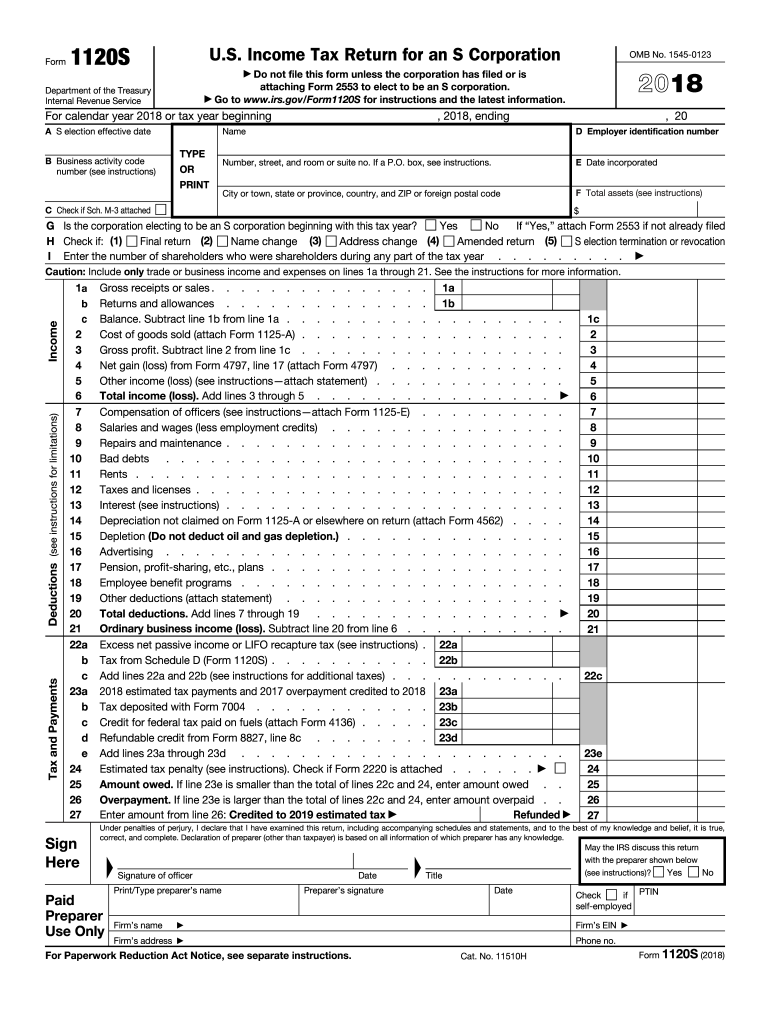

Understanding the 2S Form

The 2017 Form 1120S is a U.S. Income Tax Return form exclusively for S Corporations. It serves to report the financial outcomes of an S Corporation, detailing income, deductions, and other pertinent financial information. Key to using this form is ensuring your business has elected S Corporation status by filing Form 2553 with the IRS. This establishes the flow-through tax nature of S Corporations, allowing income to pass directly to shareholders without being taxed at the corporate level.

How to Use the 2S Form

To effectively use the 2S form, it is vital to understand its structure and requirements:

- Income and Deductions

- Accurately report the corporation's gross income and deduct any allowable expenses.

- Shareholder Information

- Include information about the shareholders’ shares of income, credits, and deductions.

- Schedules and Attachments

- Fill out required schedules, such as Schedule K-1, to document income distribution to shareholders.

Each section must be completed with precision to ensure compliance with IRS standards.

Steps to Complete the 2S Form

Filing the 2S form involves multiple steps:

- Gather Required Information

- Collect financial records, shareholder details, and any previously filed forms like Form 2553.

- Fill Out General Information

- Enter the S Corporation’s name, address, and EIN on the form.

- Report Income and Deductions

- Complete Part I to report total income and allowable deductions.

- Provide Shareholder Details

- Fill in details for each shareholder, including their share of the corporation's income or loss.

- Review and Submit

- Thoroughly review the form for accuracy, attach necessary schedules, and submit by the deadline.

Important Terms Related to the 2S Form

Certain key terms are integral to understanding the 2S Form:

- S Corporation: A corporation that elects to pass corporate income, losses, deductions, and credits to their shareholders for federal tax purposes.

- EIN: Employer Identification Number, a unique number assigned by the IRS to business entities operating in the United States.

- Schedule K-1: A document used to report income, deductions, and credits to shareholders.

Eligibility Criteria for Using the 2S Form

Eligibility for filing the 2S form requires:

- A valid election to be taxed as an S Corporation, confirmed through Form 2553.

- Not having more than 100 shareholders.

- Having shareholders who are exclusively individuals, certain trusts, or estates.

- Being a domestic corporation.

Filing Deadlines and Important Dates

For the 2017 tax year, the key filing deadline for Form 1120S is:

- March 15, 2018: The standard deadline for filing, with considerations for extensions available until September 15, if necessary.

Penalties for Non-Compliance

Failure to file the 2S form on time or inaccuracies can result in penalties:

- Late Filing Penalty: A penalty for failing to file by the due date, currently set at $210 per month per shareholder.

- Inaccuracy: Penalties may also apply if the form is completed inaccurately and leads to underpayment of taxes.

Digital vs. Paper Version

While the 2S form can be filed either digitally or via paper, each method has distinct considerations:

- Digital Filing: Offers convenience and faster processing. It is compatible with tax software like TurboTax.

- Paper Filing: Necessary if electronic filing is not an option, requiring submission through mail to the designated IRS address.

Software Compatibility

The 2S form is fully compatible with leading tax preparation software such as:

- TurboTax and QuickBooks: Use these programs to ensure accuracy and streamline the filing process for S Corporations.

These platforms often guide the user through the completion process, reducing the likelihood of errors.

Business Types That Benefit Most from the 2S Form

Small to medium-sized businesses that:

- Desire pass-through taxation to avoid double taxation seen in C Corporations.

- Have less than 100 shareholders.

- Seek a simplified reporting structure for financial results.

These characteristics make the 1120S form ideal for businesses wanting the benefits of limited liability combined with potential tax advantages.