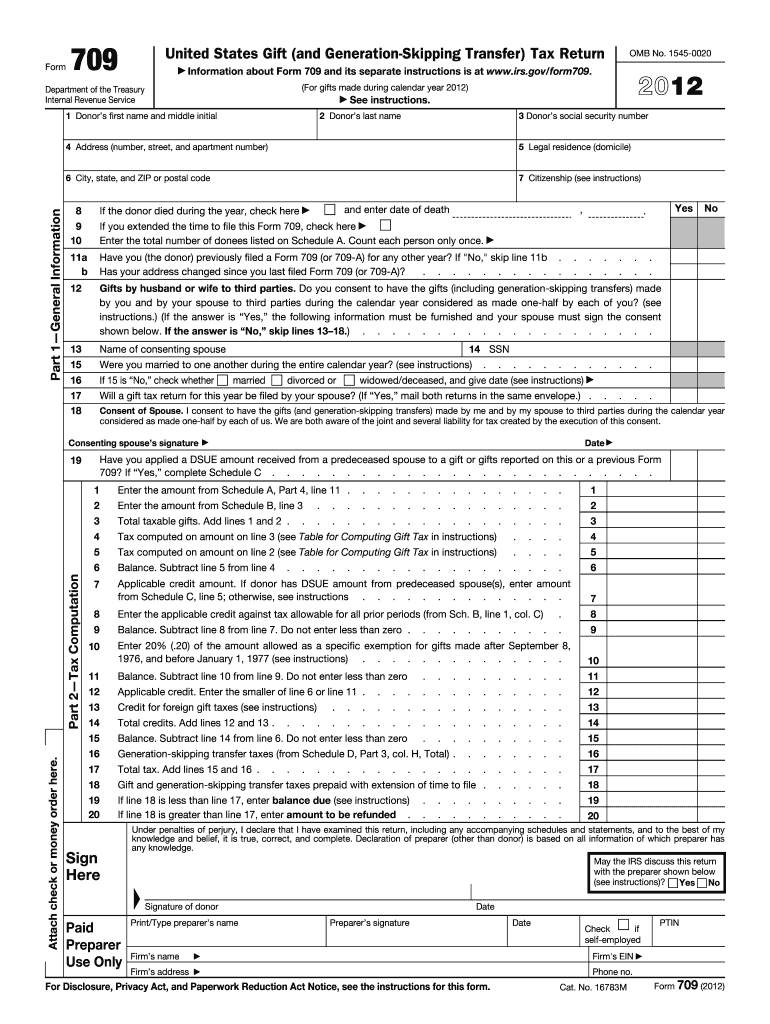

Understanding the 709 Form 2012

The 709 form 2012 is critical for individuals in the U.S. who need to report gifts given during the calendar year under the United States Gift (and Generation-Skipping Transfer) Tax Return. Primarily used to disclose the value of gifts and ensure proper taxation, it includes sections detailing the identity of donors and donees, values of gifts, marital deductions, and applicable tax credits.

Purpose and Importance

- Documentation of Gifts: Ensures gifts are properly documented to meet IRS requirements.

- Tax Compliance: Aids in compliance with gift tax laws, preventing errors or omissions.

- Generation-Skipping Transfers: Captures transfers that skip a generation, specific to IRS needs.

Legal Use of the 709 Form 2012

- State-specific regulations necessitate understanding local requirements to achieve compliance.

- The form adheres to federal tax laws by documenting gifts exceeding the annual exclusion amount.

- Legal consequences exist for inaccurate or incomplete reporting, emphasizing the necessity of precision.

How to Use the 709 Form 2012

Comprehending the use of the 709 form 2012 involves understanding its different sections and requirements:

- General Information: Input and verify donor and donee details, ensuring accurate record keeping.

- Gift Details: Specify any gifts transferred, including descriptions and fair market values.

- Tax Calculations: Use applicable worksheets to calculate any due taxes, ensuring accuracy.

- Schedule A: Complete to delineate taxable gifts and any deductions or credits applied.

- Example: When gifting appreciated property, report the fair market value rather than the original purchase price.

How to Obtain the 709 Form 2012

Accessing the 709 form 2012 for filing purposes can be done through several channels:

- Online Resources: The IRS website offers digital forms which can be downloaded and printed.

- Tax Software: Platforms such as TurboTax may include this form within their suite for supported years.

- Professional Preparation Services: Utilize CPAs or tax professionals who often have historical forms available.

Steps to Complete the 709 Form 2012

The completion of the form requires careful attention to detail to ensure all information is precise:

- Gather Information: Collect financial records, including appraisals or valuations of gifts.

- Fill Out Donor Section: Provide your personal information and address any marital adjustments.

- Report Each Gift: Accurately detail each gift within the specified areas of the form.

- Calculate Tax: Use IRS worksheets to calculate the gift tax liability accurately.

- Review and Sign: Ensure all information is complete before signing and submitting to the IRS.

- Practical Tip: Double-check marital status as it can impact deductions and transfer amounts.

Who Typically Uses the 709 Form 2012

The form is utilized by various individuals and entities when specific conditions are met:

- Individuals with Large Gifts: Used by those gifting over the annual exclusion amount.

- Estate Planners: Professionals managing estates may also file to pre-organize wealth transfers.

- Advisors to High-Net-Worth Individuals: Clients with significant assets require this form for tax planning.

IRS Guidelines for 709 Form 2012

The IRS offers comprehensive guidelines to assist taxpayers in their reporting duties:

-

Publication 559: Offers insight into estate and gift tax regulations, guiding correct form use.

-

Instruction Manuals: Detailed instructions accompany the form for step-by-step completion assistance.

-

FAQs and Help Desks: Online resources provide additional support for questions arising during filing.

-

Example Scenario: Donating significant wealth to a relative’s education fund should be reported as per IRS gifting rules.

Filing Deadlines and Important Dates

Understanding deadlines is crucial for timely compliance:

-

Annual Filing Deadline: Typically due by April 15th, aligning with the federal tax filing deadline.

-

Extension Forms: Utilize Form 4868 if extra time is needed to prepare the form thoroughly.

-

Important Exception: If April 15th falls on a weekend or holiday, the deadline may shift to the next business day.

Examples of Using the 709 Form 2012

Illustrative scenarios can help clarify form usage:

- Example 1: A donor gives $50,000 to a nephew for educational expenses in 2012, requiring them to report this amount as it exceeds the exclusion limit.

- Example 2: Multiple gifts to different family members each over the annual limit, necessitating use of several Schedule A forms.

Understanding these real-world scenarios ensures the 709 form is filled accurately and comprehensively.