Definition and Purpose of Form

Form 709 is officially known as the "United States Gift (and Generation-Skipping Transfer) Tax Return." It is used to report gifts subject to tax during the calendar year 2015. This form ensures compliance with federal regulations regarding gift taxes and provides a structured way for individuals to detail gifts given to others, including generation-skipping transfers to grandchildren or further descendants. The documentation of these gifts helps the IRS track gift tax liability and apply any applicable credits.

How to Obtain Form

Form 709 for the year 2015 can be obtained through the official IRS website, where it is available for download in PDF format. Additionally, various tax preparation software programs, such as TurboTax and QuickBooks, offer options to access the form as part of their filing services for federal taxes. Even though the form can also be requested at local IRS offices, accessing it online or via tax software provides a more streamlined and efficient process.

Steps to Complete Form

- Personal Information: Begin by entering your personal details, including name, address, and taxpayer identification number.

- Gifts and Transfers: Report all gifts given in 2015, providing details about the recipients and the value of the gifts.

- Deductions and Credits: Calculate allowable deductions, such as the annual exclusion amount, and apply any applicable credits.

- Tax Calculation: Follow the form’s instructions to compute the taxable amount of the gifts and determine any tax due.

- Sign and Submit: After ensuring all entries are correct, sign the document and prepare it for submission to the IRS.

Forms must be filled out precisely, as inaccuracies can result in processing delays or penalties.

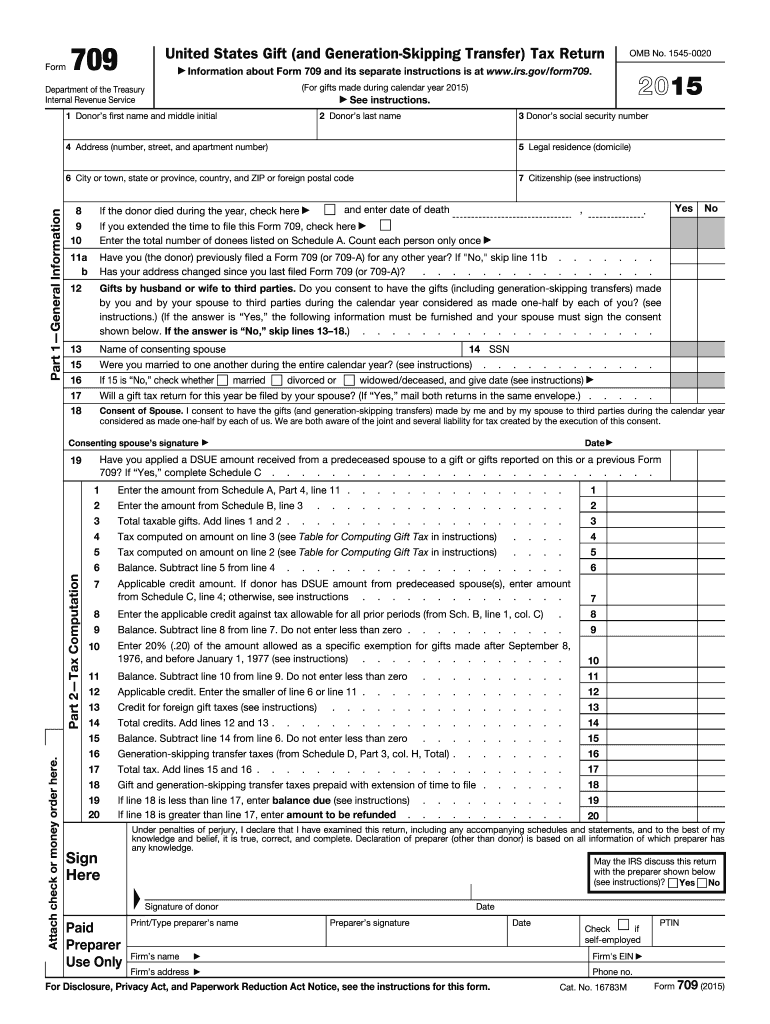

Key Elements of Form

- Part 1: General Information about the donor, including citizenship status and residency.

- Part 2: Reconciliation of the total gifts given against any exclusions and deductions.

- Schedules A and B: Detail specific gifts, providing information about the property given, valuation, and recipient identities.

- Schedule C: Provides a summary of gift tax computations, where applicable credits are documented.

- Part 3: Documentation of generation-skipping transfers, if applicable.

Each section of the form addresses different elements of gift reporting and requires detailed attention to ensure compliance.

IRS Guidelines on Form

The IRS provides extensive guidelines to assist in the completion of Form 709. These guidelines explain the intricacies of federal gift tax laws, annual exclusions, and how to appropriately calculate the value of gifts. The IRS publication on gift taxes should be reviewed in conjunction with the form to ensure a clear understanding of compliance requirements. The guidelines also highlight the necessity of using fair market value for all reported gifts and stipulate how to handle gift-splitting between spouses.

Filing Deadlines and Important Dates

For the 2015 tax year, Form 709 was required to be filed by April 18, 2016, aligning with the federal income tax return deadline. Extensions for filing can be requested using IRS Form 8892, while payment extensions require the use of Form 4768. Missing filing deadlines can lead to penalties, so timely submission is critical.

Required Documents for Form

Every form submission should be accompanied by:

- Valuation Documentation: Appraisals or assessments confirming the fair market value of the gifts.

- Gift Agreements/Contracts: Legal documents that constitute or describe the gift transaction.

- Spousal Consent Forms: Where applicable, documented agreements for gift-splitting.

Gathering and organizing these documents ahead of time ensures a accurate reporting and expedites the filing process.

Penalties for Non-Compliance

Failure to properly complete or timely file Form 709 can result in significant fines and interest charges. Additionally, incorrect reporting of gift taxes can lead to increased scrutiny by the IRS, additional penalties, and potential audits. For instance, intentionally failing to disclose taxable gifts can result in a penalty up to 30% of the tax due. Taxpayers are encouraged to seek clarification or expert advice if unsure about compliance requirements.

Legal Use of Form

Form 709 is legally mandated under the Internal Revenue Code for individuals who exceed the annual exclusion limit for gifts, ensuring correct tax assessments on transferred wealth. It serves as a legal record of gift-giving and tax obligations, making it essential for financial planning, estate planning, and the accurate calculation of tax liabilities tied to gifts. Taxpayers should ensure the form is completed accurately and submitted prudently to align with legal standards and IRS expectations.