Definition and Purpose of Form 940

Form 940 is known as the Employer's Annual Federal Unemployment (FUTA) Tax Return. This form is crucial for employers as it reports the unemployment tax liability they have incurred over the year. The IRS requires this form to ensure employers comply with paying federal unemployment taxes, which fund unemployment compensation for workers who have lost their jobs. The FUTA tax is separate from state unemployment taxes and is designed to provide a safety net for those temporarily without work.

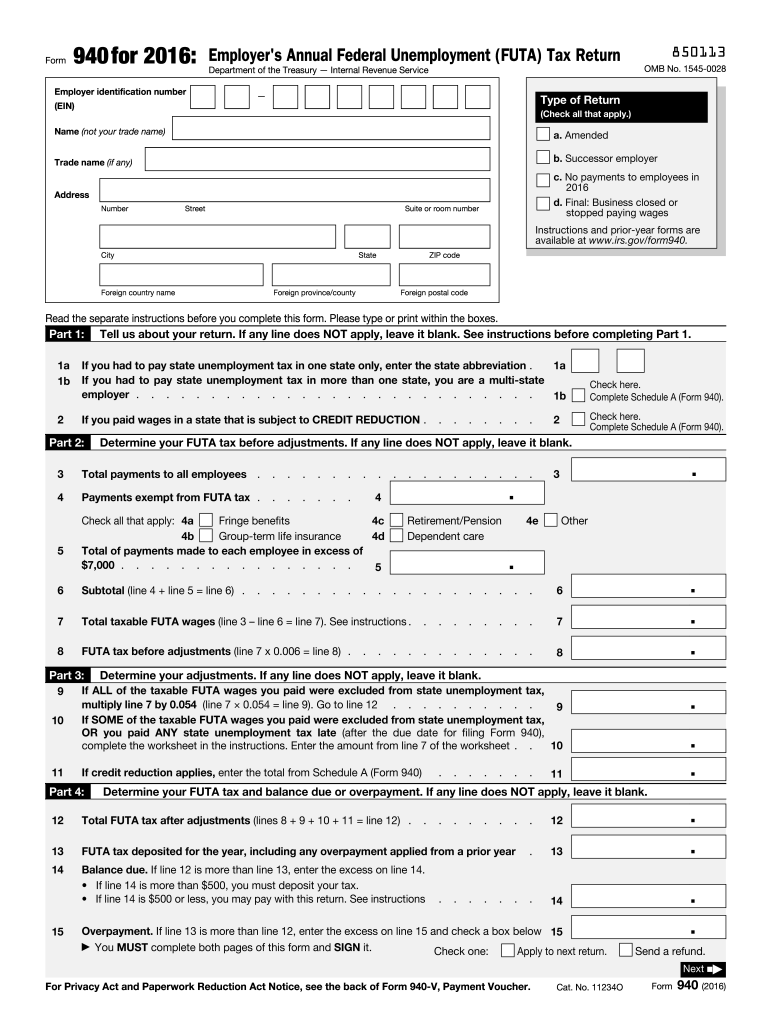

Key Elements of Form 940

The 2016 Form 940 includes several sections that businesses need to complete accurately. These sections encompass the total payments made to employees, the FUTA tax adjustments, credit reductions, and the calculated tax owed. Employers must review these elements to avoid errors in reporting their tax liability. Understanding each component allows businesses to correctly assess their financial obligations to the IRS.

Step-by-Step Completion Guide

-

Identify Employer Information: Begin by entering the employer's identification, including name, address, and employer identification number (EIN). This ensures that the IRS can accurately associate the form with the taxpayer.

-

Calculate Total Wages: Input the total wages paid to employees throughout the year. It’s important to only include those wages subject to FUTA tax.

-

Determine Adjustments: Review any adjustments that might affect the FUTA tax calculation. This includes exempt wages, such as those paid to certain nonprofit organization employees.

-

Apply State Credits: If you paid state unemployment taxes, you might be eligible for a credit, reducing the FUTA tax owed. Properly calculating these credits ensures that you are not overpaying.

-

Summarize Total Taxes Due: After completing the necessary calculations on the form, derive the total FUTA tax due. This figure is critical as it determines the final amount owed to the IRS.

Who Uses Form 940

Form 940 is primarily used by U.S.-based employers subject to the Federal Unemployment Tax Act. This includes businesses that paid wages of $1,500 or more during any calendar quarter of the year, or those that had at least one employee working for 20 or more weeks. Nonprofit organizations, government entities, and select small businesses might have different reporting requirements but often must still address FUTA obligations.

Filing Deadlines and Important Dates

Employers are generally required to file Form 940 annually, with a due date of January 31 of the following year. However, if the FUTA tax was deposited in full and on time, the deadline extends to February 10. It is crucial for employers to adhere to these deadlines to avoid penalties and interest charges for late filings.

Software Compatibility for Form 940

Form 940 can be prepared and filed using various tax software solutions, such as TurboTax and QuickBooks, which provide functionalities tailored to the needs of businesses. These tools simplify the process of data entry and force error-checking, aiding taxpayers in meeting IRS standards efficiently.

Legal Use and Compliance

Maintaining compliance with FUTA tax regulations involves accurate completion and timely filing of Form 940. The IRS guidelines demand that employers report all taxable wages accurately and apply any eligible state unemployment tax credits correctly. Adhering to these requirements ensures that employers meet their legal obligations and avoid potential audits or penalties.

Penalties for Non-Compliance

Failure to file Form 940 on time can result in penalties, typically calculated as a percentage of the unpaid tax for each month the return is late. The IRS may also impose interest on the overdue amount, compounding daily until full payment is received. Compliance with filing requirements protects employers from such financial repercussions.

State-Specific Rules

While FUTA tax is a federal obligation, each state may have unique rules affecting the application of credits against the federal tax. For example, wage base limits or tax rates may differ, influencing the overall calculation of the tax due. Employers must stay informed of their state-specific regulations to ensure correct FUTA tax reporting.

By following these guidelines, employers can effectively manage their unemployment tax responsibilities and fulfill their annual reporting obligations accurately.