Definition & Meaning

The 2013 Form 1120-S is an official United States federal tax document used by S corporations to report income, deductions, gains, losses, etc. S corporations pass these financial elements onto their shareholders, who then report these on their individual tax returns. Each shareholder receives a Schedule K-1, which outlines their share of the corporation's financial activities.

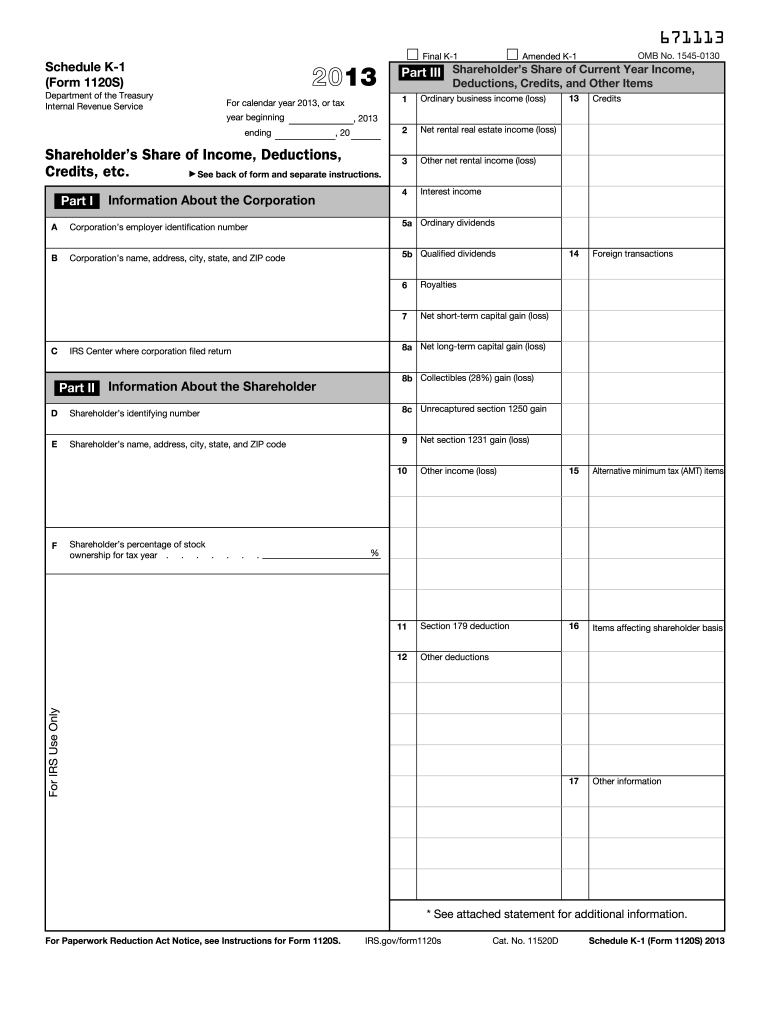

Key Elements of the 2013 Form 1120-S

Form 1120-S includes several key sections:

- Income section: This part reports the total revenue generated by the S corporation from various sources.

- Deductions section: Here, the company lists all eligible expenses, such as salaries, rent, and utilities, which reduce taxable income.

- Tax and Payments section: This section is used to calculate any taxes owed based on the corporate income.

- Schedule K-1: Each shareholder receives this to report their share of the S corporation’s finances in their personal tax filings.

Steps to Complete the 2013 Form 1120-S

- Gather Required Documents: Collect all necessary documents, including financial statements and prior year tax returns.

- Fill Out General Information: Provide detailed information about the business, such as name, address, and employer identification number (EIN).

- Report Income and Deductions: Enter detailed financial figures in the income and deductions sections.

- Complete Schedule K-1: Assign income, credits, and deductions to shareholders proportional to their ownership interests.

- Review and Verify All Entries: Ensure no errors or omissions exist in the form.

- Submit by Deadline: File the completed form by the due date, usually March 15, to avoid penalties.

Who Typically Uses the 2013 Form 1120-S

This form is primarily used by S corporations and their shareholders. Typically, small to medium-sized business entities that elect to be treated as S corporations for tax purposes use this form. This structure allows these entities to avoid double taxation, as income is passed through to the shareholders.

Legal Use of the 2013 Form 1120-S

Filing Form 1120-S correctly is essential for ensuring compliance with U.S. tax laws. It provides the necessary documentation for declaring business income and expenses, helping to mitigate the risk of audits and penalties. This form is legally binding and provides a transparent record of the company's financial activities.

IRS Guidelines

The Internal Revenue Service (IRS) provides detailed instructions for completing Form 1120-S:

- E-filing Encouraged: The IRS provides electronic filing options for convenience and quicker processing.

- Correction Protocols: If errors are discovered post-filing, an amended return can be submitted using Form 1120-X.

- Recordkeeping Requirements: Businesses must maintain records supporting all figures and claims for a minimum of seven years.

Filing Deadlines / Important Dates

Typically, Form 1120-S must be filed by March 15 for calendar-year corporations. If additional time is needed, businesses can request an automatic six-month extension using Form 7004, but any taxes owed must still be paid by the original deadline to avoid interest and penalties.

Penalties for Non-Compliance

Failure to timely file Form 1120-S or provide accurate Schedule K-1s to shareholders can lead to significant penalties. The IRS may impose fines for late filings or incorrect documentation. It's crucial to adhere to deadlines and maintain accuracy to avoid financial and legal consequences.