Definition and Purpose of the 2008 Form 709

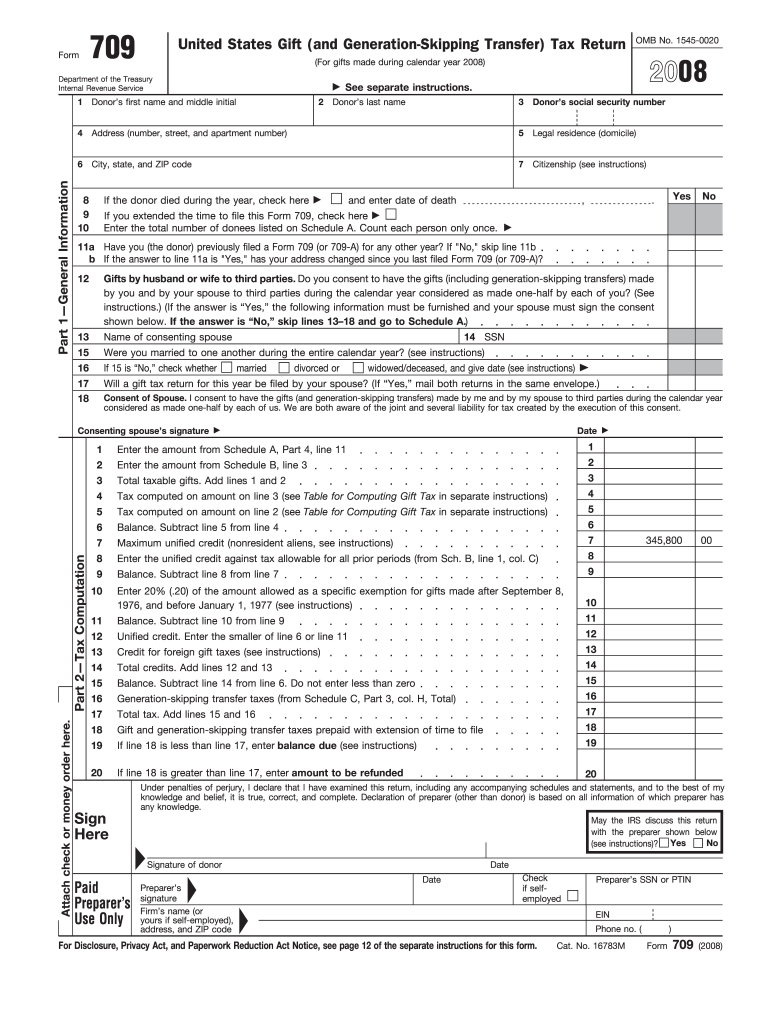

The 2008 Form 709 is the United States Gift (and Generation-Skipping Transfer) Tax Return, crucial for reporting gifts made during the year and calculating any taxes due. This form specifically applies to individuals who have exceeded the annual gift tax exclusion while transferring substantial assets to others. The document ensures compliance with the Internal Revenue Service (IRS) by detailing both taxable gifts and generation-skipping transfers. Understanding its purpose is essential for donors navigating complex tax obligations, highlighting the importance of accurately reporting all relevant transactions for the 2008 tax year.

Obtaining the 2008 Form 709

Acquiring the 2008 Form 709 involves several straightforward steps. The IRS website is the primary source, hosting an archive for past forms available for download in PDF format. Alternatively, tax preparation software may offer the 2008 version, facilitating easier completion with integrated guidance. Individuals seeking physical copies can request documents directly from the IRS via phone or online, with delivery options available through standard mail. Understanding these acquisition methods ensures timely access to the necessary paperwork, allowing taxpayers to prepare their returns efficiently.

Steps to Complete the 2008 Form 709

Completing the 2008 Form 709 necessitates careful attention to detail. Begin by filling out general information about the donor, such as name, address, and taxpayer identification number. The tax computation section follows, requiring details of all gifts exceeding the annual exclusion. Detailed schedules are essential for reporting specific transactions, including generation-skipping transfers. Instructions accompanying the form provide guidance on each section, emphasizing the importance of accuracy. Review the completed form thoroughly before submission to ensure compliance with regulatory requirements and minimize potential errors.

Importance of the 2008 Form 709

The 2008 Form 709 is pivotal for individuals who have made substantial financial gifts, as it facilitates accurate tax reporting and compliance with federal regulations. The form aids in tracking gift amounts against lifetime exemptions, granting clarity on potential tax liabilities. By documenting these transactions, taxpayers uphold their obligations to the IRS, avoiding potential penalties. Highlighting its significance, the form also provides transparency and accuracy in personal financial dealings, ensuring that all substantial gifts are documented legally and comprehensively.

Typical Users of the 2008 Form 709

Typically, individuals engaging in significant financial transactions that involve gifting assets will utilize the 2008 Form 709. The form applies to those exceeding annual gift tax exclusions, generally wealthier individuals or those engaged in estate planning. Parents, grandparents, and business owners distributing assets to family or organizations are common users. Familiarity with the form's requirements allows individuals to make informed decisions, ensuring that all transfers align with federal tax regulations. The form supports those planning their estate while managing impactful financial gifts.

Key Elements to Consider When Filling the 2008 Form 709

Key elements integral to the 2008 Form 709 include:

- General Information: Basic donor details and identification.

- Tax Computation: Section for calculating total gift amounts and associated taxes.

- Detail Schedules: Precise reporting of individual gifts and transfers.

- Signature and Verification: Certification of the form's accuracy by signing manually or electronically. Meticulous attention to these components ensures comprehensive and accurate completion. Missteps in any section can lead to discrepancies, making it imperative to address each element with diligence. The form's complexity necessitates a thorough approach, catered to individuals familiar with tax protocols.

IRS Guidelines for the 2008 Form 709

The IRS guidelines provide a framework for accurately completing the 2008 Form 709. These guidelines specify reporting thresholds for gifts, annual exclusion amounts, and how to compute tax liabilities. Detailed instructions accompany the form, clarifying each section and assisting in accurate completion. Understanding these guidelines is crucial for compliance, as the IRS mandates precise documentation of all pertinent financial transfers. Familiarity with requirements ensures proper filing, reducing the risk of penalties or additional scrutiny.

Deadlines and Important Dates for Filing

Compliance with IRS deadlines is essential for the 2008 Form 709 to avoid penalties. Typically, the form must be filed by April 15 following the gift year, aligning with the federal income tax return deadline. Taxpayers may request an extension with Form 8892, granting additional time but still requiring payment of any owed taxes by the original date. Adhering to these deadlines is crucial, as late submissions may incur interest or additional charges, underscoring the need to prioritize timely filing.

Required Documents to Accompany the 2008 Form 709

Preparation of the 2008 Form 709 necessitates gathering several supporting documents. These include records of all gifts exceeding the annual exclusion, appraisals for non-cash assets, valuations for property transfers, and legal agreements for transfers involving trust funds. Collecting and organizing these documents ensures comprehensive reporting and supports the information declared on the form. Proper documentation is instrumental in verifying the accuracy of submitted data, facilitating smoother processing and approval by the IRS.