Definition and Purpose of Form 709

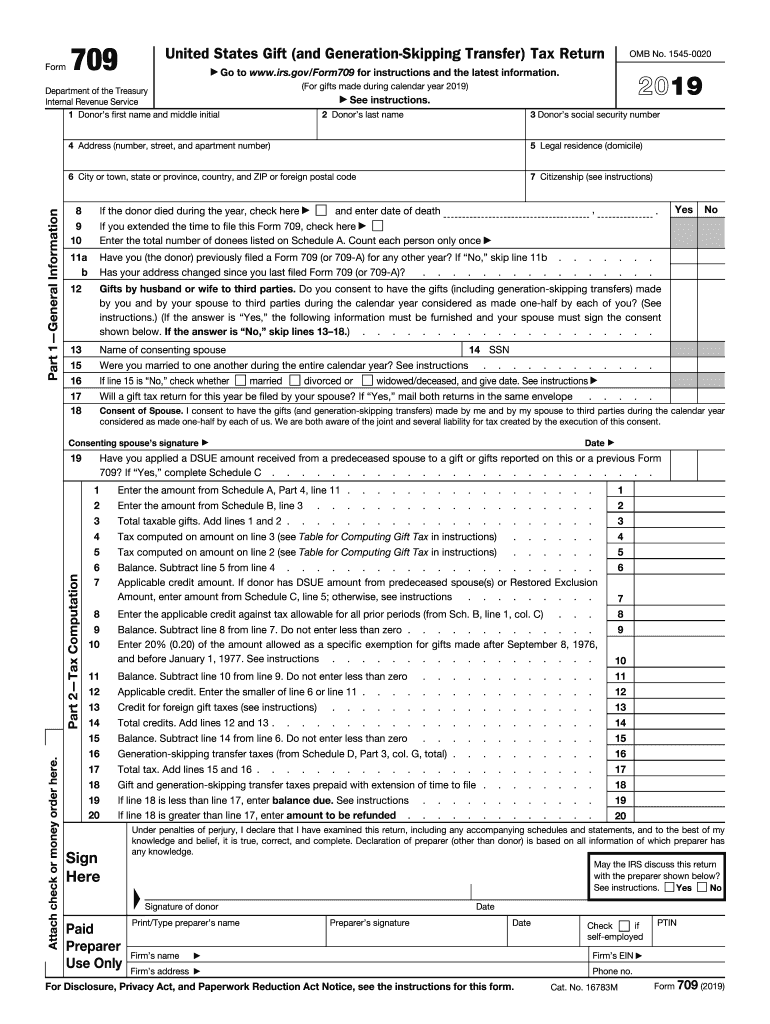

Form 709, officially known as the United States Gift (and Generation-Skipping Transfer) Tax Return, serves as a critical document for reporting gifts and transfers subject to the gift tax and/or the generation-skipping transfer tax. This form is used primarily by individuals who have made gifts that exceed the annual exclusion limit, thereby necessitating a detailed account of the transaction to the IRS. The form is essential for disclosing the nature, value, and recipient of gifts and helps ensure compliance with federal tax laws.

How to Obtain the 709 Form 2018

Acquiring Form 709 for 2018 can be done via multiple methods. The IRS website offers downloadable PDFs of the form, which can be printed and filled out manually. Alternatively, taxpayers can utilize specialized tax software or services that integrate the form directly into their digital filing process. Tax professionals often have access to the latest forms and can provide them upon request, ensuring that the most accurate and legally compliant version of the document is used.

Steps to Complete the 709 Form 2018

-

Gather Required Information: Begin by collecting the donor's personal details, as well as the recipient(s) of the gift. This includes names, addresses, and Social Security Numbers.

-

Detail the Gifts: On Part 1 of the form, list each gift given during the calendar year, specifying the description, date, and fair market value.

-

Tax Computation: Utilize Schedule A to compute the taxable amount of the gifts, taking into account any applicable exclusions or deductions.

-

Address Spousal Gift Splitting: If applicable, complete Part 1 for consenting to split gifts with a spouse. This ensures each partner is responsible for half the value of the gift basket.

-

Signature and Submission: Finally, the form must be signed by the individual filing as well as any involved spouse for split gifts, and then sent to the IRS, either electronically or via mail.

Eligibility Criteria for Using Form 709

The primary eligibility criterion revolves around the annual gift tax exclusion threshold, which has adjusted periodically. For the year 2018, if an individual made a gift exceeding $15,000 to a single person, they were required to file Form 709. Additionally, any gift involving generation-skipping transfer tax arrangements, regardless of the amount, necessitated completion of the form. Specific exemptions, deductions, and marital doubling rules must be assessed to determine exact filing requirements.

Key Elements of the 709 Form 2018

- Donor Information: Essential details of the individual making the gift.

- Gift Descriptions: Comprehensive descriptions for each gift, including their fair market value.

- Schedules for Tax Calculation: Sections such as Schedule A are used for calculating and reporting taxable amounts.

- Splitting Gifts: Options available for spouses to split gifts, thereby reducing the individual taxable amount per person.

- Signatures and Declarations: Required affirmations to confirm accuracy and compliance with tax regulations.

Penalties for Non-Compliance

Failure to file Form 709 when required can result in significant penalties. Financial penalties accrue based on a percentage of the tax initially owed, escalating with delay duration. Additionally, the statute of limitations for the IRS to audit the gift remains open until the form is correctly filed. In extreme cases, failure to report accurately can lead to allegations of tax evasion, subject to more severe legal repercussions.

Software Compatibility for Form 709

Form 709 for 2018 can be processed using popular tax preparation software like TurboTax and QuickBooks, which streamline the filing process. Such software typically guides users through data entry, ensuring all necessary fields are completed and validated for accuracy. These platforms often provide audit alerts and potential penalty assessments, offering a more secure avenue for submission.

Filing Deadlines for Form 709

The deadline for submitting Form 709 is April 15 of the year following the gift’s issuance. If the filer needs additional time, an extension can be requested by filing Form 4868. This extension aligns with personal income tax deadlines, granting additional time to gather necessary information and computations for comprehensive compliance.