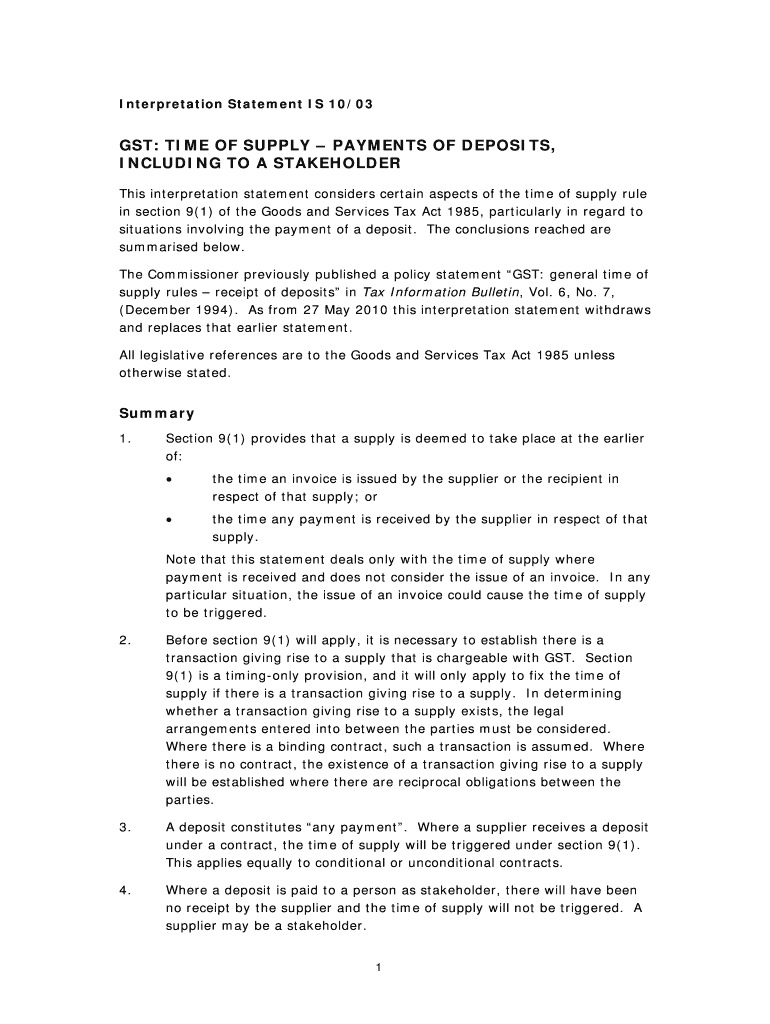

Definition & Meaning

The Interpretation Statement IS 10/03 serves a crucial role in clarifying the time of supply rules primarily outlined under section 9(1) of the Goods and Services Tax Act 1985. It explicitly addresses how deposits are treated under these rules, emphasizing that a deposit, once received by a supplier, triggers the time of supply regardless of contractual conditions. Its intentions are to ensure that all stakeholders understand when a transaction constitutes a taxable supply by standardizing interpretations across different scenarios.

Key Aspects of the Interpretation

- Deposits as Payment: Unambiguously states that deposits are considered payments at the point of receipt.

- Unconditional vs. Conditional Contracts: Delivers clarity on the implications, whether the contract is conditional or not.

- Replacement of Previous Statements: It updates and supersedes any earlier guidelines, thus solidifying new interpretations for consistency.

Key Elements of the Interpretation Statement IS 10/03

This section is geared towards understanding the foundational components that make up the Interpretation Statement IS 10/03.

Components

- Time of Supply: Establishes when a taxable supply is considered to have been made, focusing heavily on the deposit's receipt.

- Role of Stakeholders: Clarifies that if a deposit is held by a stakeholder and not the supplier, the time of supply is delayed.

- Guidance on Taxable Transactions: Offers directives on how VAT obligations are to be met based on these definitions.

Implications for Businesses

- Enhanced Compliance: Businesses have clear guidelines on VAT reporting, minimizing risks of non-compliance.

- Uniform Interpretations: Promotes consistency across various transactions and sectors.

How to Use the Interpretation Statement IS 10/03

Utilizing the Interpretation Statement IS 10/03 effectively requires a strong grasp of its changes and guidelines. Here's how businesses and individuals can implement this understanding.

- Identify Relevant Transactions: Determine if the time of supply rules apply to any deposits in your transactions.

- Assess Contractual Conditions: Review contracts to ascertain if the new rules align with the terms or if adjustments are needed.

- Consult Financial Advisors: Engage tax advisors to ensure proper application of the rules within existing accounting practices.

By following these steps, organizations can significantly enhance the accuracy of their VAT reporting.

Legal Use of the Interpretation Statement IS 10/03

The legal framework within which the Interpretation Statement operates ensures proper application and compliance with the VAT laws.

Applicable Laws and Regulations

- Goods and Services Tax Act 1985: The foundation of the Interpretation Statement's authority and application.

- ESIGN Act Compliance: Ensures that any electronic submissions related to VAT reporting are legally binding and acknowledged.

Compliance Strategies

- Regular Training: Businesses should educate their accounting teams on these legal shifts to maintain compliance.

- System Integrations: Leverage platforms like DocHub to enable seamless documentation compliance across transactions.

Who Typically Uses the Interpretation Statement IS 10/03

Understanding the diverse range of users of the Interpretation Statement IS 10/03 helps illuminate its practical applications.

Primary Users

- Accountants and Tax Advisors: Individuals responsible for preparing and advising on VAT reporting.

- Business Owners: Particularly those who manage their finances independently.

- Legal Teams: Legal professionals who need to ensure contractual terms comply with tax laws.

Impact on Users

- Enhanced Precision: Users can ensure interpretations and tax filings align with updated legislative standards.

- Risk Mitigation: By understanding usage, stakeholders can prevent costly errors and penalties.

Step-by-Step Completion Process

A structured approach is crucial for completing transactions under the new rules defined by the Interpretation Statement IS 10/03.

- Collect Necessary Documents: Include contracts, invoices, and evidence of deposit receipts.

- Review Financial Details: Ensure that the deposit's treatment aligns with the rules detailed in IS 10/03.

- Record Transaction in Accounting Software: Use platforms compatible with these requirements for accurate bookkeeping.

- Submit Relevant Returns: File VAT returns where applicable, meeting the deadlines set by the IRS.

These steps help businesses and individuals effectively incorporate the requirements into their financial practices.

State-Specific Rules for the Interpretation Statement IS 10/03

While IS 10/03 provides a broad framework, state-specific rules can affect certain applications and interpretations.

Understanding Regional Variances

- State Tax Regulations: Each state may have additional requirements influencing how the Interpretation Statement is applied.

- Regulatory Adjustments: Businesses should remain vigilant to state-specific modifications.

Adapting to Changes

- Continuous Monitoring: Regularly review state legislative updates to maintain compliance.

- Consult Local Experts: Liaise with local tax advisors for region-specific guidance and implementation strategies.

Examples of Using the Interpretation Statement IS 10/03

Real-world scenarios can illustrate the practical application of IS 10/03.

Scenario Illustrations

- Contractual Transactions: A deposit received for goods in a conditional sale triggers time of supply, even if the conditions aren’t met.

- Stakeholder Situations: If a stakeholder holds the deposit, the supply isn’t considered made until the supplier receives it.

These examples show how businesses should navigate deposit-related VAT considerations effectively.