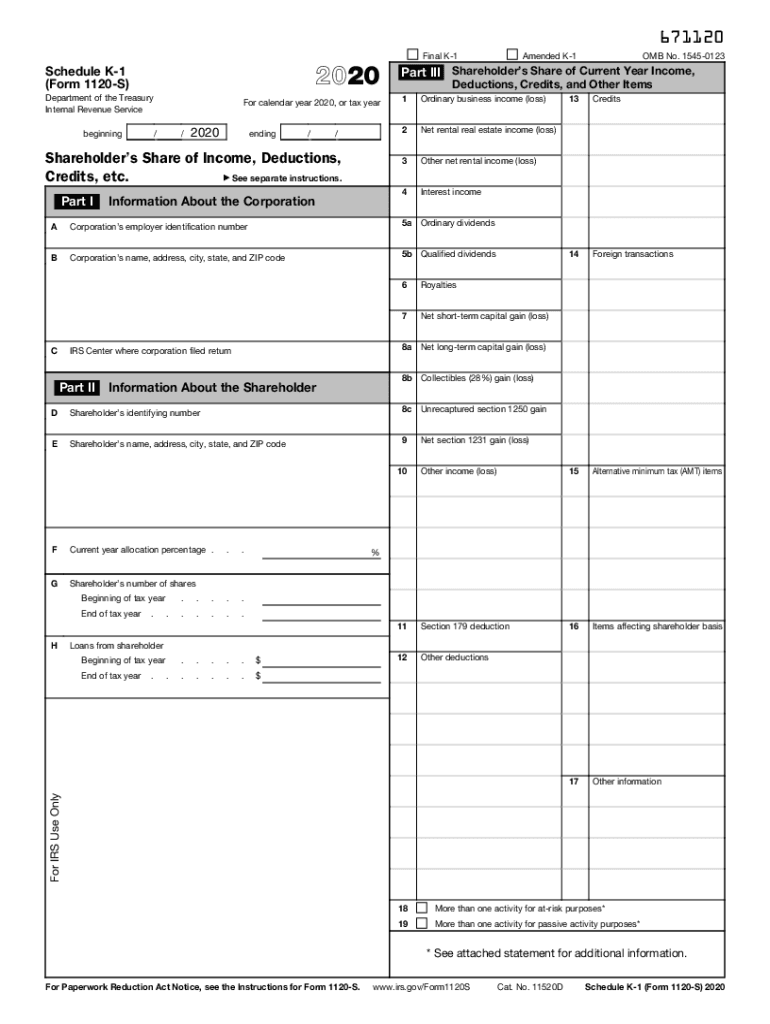

Definition and Purpose of the K-1 Form

The K-1 form, officially known as the Schedule K-1, is a tax document used to report income, deductions, credits, and other fiscal items for partners, shareholders, or beneficiaries in a variety of business structures such as partnerships, S corporations, and trusts. Each entity that passes income through to individuals must provide them with a K-1 form detailing their share of the financial activities. The information collected helps individuals accurately report their income on their personal tax returns.

How to Use the K-1 Form

Using a K-1 form involves several steps to ensure correct reporting of income and deductions. Recipients of a K-1 must carefully transfer the data from the form onto their personal tax return. For example:

- Identifying Information: Verify the taxpayer information to ensure the details on the form match personal records.

- Income Reporting: Transfer designated income items, such as ordinary business income or dividends, onto the appropriate sections of your tax return (e.g., IRS Form 1040).

- Deductions and Credits: Accurately deduct expenses or claim credits, such as investment credits, which are reported on the K-1.

It is essential to consult IRS instructions or a tax professional for guidance when using a K-1 form, as misreporting can lead to tax complications.

Steps to Complete the K-1 Form

The process of completing a K-1 form primarily rests with the entity issuing the document, but recipients should know how the form is compiled to understand their tax obligations:

- Collect Financial Data: Businesses calculate each partner’s or shareholder’s share of income, losses, and other tax items.

- Assign Individual Shares: Proportionally distribute components of the entity's earnings to each participant according to their ownership percentage or agreement.

- Complete the K-1 Form: Contributions are documented on the correct lines, and descriptive information, like the participant’s share of liabilities, is included.

- Distribute Forms: Issued forms are sent to the involved individuals, who use this data for their tax filings.

Key Elements of the K-1 Form

A K-1 form includes several crucial sections that must be correctly filled out:

- Partner's Information: Name, address, and tax identification number.

- Income Details: Breakdown of ordinary business income, rental income, dividends, and capital gains.

- Deductions: This could involve deductions related to passive activities or tax credits.

- Foreign Transactions: Information if involved in foreign operations.

Understanding each section is key to ensuring compliance and proper financial reporting.

Who Typically Uses the K-1 Form

A variety of individuals and entities utilize the K-1 form:

- Members of Partnerships: Must report their share of partnership income, deductions, and credits.

- S Corporation Shareholders: Use the Schedule K-1 (Form 1120-S) to determine their share of income and expenditures.

- Beneficiaries of Trusts or Estates: Schedule K-1 (Form 1041) informs beneficiaries of the income, deductions, and credits distributed by the trust or estate.

Each group uses the K-1 to fulfill disclosure obligations on their personal tax filings.

IRS Guidelines and Compliance

Adhering to IRS guidelines when handling K-1 forms is crucial:

- Reporting Deadline: Entities must provide K-1 forms to recipients by March 15 following the end of the fiscal year.

- Accurate Reporting: Ensures individuals assess their tax liabilities correctly and prevents disputes with the IRS.

- Amendments: In case of errors, entities must issue a corrected K-1 to maintain IRS compliance.

It’s essential to stay updated with any tax code changes impacting the K-1 form to ensure proper filing.

Penalties for Non-Compliance

Failure to comply with IRS requirements surrounding the K-1 form can result in:

- Fines: Penalties for neglecting to provide an accurate or timely K-1 form.

- Increased Audits: Non-compliance could increase the risk of IRS audits for both the entity and the individual.

Understanding these risks emphasizes the necessity of accurate form preparation and filing.

Taxpayer Scenarios and Use Cases

The K-1 form applies to various taxpayer scenarios, influencing how tax obligations are met:

- Self-Employed Individuals: Those involved in partnerships report their share of profits and losses.

- Retirees with Investments: Retirees with stakes in S corporations rely on K-1 for dividend income reporting.

- Trust Beneficiaries: Individuals receiving income from a trust report it based solely on the K-1 form data.

Investigating these scenarios elucidates how diverse taxpayer situations necessitate accurate use of the K-1 form.