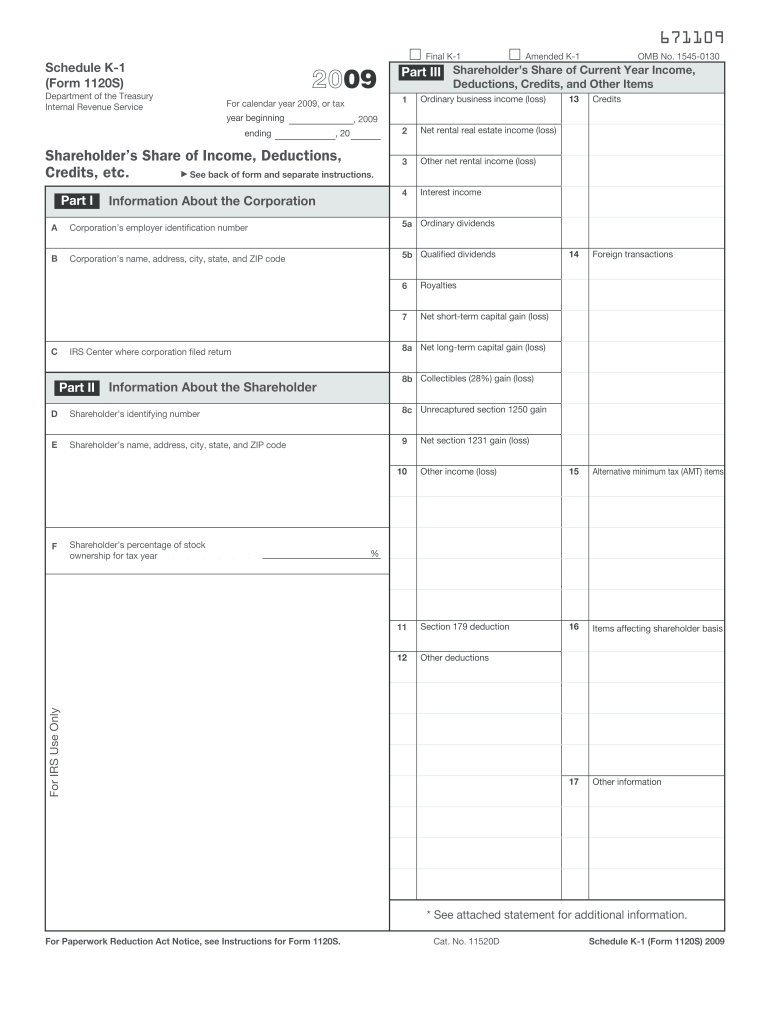

Definition & Meaning

The 2-S Form is a tax document issued by the IRS used by S corporations to report their financial activities for the tax year 2009. This form is vital as it outlines the corporation’s income, deductions, and credits, accessed by the shareholders for inclusion in their individual tax returns. It includes sections to detail items such as ordinary business income, rental income, dividends, and capital gains.

How to Use the 2-S Form

To use the 2-S Form, an S corporation must gather all its financial transactions from the tax year. Corporations utilize this form to disclose their financial details, which are then passed on to shareholders via Schedule K-1, detailing each shareholder’s share of income and other tax items.

- Gather Financial Data: Ensure all income and expenses are accurately documented.

- Complete Each Section: Fill in ordinary business income, deductions, and other required information.

- Attach Schedule K-1: Provide copies to all shareholders for their individual tax filings.

Steps to Complete the 2-S Form

Completing the 2-S Form requires careful attention to detail. Follow these steps:

- Start with Basic Information: Include the corporation’s name, address, and EIN.

- Report Income: Fill in details of gross income derived from various activities.

- Deductions and Credits: Accurately enter all possible deductions to minimize tax liabilities effectively.

- Calculate Net Income: Determine net income by subtracting deductions from total income.

- Final Review: Verify all information, ensuring complete accuracy.

- File Correctly: Submit the form to the IRS by the required deadline to avoid penalties.

Important Terms Related to the 2-S Form

Several terms are essential to understand when dealing with the 2-S Form:

- S Corporation: A corporation that elects to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes.

- Schedule K-1: A crucial part of the form sent to shareholders, detailing their share of the corporation’s income.

- Deductions: Expenses that can be subtracted from gross income to determine taxable income.

- EIN (Employer Identification Number): A unique number assigned to businesses for tax identification purposes.

IRS Guidelines

The IRS provides guidelines to ensure proper compliance with tax regulations regarding the 2-S Form:

- Timely Filing: The IRS mandates that the 1120-S Form must be filed by March 15th annually unless an extension is granted.

- Accurate Reporting: All income, deductions, credits, and shareholder information must be reported truthfully.

- Compliance Requirements: Follow due diligence in calculations and form submissions as stipulated by IRS guidelines to prevent errors.

Filing Deadlines / Important Dates

Adhering to critical dates is essential to avoid penalties:

- Filing Deadline: March 15, following the end of the tax year.

- Extension Deadline: If an extension is granted, the filing deadline may extend to September 15.

- Amendments: Submit any corrections to the IRS as soon as possible to mitigate potential legal repercussions.

Penalties for Non-Compliance

Failing to comply with IRS regulations can result in penalties:

- Late Filing Penalty: If the form is not filed timely, the IRS imposes a penalty calculated per month for each shareholder.

- Incorrect Information Penalty: Providing false or incorrect information can result in additional fines or legal consequences.

- Negligence Penalty: Careless errors that show disregard for tax rules may incur further penalties.

Business Entity Types (LLC, Corp, Partnership)

Different business entities may have specific implications when using form 1120-S:

- S Corporations: The primary users of Form 1120-S, these entities must meet specific IRS qualifications to maintain their tax status.

- LLCs: Limited Liability Companies that elect to be taxed as S corporations can also use this form.

- Partnerships & Corporations: Generally use forms specific to their entity type, rather than 1120-S.