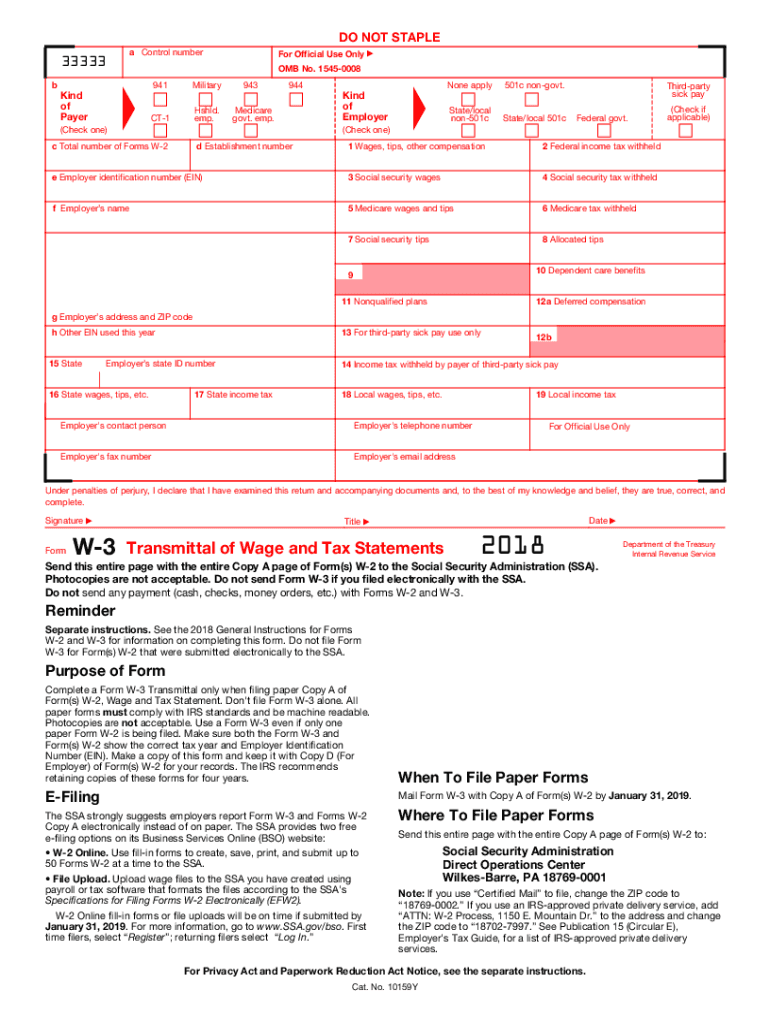

Definition & Meaning

The 2015 W-3 form, known as the Transmittal of Wage and Tax Statements, is a summary form filed with the Social Security Administration (SSA) to accompany the W-2 forms. This document provides a summary of the total wages, tips, and other compensation paid to employees, as well as the total income and Social Security taxes withheld throughout the year. The W-3 form acts as a reconciliation form to ensure that the total amounts reported on the accompanying W-2 forms match what is being submitted to the SSA. It's crucial for accurately reporting total wages and taxes paid by an employer.

How to Use the 2015 W-3 Form

Employers use the W-3 form to compile and transmit the information from multiple W-2 forms to the SSA. The process begins by collecting all the W-2 forms issued for the tax year. Each of these forms contains employee-specific details about earnings and tax withholdings. The W-3 form summarizes the totals from all employee W-2s, consolidating them into one document. Employers must ensure that all figures align correctly to avoid discrepancies. They must then submit the W-3 form to the SSA, either electronically or via mail, ensuring compliance with deadlines.

How to Obtain the 2015 W-3 Form

The 2015 W-3 form can be obtained through the IRS website or by ordering it directly from the IRS for physical copies. Some tax preparation software also provides printable forms that can be completed electronically. It's advisable for businesses to ensure they are using the correct year’s form by confirming the tax year on the document. Employers should also check if they have the latest version that matches IRS guidelines for that specific tax year, as forms may be updated or revised.

Steps to Complete the 2015 W-3 Form

- Gather Employee W-2 Forms: Collect all completed W-2 forms for the respective tax year.

- Enter Employer Information: Fill in details such as the employer's name, address, and EIN.

- Summarize Employee Data: Record totals for wages paid, federal income tax withheld, Social Security wages, and Medicare wages.

- Reconcile with Payroll Records: Verify that the totals match your payroll records to prevent errors.

- Include Special Codes if Needed: If applicable, incorporate any specific codes related to retirement plans or third-party sick pay.

- Sign and Date the Form: Ensure that a responsible person reviews and signs the form.

- Submit the Form to SSA: File electronically through the SSA Business Services Online platform, or mail the form along with the W-2 copies.

Important Terms Related to 2015 W-3 Form

- EIN (Employer Identification Number): A unique number assigned to businesses by the IRS for tax purposes.

- Wages, Tips, Other Compensation: The total amount paid to employees before any deductions.

- Federal Income Tax Withheld: The total tax withheld from an employee's wages.

- Social Security and Medicare Wages: The earnings subject to Social Security and Medicare taxes.

- Codes for Special Situations: Lists specific scenarios like statutory employees or retirement plans that require additional reporting on W-3 and W-2 forms.

Filing Deadlines and Important Dates

For the 2015 tax year, employers were required to submit both the W-2 forms and the W-3 form to the SSA by February 29, 2016, for paper filing, or by March 31, 2016, if filing electronically. Timely filing is crucial to avoid penalties and ensure accurate processing. The deadlines facilitate the SSA's ability to process wage reporting promptly, which further affects employees' tax filings and Social Security benefits.

Required Documents

When preparing the 2015 W-3 form, employers need the following documents:

- W-2 Forms: One for each employee, detailing their earnings and taxes withheld.

- Payroll Records: To verify accuracy against the data reported.

- Employer Identification Number (EIN): To ensure the employer is correctly identified.

- Any IRS Notices or Correspondence: If applicable, detailing specific issues or adjustments needed.

Penalties for Non-Compliance

Failure to file the W-3 form accurately, or to meet filing deadlines, can result in penalties from the IRS. In 2015, penalties were imposed based on how late the filing occurred and the employer's annual revenue. The penalties could range from $30 per form to a maximum of $250 per form, depending on the delay length and size of the business. Additionally, providing incorrect or inconsistent information could lead to further fines and require correction filings to rectify any inaccuracies, underscoring the need for meticulous data verification.

Form Submission Methods (Online / Mail / In-Person)

Employers have the option to submit the 2015 W-3 form either online or by mail. Electronic filing is preferred and often recommended due to its efficiency; it can be done through SSA's Business Services Online (BSO). This method offers immediate confirmation and reduces potential errors associated with manual data entry. If filed by mail, the forms should be sent to the SSA's appropriate office, ensuring proper delivery by the specified deadlines. In-person submissions are not an available method, making electronic or postal filing the primary options.

IRS Guidelines for the 2015 W-3 Form

The IRS guidelines for the 2015 W-3 form emphasize the accuracy of information and adherence to submission deadlines. Employers must use official forms without alterations or print them directly from IRS-approved software. The guidelines also detail the importance of using legible, scannable forms for paper submissions to prevent rejection due to quality issues. Employers are encouraged to verify all data against internal records to avoid discrepancies and penalties. Additionally, the IRS provides updates and publications that detail specific filing requirements and changes applicable to that tax year, ensuring compliance with federal tax laws.