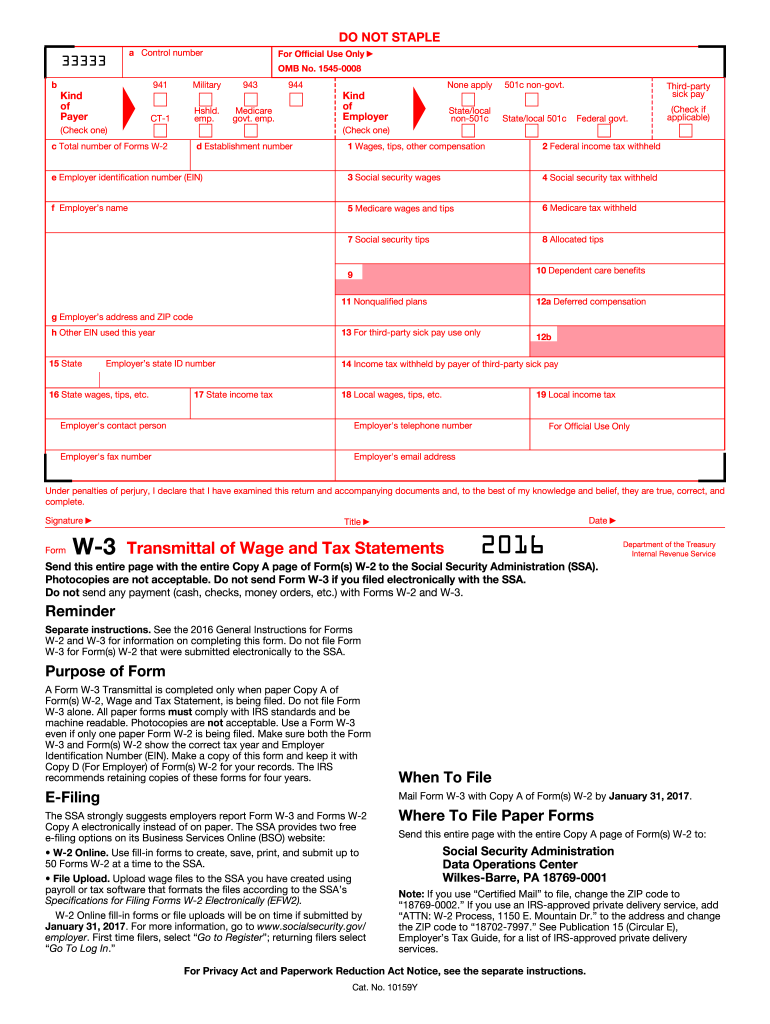

Definition and Purpose of Form W-3 2016

Form W-3, officially known as the Transmittal of Wage and Tax Statements, serves as a cover sheet for Forms W-2, summarizing employees' annual wages and taxes withheld. This document is integral to ensuring compliance with federal tax filing requirements, as employers must submit it to the Social Security Administration (SSA). In 2016, the form remained an essential part of the reporting process, facilitating correct recording of employee earnings and withholding data for tax purposes. The information on Form W-3 helps the SSA verify the earnings of employees, contributing to the accurate calculation of future Social Security benefits and other welfare programs.

How to Use Form W-3 2016

To use Form W-3, employers should gather all completed W-2 forms for their employees for the tax year 2016. After ensuring that each W-2 contains accurate wage and tax information, the employer must complete Form W-3 by summarizing the total wages paid and taxes withheld for all employees. The form then acts as a transmittal document accompanying the W-2 forms submitted to the SSA. Form W-3 is only required when filing one or more paper W-2 forms with the SSA, serving as a comprehensive cover letter that includes a summary of all collected data.

Steps to Complete Form W-3 2016

- Collect Employee Data: Ensure all W-2 forms are complete and accurate.

- Fill Out Business Information: Enter the employer’s EIN, company name, address, and contact information on Form W-3.

- Summarize Employee Wages and Taxes: Calculate and enter the total salaries paid and taxes withheld for all employees as reported on their W-2 forms, for fields like wages, Social Security wages, and Medicare wages.

- Cross-Verify Totals: Ensure that the totals on Form W-3 match the cumulative data from the W-2 forms.

- Choose Filing Method: Determine whether to file electronically or use paper forms. Note that electronic filing is required if submitting 250 or more W-2 forms.

- Submit to the SSA: Send Form W-3 along with the W-2 forms to the SSA by the stipulated deadline.

Filing Deadlines and Important Dates for Form W-3 2016

The deadline for submitting Form W-3 and accompanying W-2 forms to the SSA for the 2016 tax year was January 31, 2017. This deadline applies to both paper and electronic submissions. Employers should ensure timely filing to avoid penalties. Prior to submission, employers should also confirm that all information is accurate, as corrections after the filing deadline can complicate compliance and result in fines.

Penalties for Non-Compliance

Non-compliance with Form W-3 filing requirements can result in substantial penalties. If the employer fails to file by the deadline, the penalty starts at $50 per form and can escalate based on how late the submission is and the size of the business. Additionally, providing incorrect information or failing to file can result in further fines. These penalties are designed to encourage timely and accurate submission to prevent disruptions in wage and tax reporting, impacting Social Security records.

Key Elements of Form W-3 2016

- Employer Identification Number (EIN): Required for identifying businesses.

- Employer’s Contact Details: Business name and address for correspondence.

- Total Wages Paid: Aggregate of all wages paid to employees as reported on W-2 forms.

- Total Tax Withheld: Summed amounts of federal income, Social Security, and Medicare taxes withheld from employee wages.

- Number of W-2s Attached: Indicate how many forms are included with the W-3 submission.

Who Typically Uses Form W-3 2016

Form W-3 is primarily used by employers or business owners in the U.S. who have paid wages to employees throughout the tax year. This includes small businesses, large corporations, and nonprofit organizations. The form ensures that these entities report accurate wage and tax information to the SSA, fulfilling both federal and state requirements and setting the groundwork for employees’ tax returns and Social Security entitlements.

Digital vs. Paper Version of Form W-3 2016

The digital version of Form W-3 offers efficiency, ensuring quick submission and fewer errors due to automated checks through the IRS e-file system. Electronic filing is encouraged for those submitting more than 250 W-2 forms, offering benefits such as confirmation of receipt and processing. In contrast, paper submissions can be slower with a higher risk of errors, requiring careful manual validation before posting. The SSA provides specific guidelines to ensure that paper forms are printed correctly to facilitate scanning and processing.