Definition & Meaning

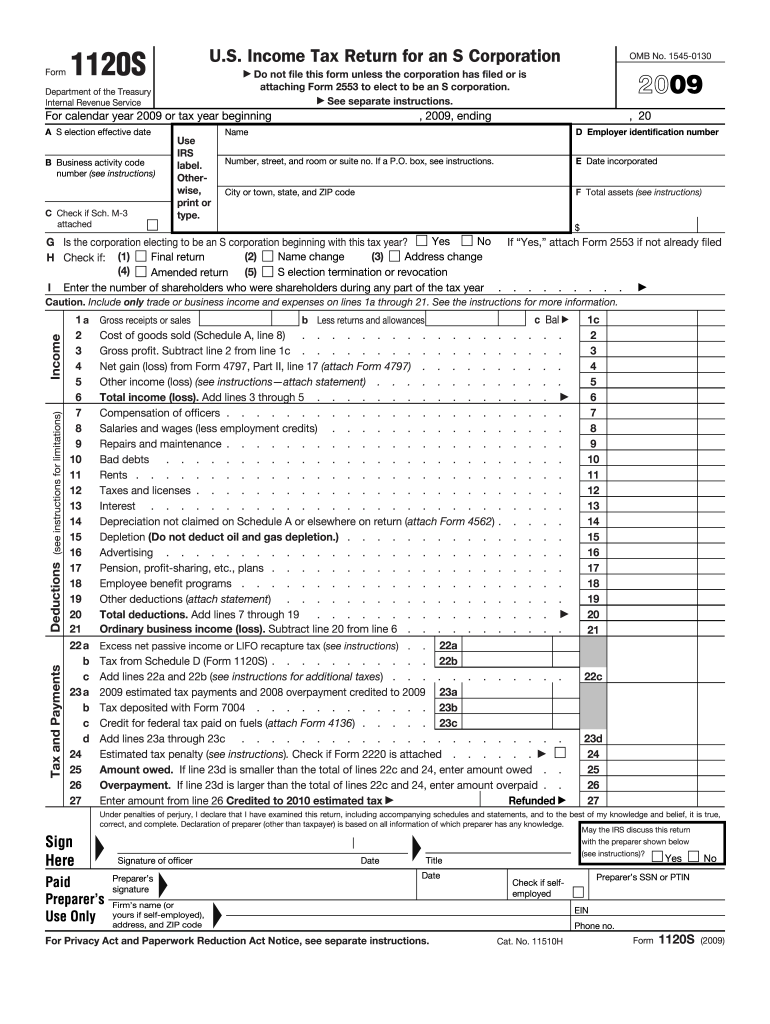

Form 1120-S is a U.S. tax form used by S Corporations to report income, deductions, and other pertinent financial information to the Internal Revenue Service (IRS). The 2009 version of this form pertains specifically to tax returns for the fiscal year ending in that calendar year. Unlike traditional corporations that are taxed at the corporate level, S Corporations pass income, losses, deductions, and credits through to their shareholders, who report these elements on their individual tax returns. This arrangement helps avoid double taxation on the corporate income, making the form crucial for ensuring accurate reporting and compliance with IRS regulations.

How to Use Form 1120-S 2009

-

Gather Necessary Documentation: Begin by assembling all financial documents, including income statements, balance sheets, and records of deductions and credits. This data is essential for accurate completion of the form.

-

Complete the Basic Information Section: Provide the corporation’s name, Employer Identification Number (EIN), and the tax year. Also, specify the date of incorporation and the type of business.

-

Report Income and Deductions: Fill out the sections dealing with various income sources and allowable deductions. Ensure accuracy to avoid discrepancies.

-

Attach Additional Forms: If the S Corporation has special deductions, credits, or activities, attach relevant forms or schedules, such as Schedule K-1, which outlines each shareholder’s share of income, deductions, and credits.

-

Review and Finalize: Double-check all entries for accuracy and compliance with IRS guidelines before filing electronically or via mail.

How to Obtain the Form 1120-S 2009

-

Download from IRS Website: The most straightforward method is downloading the form directly from the IRS website. Ensure you are downloading the 2009 version, which is essential for filing taxes for that specific year.

-

Tax Software: Many tax preparation programs offer access to the necessary IRS forms, including previous years, which may assist in completing and filing the form electronically.

-

Professional Assistance: If unsure about obtaining or filling out the form, consult with a tax professional who can provide guidance and access to the correct versions.

Steps to Complete the Form 1120-S 2009

-

Identifying Information: Enter the corporation’s name, address, EIN, and the date of incorporation on the form. Check if the S corporation election is valid for 2009.

-

Income Reporting: Detail gross receipts or sales, along with deductions for returns and allowances, to calculate total income.

-

Deductions: Complete Section II for ordinary business income deductions, including salaries, wages, and other expenses.

-

Compensation of Officers: Report compensation paid to officers, including the amount allocated based on their time dedication and role importance.

-

Tax Credits and Payments: Report estimated tax payments and any overpayment applied from the prior year’s return.

-

Schedule K & Shareholders’ Information: Complete this section with information to be distributed to shareholders for their individual tax returns.

Important Terms Related to Form 1120-S 2009

-

S Corporation: A special type of corporation created through an IRS tax election, allowing income to pass through to shareholders.

-

Schedule K-1: A form used to report each shareholder's pro-rata share of the corporation’s income, deductions, and credits.

-

EIN (Employer Identification Number): A unique number assigned to businesses for tax reporting purposes.

-

Ordinary Business Income: Income derived from typical business operations, excluding unusual or infrequent transactions.

Key Elements of Form 1120-S 2009

-

Part I: Income: This section details gross receipts, returns and allowances, and cost of goods sold to determine total income.

-

Part II: Deductions: Lists deductions like compensations and officer salaries, necessary for calculating net income.

-

Part III: Shareholder Information: Requires information about shareholders necessary for distributing Schedule K-1s.

-

Accountant’s Report Section: If an accountant's report is included, it must be attached to the return.

IRS Guidelines

Adhering to IRS guidelines is critical when completing Form 1120-S. Key points include:

-

Timely Filing: Ensure the form is filed by the 15th day of the third month after the end of the corporation’s tax year (usually March 15 for calendar-year taxpayers).

-

Completeness and Accuracy: Verify all information and computations to avoid IRS queries or rejections.

-

Signature Requirement: The form must be signed by an officer of the corporation to be considered valid.

-

Record Retention: Maintain copies of filed forms and related documentation for a minimum of three years for auditing purposes.

Filing Deadlines / Important Dates

-

Standard Deadline: The standard deadline for filing Form 1120-S is March 15, assuming a calendar-year fiscal period. Extensions may be available, pushing this deadline to September 15.

-

Estimated Payments: Businesses are required to make quarterly estimated tax payments if needed, according to their anticipated tax liability.

Required Documents

To accurately complete Form 1120-S, gather the following:

-

Income Statements: Comprehensive records of the corporation’s revenue.

-

Expense Documentation: Itemized lists of business expenses and supporting receipts.

-

Shareholder Information: Accurate details needed for Schedule K-1 preparation.

-

Supporting Schedules or Forms: Additional IRS schedules or forms related to special activities or deductions.

Penalties for Non-Compliance

Failing to properly file Form 1120-S or meet submission deadlines can result in significant penalties:

-

Late Filing: A penalty is imposed for not filing on time, calculated based on the period of delay and the number of shareholders.

-

Incomplete or Inaccurate Reporting: Can trigger additional penalties or an IRS audit, which may lead to more severe financial consequences.

Ensuring adherence to IRS regulations and deadlines will mitigate risk and ensure compliance.