Definition and Purpose of Schedule K-1 (Form 1120S)

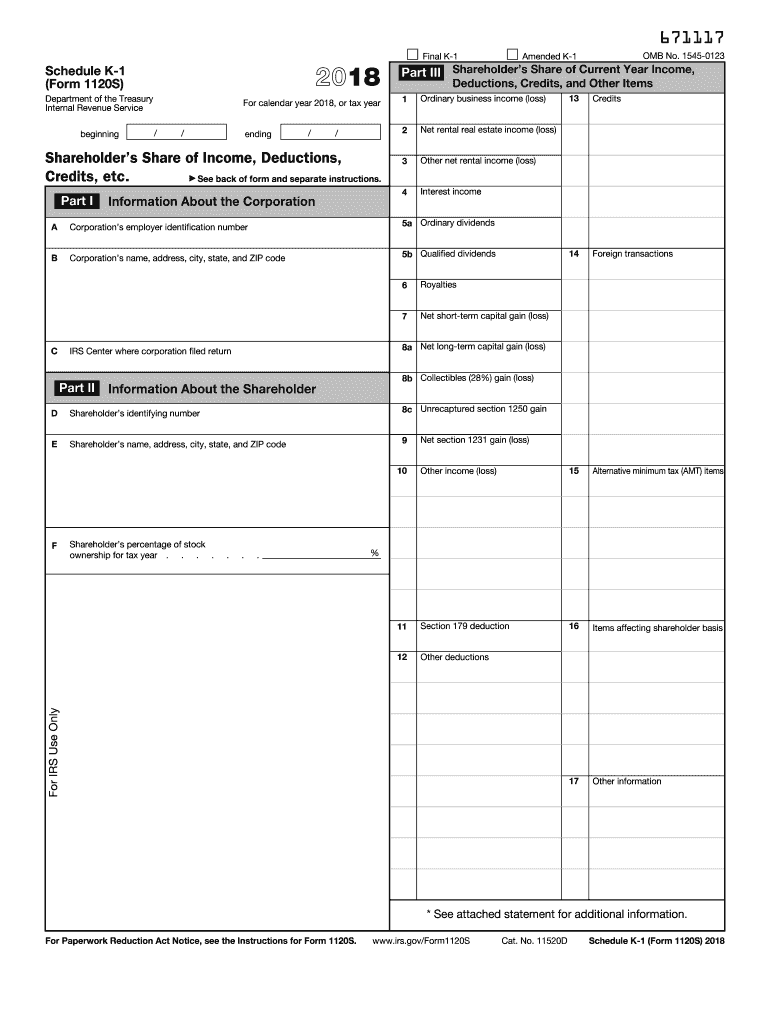

Schedule K-1 (Form 1120S) for the tax year 2018 is a document used by S corporations to report each shareholder's share of income, deductions, credits, and other tax-related items. This form is essential as it provides shareholders with necessary figures needed to report their income on individual tax returns. The document details various income types, such as ordinary business income, rental income, and capital gains, giving shareholders a comprehensive view of their tax obligations.

Key Elements in Schedule K-1 (Form 1120S)

- Ordinary Business Income: Refers to the income generated from the corporation's core operations.

- Dividends: Income distributed from the corporation’s profits.

- Capital Gains and Losses: Represents profit or loss from selling an asset.

- Deductions and Credits: Items that reduce taxable income or provide tax savings.

Understanding these components helps shareholders accurately report their income and comply with tax regulations.

Using the Schedule K-1 (Form 1120S)

Step-by-Step Usage Process

- Receive the Form: Shareholders receive Schedule K-1 from the S corporation they have invested in.

- Review Income Details: Verify all reported income figures, including business income, dividends, and capital gains, against personal records.

- Accumulate Deductions and Credits: Confirm any deductions and credits listed and how they apply to individual tax situations.

- Apply to Tax Returns: Use the figures provided in the Schedule K-1 to accurately report on personal tax returns (using IRS Form 1040).

Practical Example

For a shareholder with a diverse portfolio, the Schedule K-1 provides the granularity needed to ensure each income stream is taxed appropriately. If an investor owns shares in multiple S-corporations, cross-referencing each K-1 provides a consolidated view for accurate tax filing.

Obtaining the Schedule K-1 (Form 1120S)

Sources and Methods

- Directly from the S Corporation: Typically sent by mail or electronically from the corporation.

- Professional Tax Advisors: Often facilitate access if handling an individual's tax filings or offering financial services.

Importance of Accurate Timelines

Shareholders must receive their Schedule K-1 well in advance of tax filing deadlines to accommodate for comprehensive income analysis and accurate filing.

Who Uses the Schedule K-1 (Form 1120S)

Typical Users

- S Corporation Shareholders: Individuals with ownership in an S-corporation.

- Tax Professionals: Accountants and tax advisors who manage clients' tax documents and filings.

The document ensures transparency and allows stakeholders to meet their tax obligations accurately.

Completing Schedule K-1 (Form 1120S)

Detailed Completion Steps

- Verify Entity Information: Ensure all identifying information for the S corporation is accurate.

- Enter Shareholder’s Share of Income: Each section must be accurately filled according to the respective shareholder’s ownership interest.

- Detail Deductions and Credits: Provide a detailed breakdown to ensure all available tax advantages are recorded and reported.

- Cross-check Totals: Triple-check all numerical entries for accuracy to avoid discrepancies during tax filing.

Common Mistakes to Avoid

- Incorrect Income Allocation: Misreporting or misunderstanding income types can lead to tax complications.

- Overlooking Deductions: Failing to leverage all deductions can result in higher taxes.

Important Terms Related to Schedule K-1 (Form 1120S)

Key Definitions

- Basis: Refers to the shareholder's investment in the corporation, essential for calculating gain or loss upon disposition.

- Pass-through Income: Income passed on to shareholders without it being taxed at the corporate level.

Understanding these terms ensures clarity and compliance with tax reporting requirements.

Legal Use and Compliance for Schedule K-1 (Form 1120S)

Complying with IRS Regulations

- Accurate Record-keeping: Maintain precise records of all income and deductions.

- Timely Filing: Adhere strictly to IRS deadlines to avoid penalties.

IRS Guidelines and Instructions

The IRS provides comprehensive guidelines outlining how Schedule K-1 figures should be applied to individual tax returns, ensuring shareholders meet all federal requirements.

State-Specific Rules and Variations

State Differences

- Income Tax Variances: Different states may tax certain income types at varying rates.

- Additional State Filing Requirements: Some states require additional forms or information not captured at the federal level.

Understanding these state-specific rules helps shareholders optimize their tax filing for both federal and state compliance.

Penalties for Non-Compliance with Schedule K-1 (Form 1120S)

Avoiding Penalties and Fines

- Failure to Report: Omissions or errors in reporting can lead to fines.

- Late Filing Penalties: Deadlines are critical; missing them can incur additional charges.

Effective use and knowledge of Schedule K-1 helps prevent these costly penalties.