Definition and Purpose of Form 709

Form 709, the United States Gift (and Generation-Skipping Transfer) Tax Return, is a critical tax document used by U.S. taxpayers to report gifts given that exceed the annual exclusion. The form also addresses generation-skipping transfer taxes, which apply when property is passed to a beneficiary at least two generations younger than the donor, such as grandchildren. This form serves as a means to both document taxable gifts and compute potential tax liabilities.

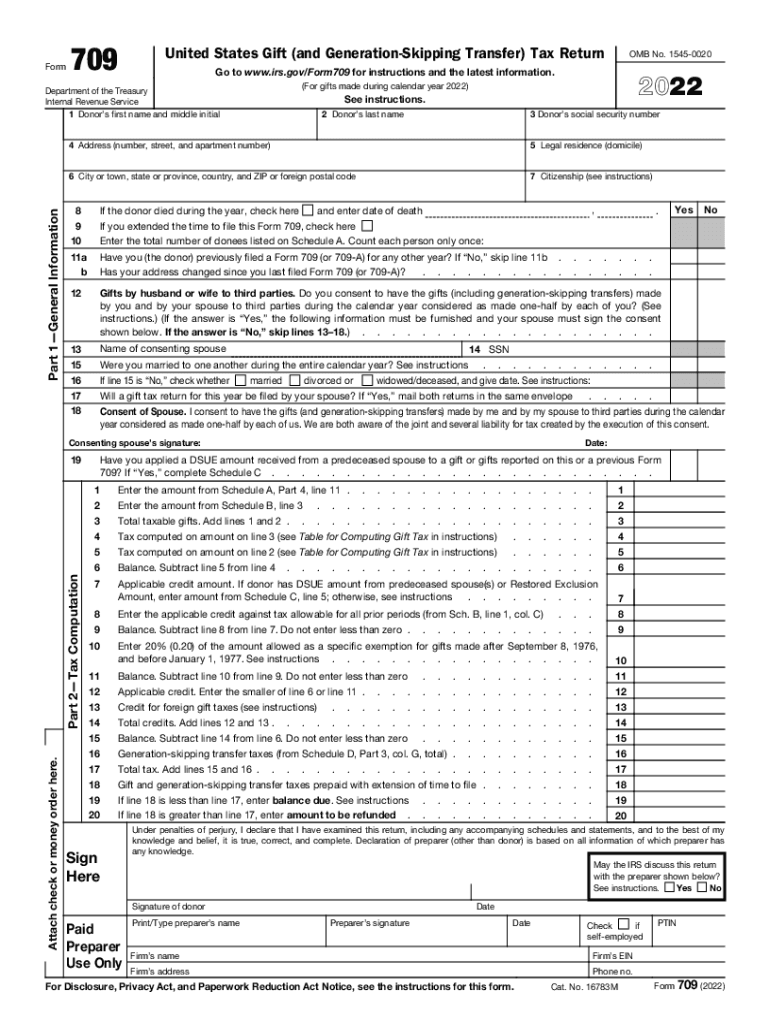

Key Elements of Form 709

-

Donor Information: Includes personal information about the individual giving the gift, such as name, address, and taxpayer identification number.

-

Tax Computation: This section is crucial for calculating any applicable gift tax. It involves summing previous lifetime gifts that count toward gift and generation-skipping transfer taxes.

-

Schedules and Attachments: Various schedules are part of the form, detailing specific gift amounts, relationship with donee, and property description. Notable are Schedule A for taxable gifts and Schedule B for prior gifts.

-

Generation-Skipping Transfer Tax: Part III of the form focuses on transfers where the donee or beneficiary is two or more generations removed from the donor.

Required Documents for Completing Form 709

To accurately fill out Form 709, taxpayers need several supporting documents:

-

Detailed List of Gifts: Includes the fair market value of each gift, date of transfer, and description of the property or cash given.

-

Prior Gift Tax Returns: If applicable, previous forms filed regarding lifetime gifts.

-

Appraisals or Valuations: For property or assets gifted, to substantiate claimed value.

-

Legal Documents: Including any gift agreements, contracts, or other documentation that substantiates the nature and terms of the gift.

How to Obtain Form 709 and its Instructions

Obtaining Form 709 and its accompanying instructions is a straightforward process. They are available for download on the Internal Revenue Service (IRS) website. Individuals can also request physical copies by contacting the IRS directly via mail or phone. Ensuring you have the correct form for the tax year in question is crucial for compliance.

Steps to Complete Form 709

-

Gather Necessary Information: Collect all required personal, financial, and gift-related documents.

-

Fill Out Donor Information: Provide comprehensive personal and contact details.

-

Report Gifts and Values: Enter details about each gift, including its fair market value and relationship to the recipient.

-

Calculate Taxes: Use the instructions to compute any gift taxes due, considering applicable exclusions and deductions.

-

Include Additional Schedules: Complete any supplementary schedules applicable to your situation, such as prior gifts or generation-skipping transfers.

-

Review and Submit: Ensure all information is accurate, then file the form by mail to the IRS address specified in the instructions. Note that electronic submissions are not permitted for this form.

Filing Deadlines and Important Dates

Form 709 typically aligns with individual income tax return deadlines. It is due by April 15 of the year following the calendar year in which the gift was made. For those unable to meet this deadline, filing for an extension using Form 4868 can provide additional time to complete their return, although it does not extend payment due dates for any established tax liability.

Legal Use and Compliance for Form 709

Using Form 709 correctly is imperative for adhering to U.S. gift tax laws. Filing the form ensures compliance with IRS regulations governing the disclosure of taxable gifts and generation-skipping transfers. Non-compliance, such as failing to file or inaccurately reporting gift values, can result in significant penalties and interest charges imposed by the IRS.

Penalties for Non-Compliance

Failure to properly complete and submit Form 709 carries several penalties:

-

Late Filing Penalty: Typically 5% of the unpaid tax for each month the return is late, up to a maximum of 25%.

-

Accuracy-Related Penalty: If underpayment arises from negligence or disregard for tax rules, this penalty may apply.

-

Interest on Unpaid Tax: Applied daily, from the due date of the return until payment is made.

Understanding these penalties emphasizes the importance of accurate and timely filing of Form 709 to avoid unnecessary financial consequences.