Definition & Meaning

The 1120S 2014 form is the official U.S. Income Tax Return for an S Corporation, as mandated by the Internal Revenue Service (IRS). This form is used by S corporations to report their financial activities, including income, deductions, gains, losses, and credits, for the 2014 tax year. By filing the 1120S form, S corporations comply with federal tax regulations, providing transparency and accountability regarding their financial status.

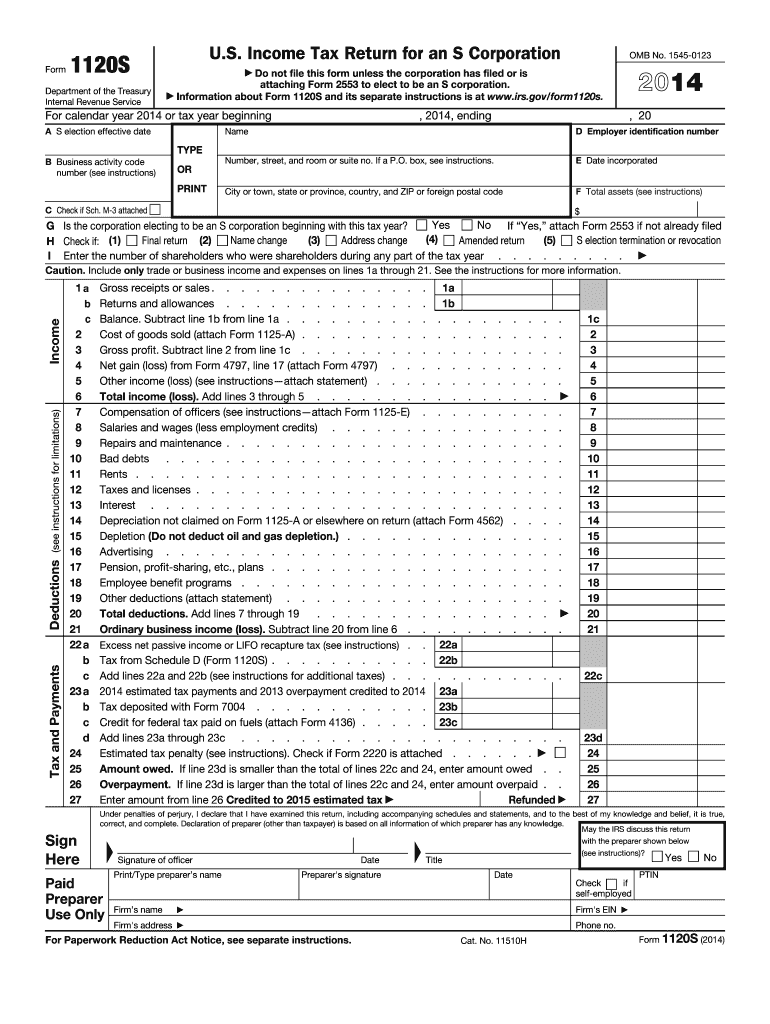

How to Use the 1120S 2014 Form

To accurately use the 1120S 2014 form, S corporations need to gather pertinent financial information from the tax year 2014. Here’s a general procedure:

- Collect necessary financial documents: Gather records of all income, expenses, and other financial activities during the tax year.

- Complete the form sections: Fill in sections related to corporate details, income, deductions, shareholder information, and other required details.

- Review for accuracy: Double-check each entry to ensure compliance and accuracy in reporting.

- File the form with the IRS: Submit the completed form following the chosen submission method, ensuring it reaches the IRS by the due date.

Steps to Complete the 1120S 2014 Form

Completing the 1120S 2014 form involves several steps, including:

- Corporate Information: Provide basic details such as the corporation’s name, address, Employer Identification Number (EIN), and date of incorporation.

- Income and Deduction Details: Report all gross receipts, sales, and other forms of income. Deduct ordinary and necessary business expenses to arrive at the taxable income.

- Shareholder Information: Itemize dividend distributions and shareholder compensation to reflect how profits are shared among shareholders.

- Tax and Payments: Calculate taxes and payments made during the year, including estimated payments or overpayments from previous years.

Who Typically Uses the 1120S 2014 Form

The 1120S 2014 form is primarily used by S corporations, which are corporations that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. These entities are typically small to medium-sized businesses structured to benefit from limited liability while avoiding double taxation. Shareholders report the income and losses on their personal tax returns, thus allowing the income to be taxed at personal tax rates.

Key Elements of the 1120S 2014 Form

Understanding the key components of the 1120S 2014 form is crucial for correct filing:

- Schedule K-1: Reports each shareholder's share of the corporation’s income, deductions, and credits.

- Schedule L: A balance sheet outlining the corporation’s assets, liabilities, and shareholder equity.

- Schedule M-1: Reconciles income per books with income per return, explaining any differences.

- Schedule M-2: Tracks changes in the corporation's retained earnings over the fiscal year.

Filing Deadlines / Important Dates

For the tax year 2014, the 1120S form must be filed by March 15, 2015. If the corporation operates on a fiscal year other than the calendar year, the form is due on the 15th day of the third month following the end of the fiscal year. If more time is needed, filing for an extension using the appropriate IRS form can provide an additional six months, pushing the deadline to September 15, 2015.

Required Documents

To prepare and file the 1120S 2014 form, S corporations need the following documents:

- Previous year’s tax returns.

- Detailed profit and loss statements.

- Comprehensive balance sheet.

- Records of all income, expenses, dividends, and distributions.

- Documentation of estimated tax payments and any tax credits claimed.

Penalties for Non-Compliance

Failing to timely file the 1120S 2014 form or file accurately can lead to penalties. Common penalties include:

- Late Filing Penalty: Typically a penalty for each month or part of a month the return is late, multiplied by the number of shareholders.

- Accuracy-Related Penalty: This applies if the corporation underpays due to negligence or disregarding rules.

- Failure to Pay Penalty: Imposed on any unpaid tax by the original due date, regardless of extensions.

IRS Guidelines

The IRS provides comprehensive guidelines that outline how to complete the 1120S 2014 form, the requirements for electing S corporation status, and the criteria to maintain that status. It also includes instructions for reporting various types of income and deductions, ensuring compliance with federal tax laws. These guidelines are essential for avoiding errors and ensuring the proper filing of the corporate tax return.