Definition and Meaning

The 2016 Schedule K-1 (Form 1120-S) is a federal tax document used by S corporations to report a shareholder's share of income, deductions, credits, and other financial items. For the 2016 tax year, this form plays a crucial role in ensuring shareholders report this information accurately on their individual income tax returns. It includes various sections covering different types of income, such as ordinary business income, rental income, dividends, and capital gains. Understanding the function of each component of the Schedule K-1 helps shareholders fulfill their tax obligations accurately.

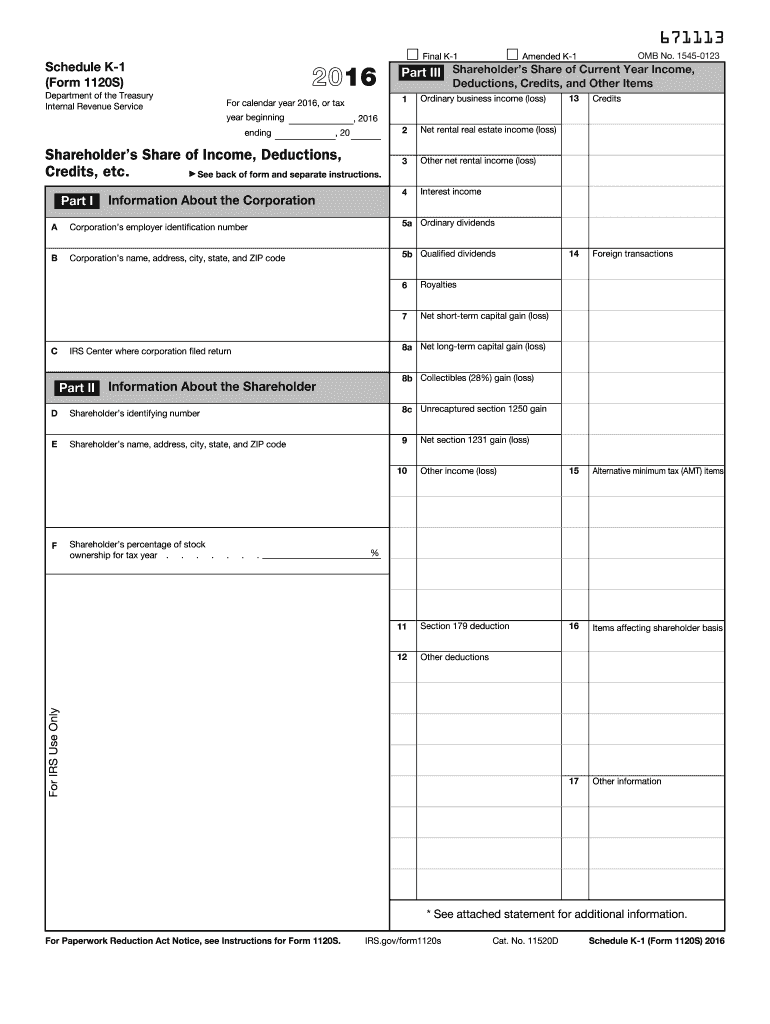

Key Elements of the 2-S K-1 Form

The form consists of multiple parts designed to capture specific financial details:

- Part I: Information about the Corporation - Includes details like the corporation's name, EIN, and address.

- Part II: Information about the Shareholder - Details the shareholder's name, TIN, and ownership percentage.

- Part III: Shareholder’s Share of Current Year Income, Deductions, Credits, and Other Items - Reports all types of incomes and deductions applicable to the shareholder.

Each section provides detailed guidelines and instructions, ensuring accurate reporting and compliance with federal tax laws.

Steps to Complete the 2-S K-1 Form

Completing the form involves several key steps:

- Gather Necessary Information: Collect all relevant financial data and documentation from both the corporation and shareholders.

- Complete Part I and II: Fill out the corporation and shareholder information sections accurately.

- Report Income and Deductions: Input all data related to income, deductions, and credits in Part III. This includes ordinary income, rental income, and deductions.

- Review and Verify: Ensure all information is correct and consistent across all sections.

- File the Form: Submit the completed form to the IRS along with the shareholder’s individual tax return.

Attention to detail is crucial in this process to prevent potential errors or discrepancies.

Important Terms Related to the 2-S K-1 Form

Understanding the terminology used on the form is essential:

- Ordinary Business Income: Income from the normal operations of the business.

- Nonpassive Income: Earnings from business activities where the shareholder materially participates.

- Deductions and Credits: Allowed reductions in income for specific expenses and eligible tax credits.

Familiarity with these terms ensures a clear understanding of the form’s requirements and an accurate representation of the shareholder's tax responsibilities.

Who Typically Uses the 2-S K-1 Form

The form is primarily used by S corporation shareholders in the United States. S corporations are pass-through entities, meaning they do not pay corporate tax directly. Instead, income, losses, and other tax attributes are passed onto the shareholders, who then report these on their individual tax returns. This form is important for anyone holding shares in an S corporation during the tax year 2016, enabling them to fulfill their tax reporting obligations.

Who Issues the Form

S corporations themselves are responsible for issuing the Schedule K-1 to their shareholders. The corporation compiles necessary financial data and completes the form, distributing it to each shareholder. The form must be furnished by the corporation to the shareholders in a timely manner to ensure that they meet their individual tax filing deadlines.

Filing Deadlines and Important Dates

For the 2016 tax year, the Schedule K-1 should be furnished to shareholders by March 15, 2017, or the 15th day of the third month after the end of the corporation’s tax year. This aligns with the corporate tax filing deadline, ensuring shareholders have sufficient time to incorporate necessary details into their individual tax submissions by April 15th.

Required Documents

To fill out the Schedule K-1 accurately, certain documents are required:

- Corporate Financial Statements: Including income statements and balance sheets.

- Shareholder Agreements: Detailing the ownership percentage and any other relevant terms.

- Previous Year’s K-1 Forms: For historical reference and comparability.

Having these documents readily available aids in the accurate and efficient completion of the form.

IRS Guidelines

The Internal Revenue Service provides specific guidelines and instructions for filling out the Schedule K-1. Following these guidelines is essential for ensuring compliance and reducing the risk of errors. These instructions detail how to report different types of income, how to handle international considerations, and the calculation of deductions and credits accurately. Adhering to IRS rules and instructions is critical for both the corporation’s and the shareholder’s tax operations.

Penalties for Non-compliance

Failure to accurately complete and submit the Schedule K-1 can result in significant penalties. Shareholders may face additional taxes, interest, and penalties for underreporting income or failing to file the form timely. Likewise, corporations that do not issue the Schedule K-1 in a timely and accurate manner could be subjected to fines and penalties, emphasizing the importance of accuracy and punctuality in this process.