Definition and Purpose of the 2011 Form 940

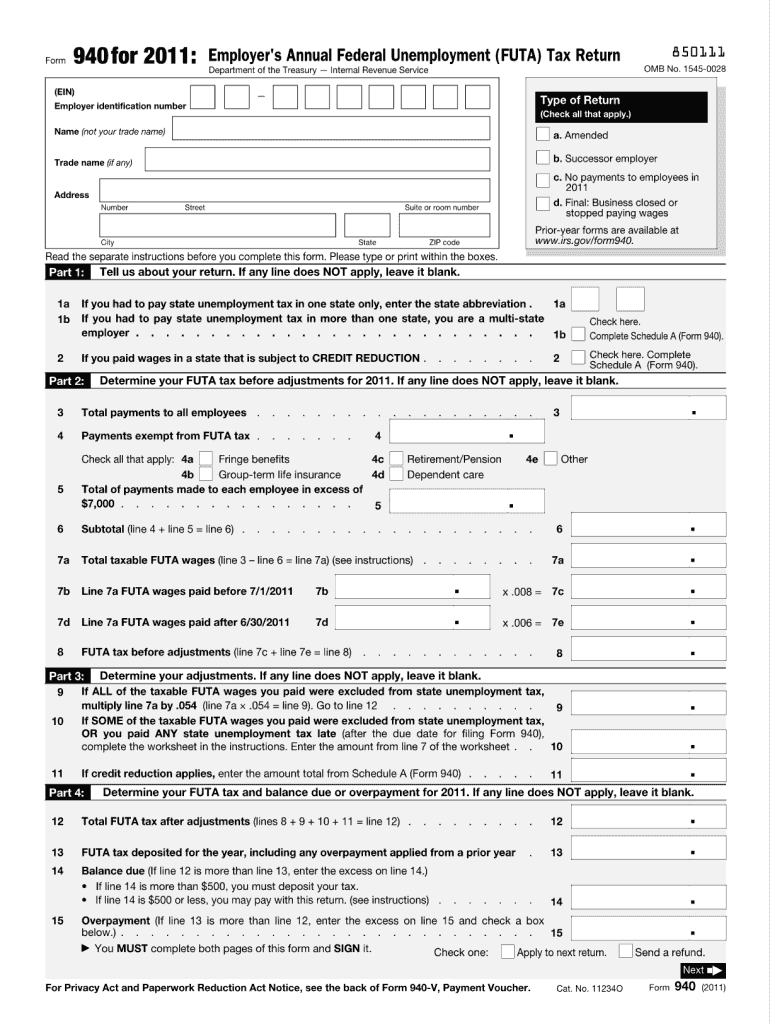

The 2011 Form 940, officially known as the "Employer's Annual Federal Unemployment (FUTA) Tax Return," is a tax document used by employers in the United States. This form is required for reporting the annual Federal Unemployment Tax Act (FUTA) tax, which helps fund unemployment compensation to workers who have lost their jobs. The primary purpose of this form is to report and pay unemployment taxes at the federal level.

How to Obtain the 2011 Form 940

To obtain the 2011 Form 940, employers can access it through various channels:

-

IRS Website: The form can be downloaded directly from the official IRS website, ensuring that the most accurate and up-to-date version is used.

-

Tax Software: Many tax preparation software programs, such as TurboTax and QuickBooks, include the 2011 Form 940 and facilitate electronic filing.

-

Tax Professionals: Employers may consult with tax professionals who can provide the form and assist with its completion.

Steps to Complete the 2011 Form 940

Completing the 2011 Form 940 requires careful attention to detail. Here are the steps involved:

-

Gather Information: Collect all necessary information about wages paid and unemployment tax already paid to state agencies.

-

Calculate FUTA Tax: Compute the FUTA tax owed by applying the applicable tax rate to the first $7,000 of wages paid to each employee.

-

Fill Out the Form: Enter required details such as employer identification number (EIN), total wages, and adjustments.

-

Review and Submit: Double-check the information for accuracy before submitting the form through mail or electronically via an authorized e-filing system.

Important Terms Related to the 2011 Form 940

Understanding specific terminology is crucial when dealing with the 2011 Form 940:

- FUTA Tax: A federal tax imposed on employers, used to fund unemployment benefits.

- Taxable Wages: The portion of employee wages subject to FUTA tax, up to $7,000 per employee.

- FUTA Tax Rate: The rate applied to taxable wages to compute the amount of FUTA tax owed.

Filing Deadlines and Important Dates for the 2011 Form 940

Employers must adhere to specific deadlines when filing the 2011 Form 940:

- Annual Deadline: The form must be filed by January 31 of the following year. For the 2011 form, the due date would be January 31, 2012.

- Quarterly Payments: If the FUTA tax liability exceeds $500 during a quarter, it must be paid by the end of the month following that quarter.

Penalties for Non-Compliance

Failure to properly file the 2011 Form 940 can result in penalties:

- Late Filing Penalty: A penalty amounting to 5% of the unpaid tax per month, up to a maximum of 25%.

- Late Payment Penalty: A penalty of 0.5% of the unpaid tax for each month the tax remains unpaid.

Who Typically Uses the 2011 Form 940

The 2011 Form 940 is primarily used by employers who meet the following criteria:

- Wage Payments: Employers who have paid wages of $1,500 or more in any calendar quarter.

- Employee Count: Employers who have employed at least one worker for some part of a day in 20 different weeks during the year.

IRS Guidelines and Instructions for the 2011 Form 940

The IRS provides official guidelines to assist in accurately completing the 2011 Form 940:

- Form Instructions: Detailed instructions accompany the form, explaining each line and entry.

- Compliance Requirements: The IRS outlines specific compliance requirements, ensuring proper reporting and payment of FUTA taxes.

Digital vs. Paper Version of the 2011 Form 940

Filing the 2011 Form 940 can be done via digital or paper methods:

- Digital Filing: Offers convenience and faster processing; supported by various tax preparation software.

- Paper Filing: Employers can mail the completed form to the IRS, but should account for postal delivery time to meet deadlines.

By understanding the purpose, obtaining the form, following detailed completion steps, and adhering to deadlines, employers can ensure compliance with federal requirements when filing the 2011 Form 940.