Definition and Purpose of Form 709

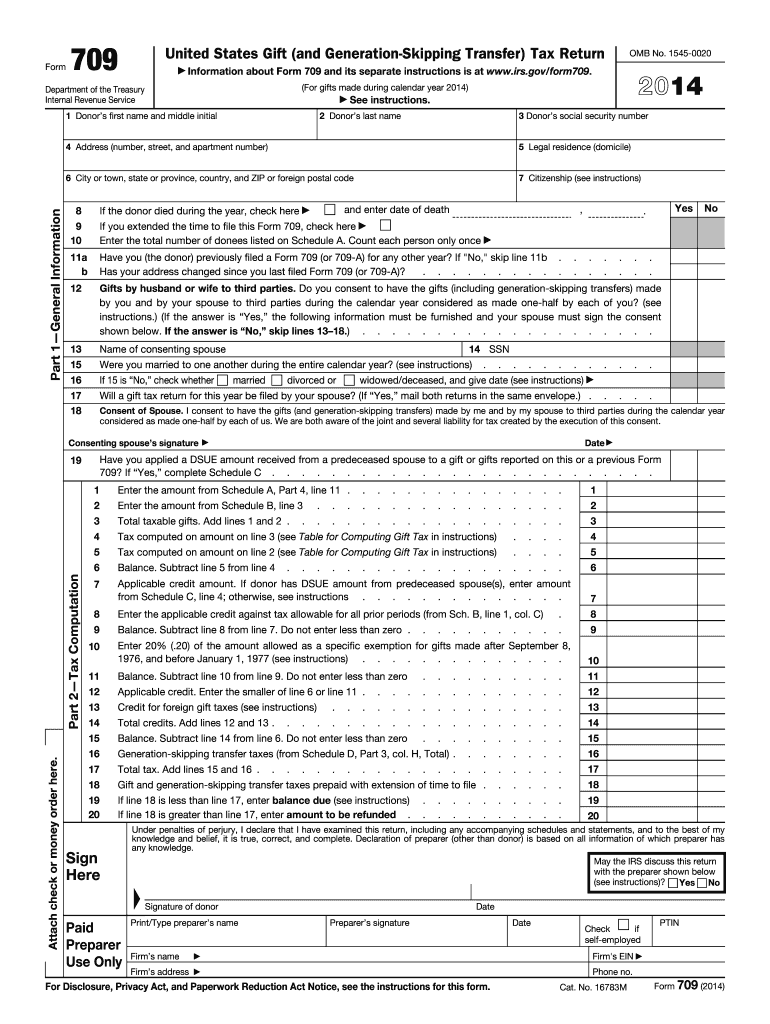

Form 709, officially titled "United States Gift (and Generation-Skipping Transfer) Tax Return," is a federal tax document used to report gifts given by an individual during a calendar year. The form is crucial for calculating any applicable gift taxes and ensuring compliance with IRS regulations. Gift tax applies when a person gives property or money to another individual without expecting fair compensation. The 2014 version covers the reporting requirements for that specific tax year, maintaining the same essential functions and sections present in other iterations.

Primary Function and Context

- Gift Reporting: Form 709 records the details of gifts over the annual exclusion limit, which must be reported to the IRS.

- Generation-Skipping Transfers: It also includes provisions for reporting generation-skipping transfers (GSTs), which involve gifts to recipients two or more generations younger than the donor.

- Gift Splitting: Married couples using gift-splitting must detail this on the form, doubling the exclusion amount allowed per recipient.

Obtaining and Accessing Form 709

Form 709 can be accessed and obtained from several sources, ensuring ease of availability for taxpayers. Both digital and paper versions are provided to accommodate different user preferences and accessibility needs.

Methods of Acquisition

- IRS Website: Direct download from the IRS website is the most straightforward way to obtain Form 709.

- Tax Software: Popular tax preparation software usually includes the form, allowing users to file digitally.

- Local IRS Offices: Paper copies are available at local IRS offices for those who prefer or require a hard copy for record-keeping.

Reasons to File Form 709

Understanding why this form is essential highlights the necessity of timely and accurate filing. The form serves more than regulatory compliance; it can be a strategic component in personal tax planning.

Key Considerations

- Tax Avoidance Strategy: Proper filing helps avoid gift tax penalties and optimizes estate tax planning.

- Legal Requirement: Filing is mandated when gifts exceed the annual exclusion, ensuring legal compliance.

- Gift Splitting Advantages: Allows married couples to maximize their tax benefits through gift splitting.

Steps to Complete Form 709

Completing Form 709 involves several steps, requiring attention to detail to ensure accuracy and compliance.

Detailed Procedure

- Gather Required Documents: Collect financial statements, appraisals, and prior year tax documents.

- Prepare Donor Information: Enter personal and identification details accurately, including marital status.

- Report Gifts and Transfers: List all gifts given that exceed the annual exclusion limit, including their value.

- Calculate Tax Liability: Use the form’s schedules to compute any gift or generation-skipping transfer taxes owed.

- Final Review and Submission: Double-check entries for completeness and accuracy before sending to the IRS.

Who Typically Uses Form 709

Identifying typical users of Form 709 helps clarify its relevance and application across various notable scenarios.

Common Filers

- High-Net-Worth Individuals: Often engage in large-scale gifting as part of estate planning.

- Parents and Grandparents: Regularly gift assets or money surpassing annual exclusions.

- Individuals Participating in Trusts: Involved in generation-skipping transfers which the IRS requires to be recorded.

Key Elements of Form 709

Recognizing critical sections of Form 709 enhances comprehension, promoting efficient navigation and completion.

Major Components

- Donor Information Section: Personal details and prior filings.

- Gift Descriptions and Values: Comprehensive documentation of each gift.

- GST Schedule: Necessary for those involved in transfers to younger generations.

- Tax Computation Section: Detailed calculations relevant to gift and transfer tax liabilities.

IRS Guidelines and Compliance

Following IRS guidelines ensures compliance, minimizing the risk of penalties associated with improper filing or late submissions.

Compliance Essentials

- Timely Filing: Form 709 is generally due on April 15 of the calendar year following the donation.

- Accuracy and Completeness: Ensure all relevant information is filled out correctly to avoid processing delays.

- Record Retention: Maintain copies of Form 709 and supporting documents for a minimum of three years.

Important Dates and Deadlines

Adhering to key filing deadlines is crucial for avoiding penalties and interest charges.

Critical Deadlines

- Annual Filing Deadline: Submit by April 15 unless an extension is granted.

- Extension Options: A six-month extension may be requested using Form 4868, aligning with personal income tax extensions.