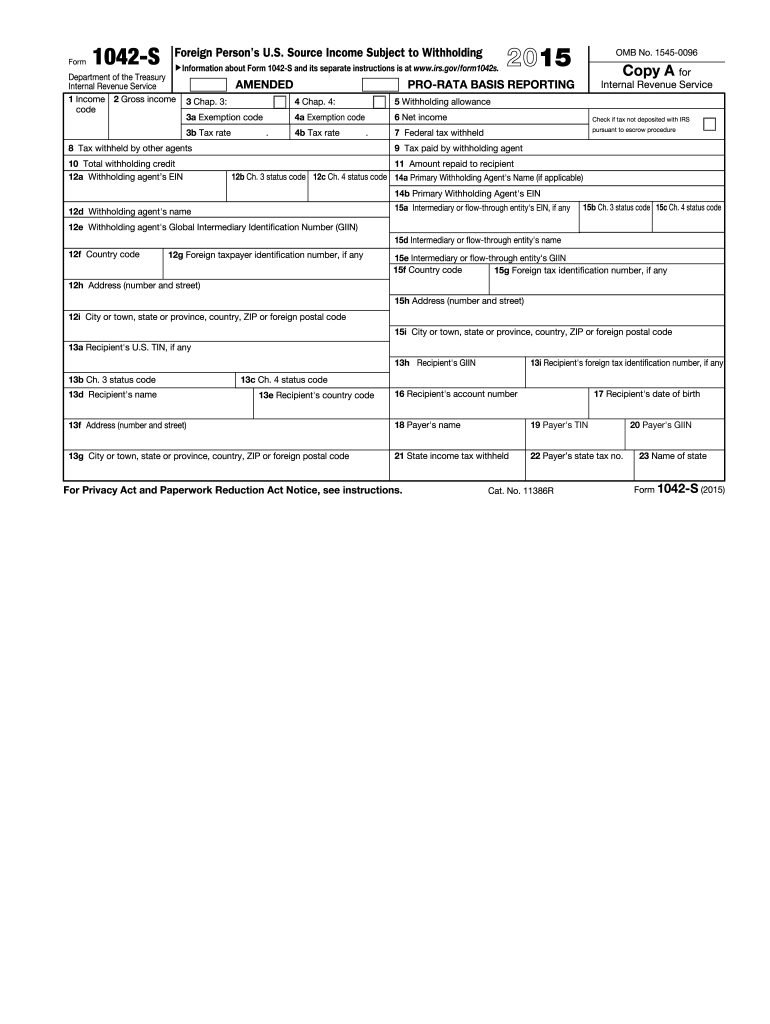

Definition and Purpose of Form 1042-S

Form 1042-S is used to report U.S. source income paid to foreign individuals and entities subject to withholding, such as nonresident aliens and foreign corporations. Foreign persons receiving income from U.S. payers must file this form to ensure compliance with U.S. tax laws. The form details various types of income, applicable tax rates, exemption codes, and withholding amounts, serving as a comprehensive record for both taxpayers and the IRS.

How to Use Form 1042-S (2015)

Using Form 1042-S involves recording necessary income details of foreign payees and ensuring proper withholding. Entities making payments must complete a separate form for each recipient, providing details such as the recipient’s name, country, income type, and tax rate. It is vital for withholding agents to keep detailed records, as they are held accountable for the correct application of withholding rules.

Obtaining Form 1042-S (2015)

To obtain Form 1042-S, you can download it directly from the IRS website. Ensure you have the correct year’s form, as tax laws and requirements can vary annually. Additionally, tax filing software often includes options to generate this form as part of the tax preparation process.

Steps to Complete Form 1042-S (2015)

- Identify Recipients: Begin by listing all foreign persons who received U.S. source income.

- Enter Personal Details: Provide the name, address, and TIN for each recipient.

- Report Income Types: Specify the type of income paid (e.g., dividends, royalties).

- Calculate Tax Withheld: Determine the correct withholding amount based on income type and applicable tax treaties.

- Complete and Review: Verify all information for accuracy to ensure compliance with IRS standards.

Key Elements of Form 1042-S (2015)

- Recipient Details: Information about the income recipient, including their foreign address and TIN.

- Income Information: Detailed descriptions of income types and amounts paid during the year.

- Withholding Rates and Exemptions: Applicable tax rates, any exemptions, and the total amount withheld.

- Payer Information: Details about the withholding agent, including their EIN and contact information.

Important Terms Related to Form 1042-S

- Withholding Agent: The entity responsible for withholding tax and issuing Form 1042-S.

- Nonresident Alien: An individual not residing in the U.S. for tax purposes but receiving U.S. source income.

- Exemption Code: Codes that represent specific tax treaties or conditions allowing reduced withholding.

- TIN (Taxpayer Identification Number): A unique number assigned to individuals and entities for tax purposes.

Filing Deadlines and Important Dates

The deadline to furnish Form 1042-S to the IRS is March 15th of the year following the payment. Payers must also provide copies to recipients by this date to ensure they have time to meet their tax filing obligations. Failure to comply with these deadlines can result in penalties.

Penalties for Non-Compliance with Form 1042-S

Non-compliance can lead to significant penalties, including a fixed penalty per form not filed or furnished correctly, escalating with the delay's duration. Withholding agents may also face penalties for late payments or underpayments of tax. It's crucial to comply fully to avoid these financial consequences.

By understanding and leveraging the detailed guidance above, withholding agents can ensure they meet all IRS requirements for reporting foreign income, thus maintaining compliance and avoiding potential penalties.