Definition of Form 940, Employer's Annual Federal Unemployment (FUTA) Tax Return

Form 940 is an essential tax document used by employers in the United States to report their annual Federal Unemployment Tax Act (FUTA) liabilities. The form calculates the amount of unemployment tax owed, which is crucial for funding unemployment benefits nationwide. As part of federal employment taxes, the FUTA tax is separate from state unemployment taxes and applies to the first $7,000 paid to each employee as wages.

Purpose and Functionality

-

Tax Assessment: Form 940 calculates the FUTA tax owed annually by an employer. The standard FUTA tax rate is 6.0%, but employers can often claim a tax credit of up to 5.4% when timely paying state unemployment taxes, which reduces their effective FUTA tax rate to 0.6%.

-

Employee Coverage: FUTA tax obligations apply to a range of employee wages, ensuring employees can access unemployment benefits if they lose their job under qualifying circumstances.

-

Compliance: Filing Form 940 is mandatory for businesses that have paid wages of $1,500 or more in any calendar quarter or have had employees working at least some part of a day in 20 or more weeks during the current or previous calendar year.

Steps to Complete Form 940, Employer's Annual Federal Unemployment (FUTA) Tax Return

Filling out Form 940 requires careful attention to various sections to ensure accurate tax reporting.

-

Gather Information:

- Collect employee wage data for the calendar year.

- Determine any state unemployment tax payments made.

-

Calculate Tax Liability:

- Complete Part 1 to report total payments and calculate unemployment tax liability.

- Adjust for potential credits due to state unemployment taxes in Part 2.

-

Finalize Calculations:

- Use Part 3 to report the final unemployment tax due, factoring in any additional credits or liabilities.

- Calculate and enter any balance due or overpayment.

-

Review and Submit:

- Ensure all information is correct before signature.

- Submit the completed form alongside any payments due, adhering to the filing method chosen.

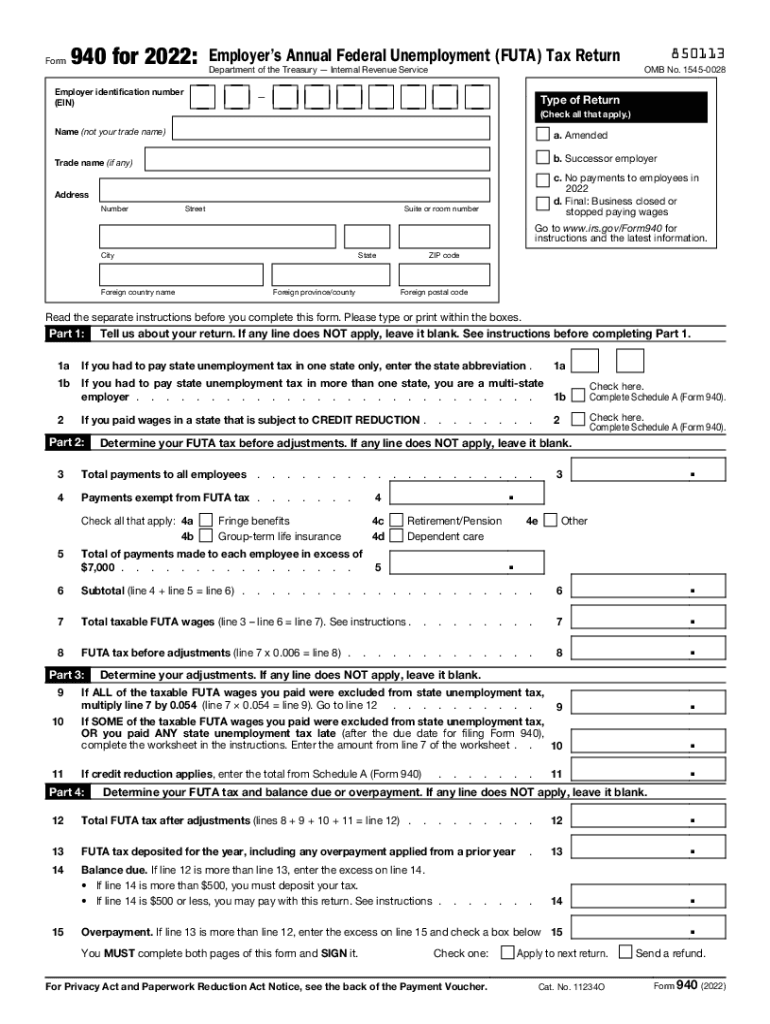

Important Sections of the Form

- Part 1: Addresses amendments to prior calculations and includes critical adjustments. Complete this section accurately to avoid potential penalties.

- Part 2: Calculation of FUTA tax consideration with possibility for reduced rate based upon timely state unemployment tax payment.

- Part 3: Summary of tax liabilities and adjustments to arrive at the total tax due or refundable.

How to Obtain Form 940

Employers can access Form 940 in multiple ways, ensuring a seamless transition to compliance with federal tax regulations.

-

Online Access: The Internal Revenue Service (IRS) provides a downloadable PDF version of Form 940 on their official website.

-

Physical Copies: Paper forms can be requested directly from the IRS or obtained at local IRS offices.

-

Through Tax Software: Most professional tax preparation software solutions include up-to-date versions of all IRS forms, including Form 940.

IRS Guidelines and Requirements for Form 940

Employers must follow specific guidelines when filing Form 940:

-

Eligibility Criteria: Includes paying wages to at least one employee for some part of a day during 20 different weeks in a calendar year or paying wages of at least $1,500 in any calendar quarter.

-

Filing Deadlines: The official deadline for submitting Form 940 is January 31st following the end of the calendar year. If any FUTA tax liability remains unpaid after the deadline, penalties or interest may apply.

-

Amended Returns: Any errors identified after submission must be rectified by filing an amended return as stipulated by the IRS.

Penalties for Non-Compliance

Failure to accurately complete or timely file Form 940 may incur penalties. The IRS imposes fines based on the degree and timing of the violation, including:

-

Late Filing Penalties: Calculated as a percentage of the unpaid tax, depending on how overdue the filing is.

-

Accuracy-Related Penalties: If forms are completed inaccurately, additional penalties may apply, enhancing scrutiny on subsequent filings.

Form Submission Methods

Employers have several options when it comes to submitting Form 940 to ensure flexibility and accessibility:

-

Electronic Filing: Using IRS e-file systems or authorized third-party software is the fastest method and promotes accuracy with automated error checking.

-

Mail Submission: For traditional paperwork submission, the IRS provides specific addresses based on the employer's location.

-

In-Person Submission: Assistance at local IRS offices is available for specific inquiries or detailed support, although the physical submission isn't required at these locations.

Key Elements and Terminology in Form 940

Understanding the terminology in Form 940 ensures clarity and precision during preparation.

-

FUTA Tax Rate: The base rate used to calculate the taxes owed under the FUTA, subject to reductions based on state tax credits.

-

Credit Reduction States: States that have not repaid their federal loans are subject to credit reductions, impacting the amount of tax owed.

-

Payment Voucher (Form 940-V): Used to accompany tax payments if submitting by mail to ensure proper processing and credit allocation.

State-Specific Rules and Considerations

Each state may have its own unemployment tax regulations, affecting how the FUTA tax is calculated and reported:

-

Credit Availability: Varies by state, affecting potential tax savings for timely payment of state unemployment taxes.

-

State Tax Implications: Some states require separate reporting or acknowledgment of federal tax calculations for compliance.

Exploring these areas offers a comprehensive understanding of Form 940 and its critical role in employer tax responsibilities, especially in relation to ensuring legal compliance and supporting the broader social safety net through unemployment insurance funding.