Definition & Meaning

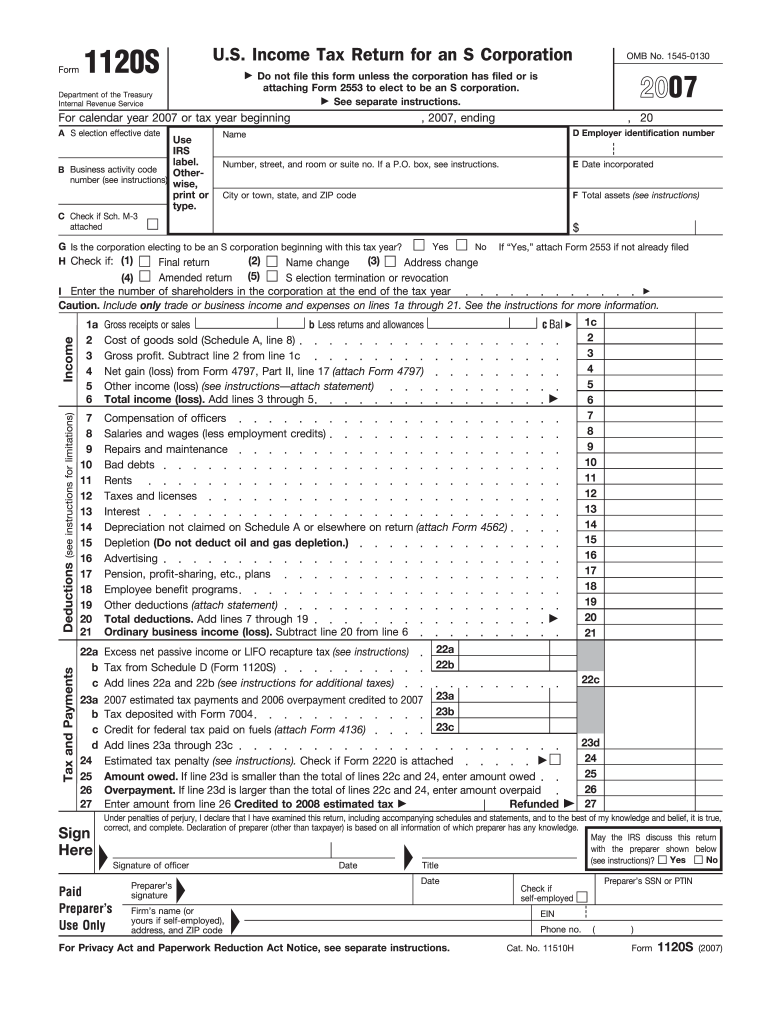

Form 1120S for the tax year 2007 is the U.S. federal income tax return used by S Corporations to report their financial activity. This tax document is pivotal for companies that have elected to be taxed under Subchapter S of the Internal Revenue Code, a status that allows income, losses, deductions, and credits to pass directly to shareholders, avoiding double taxation at the corporate level.

Characteristics of an S Corporation

- Pass-Through Taxation: Profits and losses pass through to shareholders, who report them on personal tax returns.

- Limited Liability: Shareholders have protection from business debts beyond their investment.

- Compliance Requirements: Must file Form 2553 to elect S corporation status with the IRS.

Essential Sections of Form 1120S

- Income Reporting: Sections to declare income from sales, products, and services.

- Deductions and Credits: Offers a comprehensive outline of allowable deductions, including operating expenses, salaries, and other corporate deductions.

How to Use the Form 1120S 2007

Guidance for Effective Filing

- Prepare Required Documents: Gather financial statements, proof of income, expense records, and previous tax returns.

- Fill Accurate Information: Precise income and deduction details are crucial. Include shareholder data and corporate ID numbers.

- Utilize Professional Help: Consult with a tax professional or accountant familiar with corporate filings.

Detailed Income and Deductions

- Revenue Streams: Includes line sections for gross receipts and sales. Accurate allocation between ordinary income and other income streams is necessary.

- Deductions Specificity: Accurately calculate salaries, wages, and any employment benefits granted.

Steps to Complete the Form 1120S 2007

- Start with Company Identification: Fill in the company's name, address, and unique EIN.

- Enter Shareholder Information: Precise entries for shareholder names, addresses, and share percentage.

- Complete Income Sections: Detail all income sources and any applicable credits.

- Calculate and Enter Deductions: Include expenses such as rent, wages, and utilities.

- Validate Balance Sheet Entries: Ensure that balance sheets reconcile with books.

Cross-Check with Form Instructions

- Ensure all figures align with accompanying instructions provided by the IRS.

- Double-check for any updates or nuances specific to the 2007 tax year.

Key Elements of the Form 1120S 2007

Main Components

- Page 1 - Income and Deductions: Captures the core financial details such as total income and applicable deductions.

- Schedule K: Lists income, credits, and other shareholder insights.

- Schedule M-1 and M-2: Reconciliation of income (loss) per books with income (loss) per return and analysis of unappropriated retained earnings.

Important Considerations

- Balance Sheet on Schedule L: Reflects the end-of-year financial positions.

- Distribution Details: Ensure post-filing shareholder distributions are accurately reported.

IRS Guidelines

Compliance Requirements

- Filing with the IRS: Submit Form 1120S to the IRS by the 15th day of the third month after the tax year ends, typically March 15.

- Record Keeping: Maintain comprehensive records to support entries.

Amendments and Corrections

- Procedure for Amendments: Use Form 1120X to amend or correct any filed return mistakes.

- Documentation Support: Keep copies of all supporting documents for possible future audits.

Filing Deadlines / Important Dates

- Regular Submission Deadline: March 15, 2008, for calendar year filers.

- Extension Requests: Possible extensions with Form 7004, granting an additional six months.

Considerations for Timely Filing

- File early to avoid penalties.

- Arrange electronic filing to expedite the process.

Who Typically Uses the Form 1120S 2007

Eligible Business Entities

- S Corporations Exclusively: Businesses that have filed Form 2553 for S Corporation status.

- Corporations Seeking Pass-Through Benefits: Businesses preferring income to be taxed at individual rather than corporate rates.

Typical Company Profiles

- Small to medium-sized enterprises (SMEs) utilizing pass-through benefits.

- Real estate businesses and service-based companies often find the structure advantageous.

Penalties for Non-Compliance

Understanding Consequences

- Late Filing Penalties: Calculated per month based on the number of shareholders.

- Underreporting Penalties: Imposed for significant discrepancies between true financial status and tax return content.

Avoiding Penalties

- Adhere to all deadlines.

- Assure accurate and complete information submission.

Digital vs. Paper Version

Comparing Filing Methods

- Digital Filing: Efficient and expedient, allowing autofill features and error checks.

- Paper Filing: Traditional approach with potential for manual entry errors.

Advantages of Electronic Filings

- Saves time and reduces error potential.

- IRS acknowledges receipt promptly, streamlining the process.

Required Documents

Essential Documentation

- Shareholder Agreements: Statements supporting income division.

- Financial Records: Income statements, balance sheets, and expense logs.

- Previous Tax Returns: To guide accurate current-year reporting.

Setting Up for Success

- Assemble documents before beginning to ensure an efficient filing process.

- Confirm each document's relevance to the form's sections.