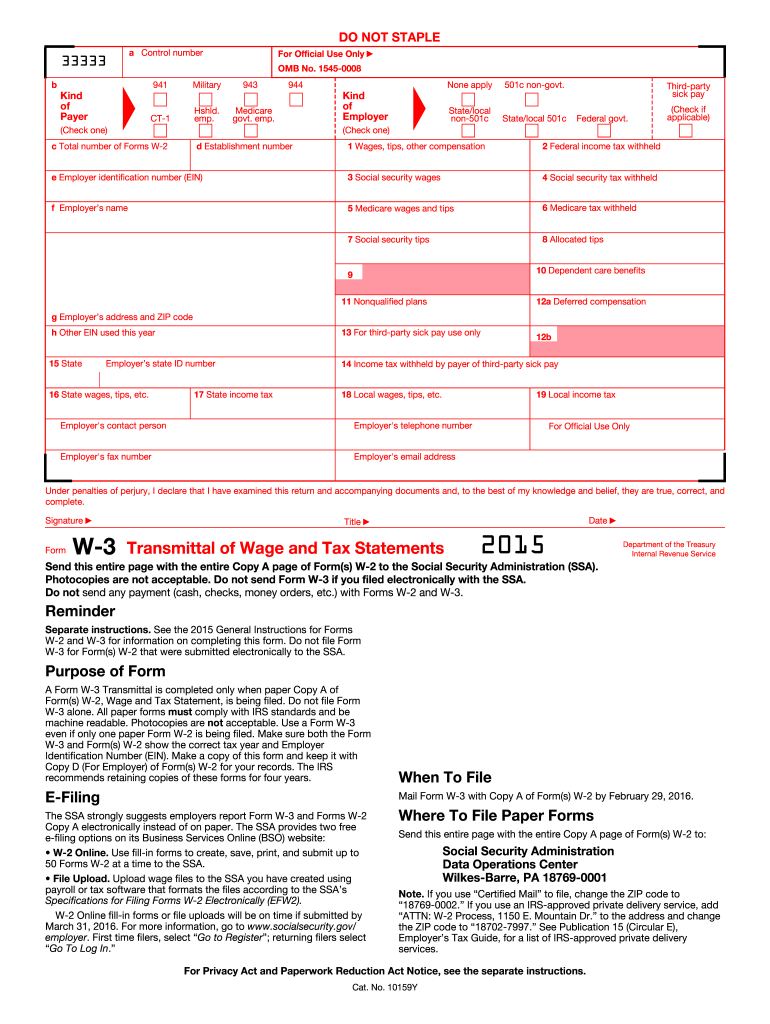

Definition and Meaning of the 2015 W-3 Form

The 2015 W-3 form, also known as the Transmittal of Wage and Tax Statements, is a summary document used by employers to transmit copies of employees' W-2 forms to the Social Security Administration (SSA). The W-3 form details the total wages paid and taxes withheld across an organization for the tax year, serving as a summary of all the individual wage and tax statements issued by the employer. This form is crucial for maintaining accurate records with the federal government and ensuring compliance with tax laws.

How to Use the 2015 W-3 Form

Employers must fill out the W-3 form when submitting the W-2 forms to the SSA. It’s essential to ensure that all information aligns precisely between the W-2s and the W-3 to avoid discrepancies. Employers can choose to file the form electronically, which is recommended by the SSA, especially if they are filing 250 or more forms, as it simplifies the process and reduces errors.

- Ensure each W-2 form's totals add up correctly on the W-3.

- Use the W-3 summary to verify that all financial information is correct before submission.

- Maintain copies for your records to support future audits or inquiries.

Steps to Complete the 2015 W-3 Form

- Gather Information: Collect all employees' W-2 forms and verify that they are correctly filled out.

- Enter Employer Details: Fill out the employer's name, address, EIN, and contact information accurately.

- Fill in Totals: Input the total amounts for wages, Social Security wages, Medicare wages, withholding taxes, etc.

- Check Boxes: Check the appropriate boxes to indicate any corrections or amendments needed for prior submissions.

- Sign and Date: The form must be signed and dated by an authorized individual within the company.

Filing Deadlines and Important Dates

The filing deadline for the 2015 W-3 form was January 31, 2016. Employers need to ensure timely submission to avoid penalties. The SSA advises filing as soon as possible within January to mitigate the risk of last-minute issues. If filing electronically, the deadline remains the same.

Penalties for Non-Compliance

Failing to file the W-3 form correctly or missing the deadline can result in significant penalties. Employers may incur costs for late filing, incorrect information, or failure to keep copies for their records. For 2015, penalties ranged based on the lateness and the size of the company, emphasizing the importance of accuracy and timeliness.

Legal Use of the 2015 W-3 Form

The legal implications of the W-3 form center around its role in verifying wage and tax reporting. Employers must ensure compliance with both IRS and SSA regulations to prevent legal challenges, which can arise from misinformation or non-compliance. Accurate filing supports an employer's legal responsibility to honestly report employee earnings and tax withholdings.

Key Elements of the 2015 W-3 Form

- Employer Information: Vital for identifying the source of the forms and the origin of the wages.

- Income and Tax Totals: Serves as a cumulative figure from all individual W-2s.

- Submission Method: Indicates whether the form is manual or electronic.

- Reconciliation Totals: Ensures the sums reported match those on all W-2 forms filed.

IRS Guidelines for the W-3 Form

The IRS provides comprehensive guidelines concerning the completion and submission of both W-2 and W-3 forms. Following these guidelines can help employers understand the specific requirements, such as which numbers must match and how corrections should be handled. The guidelines also cover the electronic filing process and necessary software compatibility to ease the filing process for large businesses.

Software Compatibility for Filing

Employers often use software programs like TurboTax or QuickBooks to facilitate the filing of W-2s and the W-3 form. These programs can streamline the data collection process, handle calculations, and electronically submit the forms to the SSA, reducing the potential for human error. Compatibility with these tools ensures more efficient management of tax documents for the employer.