes indicating why no tax was withheld if applicable.

How to Use Form 1042-S

Foreign persons receiving U.S. source income should use Form 1042-S to report income on their U.S. tax returns. It helps determine if additional taxes are owed or if a refund is due. The form is typically used by recipients to file alongside their annual tax returns and is critical for ensuring the correct tax treatment of received income.

Steps to Complete Form 1042-S

- Gather Required Information: Ensure all relevant data is available, including details about the payer (withholding agent) and the recipient.

- Complete Identification Sections: Fill in the name, address, and taxpayer identification number of both the payer and recipient.

- Enter Income Information: Include income codes, gross income paid, and any applicable exemption codes.

- Detail Withholding Information: Input the amount withheld, applicable withholding tax rates, and any adjustments if necessary.

- Submit the Form: Once completed, submit the form as part of the annual tax filing.

Filing Deadlines and Important Dates

- Annual Submission: Form 1042-S must generally be filed annually by March 15 following the calendar year in which the income was paid.

- Filing Extensions: In certain situations, an extension may be applied for using IRS Form 8809.

Who Typically Uses the 2012 Form 1042-S

- Nonresident Aliens: Individuals who are not U.S. citizens or residents but receive income from U.S. sources.

- Foreign Corporations: Corporations registered outside the U.S. receiving payments from U.S. based entities.

- Foreign Partnerships and Trusts: These entities use the form to report income and withholding effectively.

IRS Guidelines and Regulations

- Withholding Obligations: The IRS mandates certain withholding agents to deduct taxes on specified income types before making payments to foreign recipients.

- Record Keeping: Entities should maintain detailed records supporting the entries on the form, including contracts, invoices, and correspondence.

Penalties for Non-Compliance

Failure to file Form 1042-S accurately and timely can result in substantial penalties from the IRS. These penalties may apply to both the withholding agents and the foreign recipients. It’s crucial to adhere strictly to filing requirements and deadlines.

Digital vs. Paper Version

- Digital Filing: The IRS allows for electronic filing of Form 1042-S, which is often more efficient and less error-prone.

- Paper Filing: Still an option, but it requires more manual work and is generally slower in processing.

Software Compatibility and Filing Tools

Software like TurboTax and QuickBooks may assist with the accurate preparation and filing of Form 1042-S, though specialized tax software geared towards international transactions may be best suited for the complex components of this form.