Understanding the 2016 Form 709

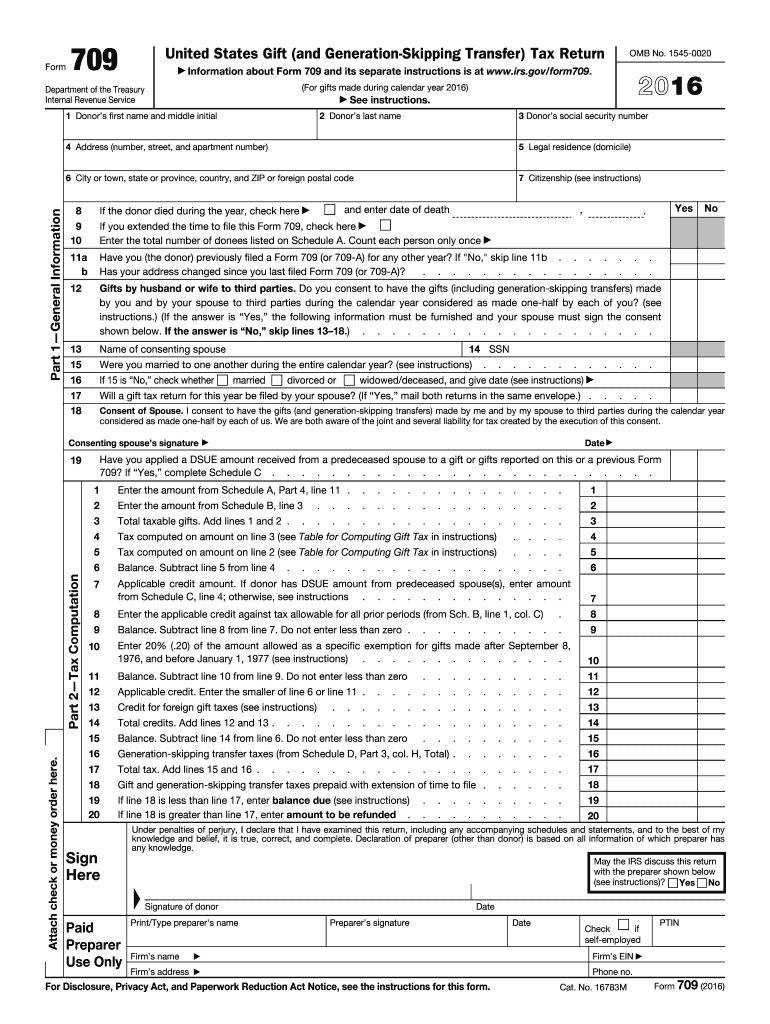

The 2016 Form 709, officially known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is a critical tax document used to report gifts made during a calendar year. Donors must use this form to provide detailed information on gifts, taxable amounts, and applicable deductions and credits related to gift taxes. The form is also essential for reporting generation-skipping transfer taxes, which apply to gifts transferred to individuals more than one generation younger than the donor.

How to Use the 2016 Form 709

Using the 2016 Form 709 requires careful attention to detail, as it involves a comprehensive breakdown of gifts given. Donors will need to record:

- General information about themselves, including the taxpayer identification number.

- The recipients' (donees') information, detailing created gift values.

- Calculations for any tax due, factoring in applicable deductions and credits.

This form serves as a mechanism to ensure compliance with federal gift and transfer tax obligations, mitigating potential future tax liabilities.

Key Steps to Complete the 2016 Form 709

Completing the 2016 Form 709 involves the following essential steps:

- Gather all information related to gifts given within the tax year, including dates, values, and descriptions.

- Fill out your personal information on the form, ensuring accuracy to avoid processing issues.

- Enter details for each gift, such as the donee's information and the valuation of the gift.

- Calculate any applicable deductions and tax credits to determine the total tax liability.

- Review the form for accuracy and completeness before submission.

Important Terms Related to 2016 Form 709

Familiarizing oneself with critical terms related to the 2016 Form 709 is essential for accurate completion:

- Donor: The individual making the gift.

- Donee: The recipient of the gift.

- Gift Tax: A federal tax applied to an individual giving anything of value to another without receiving equivalent value in return.

- Generation-Skipping Transfer Tax: Tax on gifts made to individuals more than one generation younger than the donor.

Filing Deadlines and Important Dates

The 2016 Form 709 is due annually, aligning with the standard tax filing deadline, April 15th. In situations where the deadline falls on a weekend or a public holiday, the next business day becomes the deadline. Extensions may be applied for using IRS Form 4868, granting additional time, typically up to six months, to file the form.

Eligibility Criteria

Individuals who have transferred gifts exceeding the annual exclusion limit or those involving generation-skipping scenarios must file the 2016 Form 709. The IRS sets this annual exclusion limit, which is subject to change each year. It is crucial to verify that gifts fall under the set threshold before determining the necessity of filing.

Required Documents for 2016 Form 709

To accurately file the 2016 Form 709, it is important to gather necessary documentation, including:

- Detailed records of all gifts made, including appraisals for non-cash items.

- Copies of completed gift agreements, if available.

- Documentation supporting the valuations and deductions claimed.

These documents ensure that the information provided on the form is verifiable and substantiated.

IRS Guidelines for 2016 Form 709

Adhering to IRS guidelines is crucial for compliance and avoiding penalties. The IRS provides comprehensive instructions for completing the 2016 Form 709, including guidance on reporting and computations. These instructions can be found on the official IRS website and provide valuable insight into the complexities and nuances of the form.

Penalties for Non-Compliance

Failure to file the 2016 Form 709 when required or inaccuracies in filing can result in severe penalties. These may include monetary fines, additional interest on unpaid tax liabilities, and potential legal implications. It is essential to file accurately and on time to prevent these negative outcomes.

Software Compatibility

Several tax preparation software packages, such as TurboTax or QuickBooks, are compatible with the 2016 Form 709, facilitating efficient and accurate completion. These tools often offer step-by-step instructions, guided calculations, and error checks, although it remains the taxpayer's responsibility to ensure all provided information is complete and correct.

By following these detailed sections and understanding the purpose, requirements, and procedures associated with the 2016 Form 709, taxpayers ensure they meet their legal obligations and minimize potential tax liabilities.