Definition & Meaning

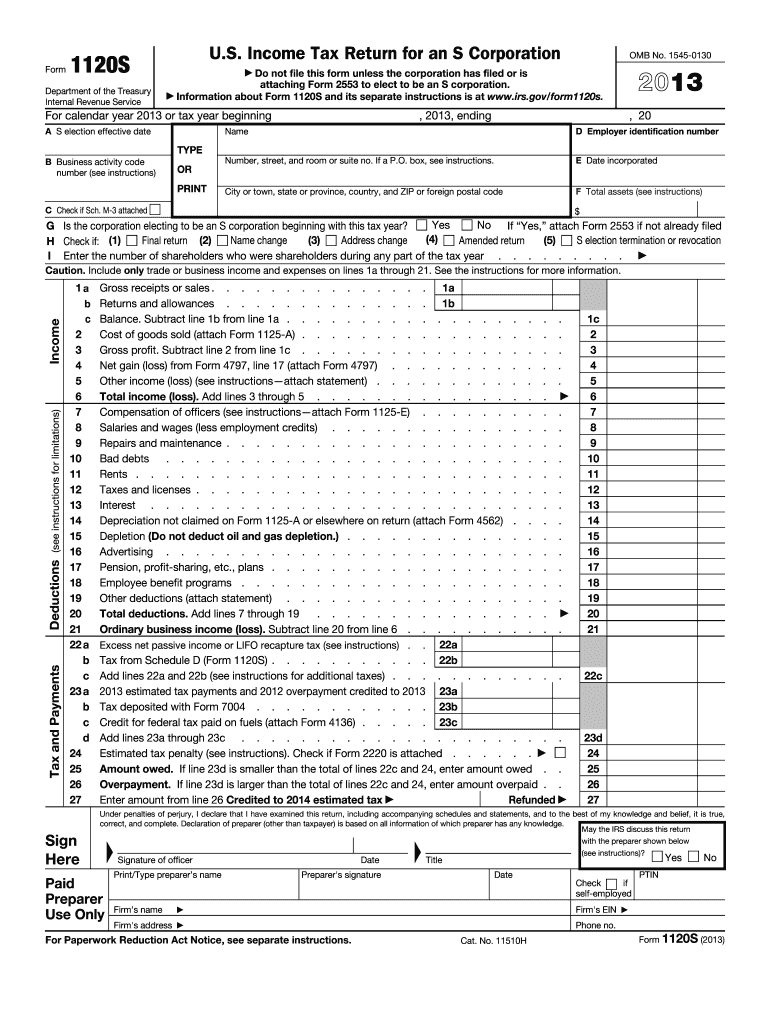

The "1120S" form, officially known as the "U.S. Income Tax Return for an S Corporation," is a tax document issued by the Internal Revenue Service (IRS) in the United States. The 2013 version of this form remains specific to that tax year, capturing financial activities of S corporations, which are entities that elect to pass corporate income, deductions, and credits through to their shareholders. The shareholders in turn report these on their personal tax returns. This mechanism helps S corporations avoid double taxation, a significant benefit within the U.S. tax system.

How to Use the 1120S 2013 Form

Filing the 1120S 2013 form requires tracking and documenting various financial aspects of an S corporation. The primary function is to report the corporation’s income, losses, deductions, and credits. Shareholders use the reported information to include on their tax returns (Form 1040). The form dictates where and how each piece of financial data should be recorded, ensuring consistency and compliance with IRS guidelines. Incorrect usage or errors can result in penalties, highlighting the form's importance in accurate tax filing.

Steps to Complete the 1120S 2013 Form

-

Gather Necessary Financial Documents:

- Profit and loss statements

- Balance sheets

- Records of income and deductions

-

Fill Out Corporate Details:

- Name and address

- Employer Identification Number (EIN)

- Date of incorporation

-

Report Income:

- Total income for the corporation

- Include sales, received services, and other income sources

-

Calculate Deductions:

- Operating expenses

- Employee wages and benefits

- Office and administrative expenses

-

Calculate Shareholder Allocation:

- Dividend distributions

- Individual share percentages

-

Review and Submit:

- Double-check calculations and entries

- Submit by the annual deadline

Important Terms Related to 1120S 2013 Form

- Pass-Through Taxation: Refers to the tax mechanism where earnings are passed directly to shareholders to report on their tax returns, avoiding corporate taxation.

- Schedule K-1: This is part of the 1120S form used by shareholders to report income, deductions, credits, etc.

- Shareholder: A person or entity owning shares in an S Corporation, responsible for reporting their share of income.

Filing Deadlines / Important Dates

The 1120S form for the 2013 tax year was due by March 15, 2014, for calendar-year filers. For those unable to meet this deadline, filing Form 7004 provided a six-month extension, moving it to September 15, 2014. Adhering to these deadlines is crucial to avoid IRS penalties and ensure compliance with federal regulations. Meeting extensions requires payment of expected taxes.

Penalties for Non-Compliance

Failing to file the 1120S form or doing so inaccurately can result in significant penalties. The IRS imposes a monthly fine for unfiled tax returns, which can be a burden for small corporations. Errors in the form or late submissions can result in audits or increased scrutiny. These penalties underscore the importance of using accurate financial data and adhering to submission timelines.

Business Types that Benefit Most from 1120S 2013 Form

S corporations are the primary users of the 1120S form, which stands to benefit from its pass-through taxation system. Of particular advantage are small to medium-sized businesses that want to avoid double taxation while allowing profit-sharing among shareholders. While larger entities can convert to S Corp status for tax purposes, this structure best suits those with straightforward financial arrangements.

Required Documents

To complete the 1120S form, corporations need to collect several documents:

- Yearly financial statements

- Record of dividends paid

- Documentation of business expenses

- Prior year's tax returns for reference

- Shareholder information, including ownership percentages

Having these documents on hand before starting the form ensures a smoother, more precise filing process.