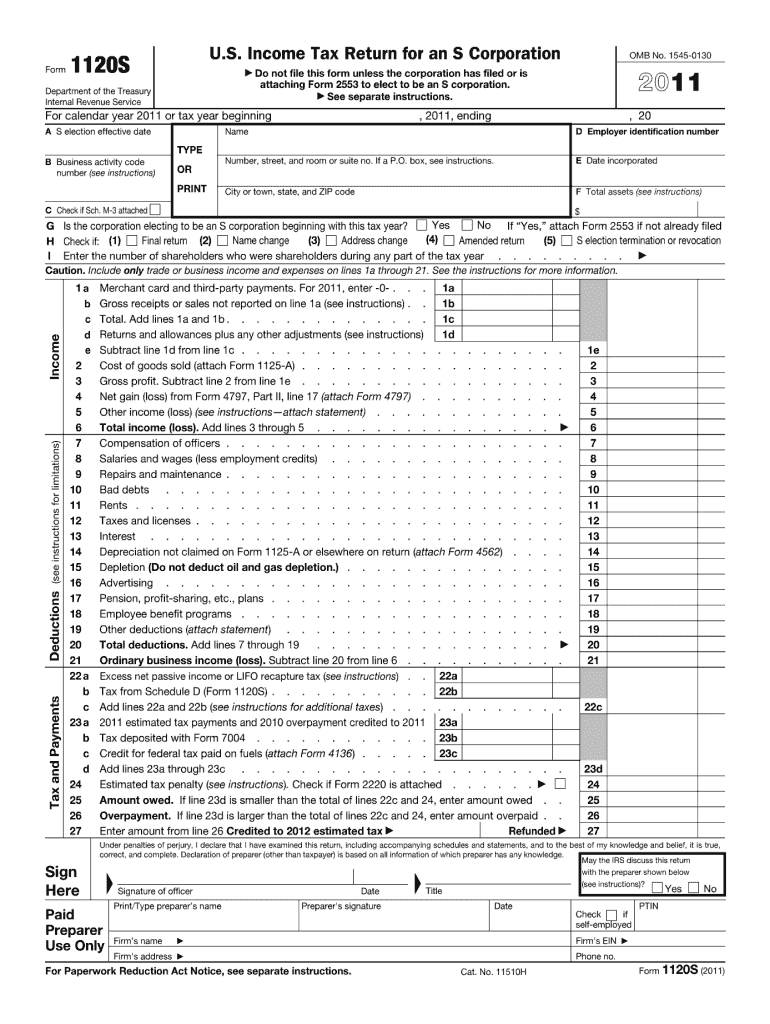

Overview and Purpose of the 2011 Form S

The 2011 Form S is an essential document designed for entities looking to make an S election, thereby allowing corporations to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. This is beneficial as it avoids double taxation on the corporate income. To fully understand the 2011 Form S, it's crucial to explore its purpose thoroughly and the specific scenarios under which it applies. Typically, this form is used by domestic corporations that meet certain criteria and wish to be taxed as an S corporation. The form helps streamline tax processes for qualifying corporations, ensuring compliance with IRS regulations.

How to Obtain the 2011 Form S

Obtaining the 2011 Form S can be achieved through several straightforward methods. This form is available for download on the Internal Revenue Service (IRS) website, ensuring easy digital access for users. Alternatively, companies can request a physical copy by contacting the IRS directly. Businesses may also work with their tax advisors or accountants to secure the form, along with guidance for its completion. It's important to note that having the right version is crucial, as any errors can delay the S election process.

Steps to Complete the 2011 Form S

-

Gather Required Information: This includes the corporation's name, address, and tax year beginning and ending dates.

-

List Shareholder Details: Provide information about each shareholder, including names, addresses, and social security numbers. Each shareholder must agree to the S corporation election.

-

Complete Entity Details: Input the employer identification number (EIN) and the date the corporation was formed.

-

Tax Year and Election: Specify the elected tax year. The corporation ordinarily must adopt the calendar year unless it can show that a different tax year is business-appropriate.

-

Sign and Date the Form: The document must be signed by an officer of the corporation.

Completing this form with accuracy is vital to ensure a smooth election process. Mistakes can lead to processing delays or rejections.

Key Elements of the 2011 Form S

Certain components of the 2011 Form S are pivotal. These include:

-

Corporation Information: Basic details regarding the corporation must be filled in, serving as the foundation for the document.

-

Shareholder Agreement: All shareholders need to sign the consent statement.

-

Entity Elections: Choices regarding accounting and tax years should be clearly marked.

Understanding these elements ensures comprehensive completion of the form, reducing risks of errors.

Who Typically Uses the 2011 Form S

The 2011 Form S is generally used by domestic small business corporations that comply with specific criteria to be taxed under Subchapter S of the Internal Revenue Code. These businesses must have no more than 100 shareholders, all of whom must be eligible individuals. Moreover, the form is commonly utilized across various entities wanting to mitigate the risk of double taxation on corporate income, thus maximizing their tax efficiency.

Business Entity Types Benefiting from the 2011 Form S

-

Small Corporations: Particularly those looking for tax efficiencies by avoiding double taxation.

-

Qualified Trusts and Estates: Entities under certain conditions also find advantage in S corporation election.

-

Partnerships: Where shareholders wish to pass income directly to personal income tax returns.

These entities benefit significantly from the tax pass-through capability that the S election permits.

Legal Use of the 2011 Form S

The 2011 Form S has critical legal implications. Adhering to its guidelines ensures that the election complies with the IRS standards. It's crucial for businesses opting for S corporation status to understand the legalities involved, including maintaining qualification standards and following precise documentation procedures. Non-compliance can lead to legal ramifications including denial of the S election status. Thus, professional guidance is often recommended.

Penalties for Non-Compliance with the 2011 Form S

Failure to properly file the 2011 Form S can result in serious consequences for businesses. Penalties may include the IRS viewing the corporation as a C corporation, leading to double taxation on profits. Additionally, incomplete or incorrect forms can cause the IRS to revoke S status, creating further tax complications. To mitigate these risks, businesses should ensure that all requirements are meticulously followed, and consider using a tax advisor for expert assistance.

By focusing on these essential aspects, users of the 2011 Form S can navigate the process effectively, ensuring compliance and optimizing their tax positions.