Definition & Meaning

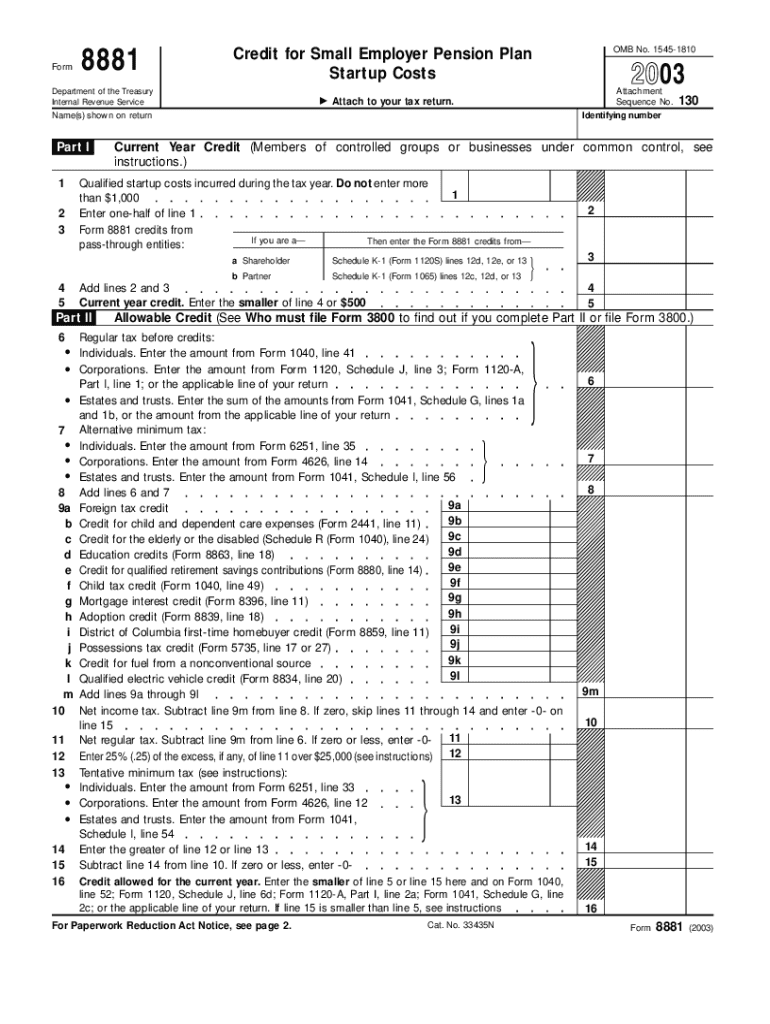

Form 8881, titled "Credit for Small Employer Pension Plan Startup Costs," is utilized by eligible small employers to claim a tax credit for qualified startup expenses associated with establishing or administering an eligible employer pension plan. This form provides financial incentives for small businesses to offer retirement plans by allowing them to reclaim a portion of the startup expenses. Specifically, this credit is a part of the general business credit, enabling employers to claim 50% of the startup costs, up to $500 annually, for the first three years. Understanding the precise definition and purpose of this form is crucial for employers who wish to take advantage of the tax benefits it offers.

How to Use the Form 8881

Small employers use Form 8881 to apply for a tax credit associated with the creation or management of a pension plan. To effectively use this form, follow these steps:

- Determine Eligibility: Ensure that your business qualifies as a small employer under IRS definitions.

- Calculate Qualified Costs: Identify and calculate the startup costs incurred from establishing or maintaining the plan.

- Complete the Form: Accurately fill out the form by entering relevant data pertaining to costs and business details.

- File with Tax Return: Submit the completed form alongside your business's tax return to claim the credit.

By following these steps, employers can ensure they maximize the benefits of Form 8881, supporting their effort to provide retirement plans to their employees.

Steps to Complete the Form 8881

Completing Form 8881 requires attention to detail and accurate data input. Here is a step-by-step guide:

- Identify Employer Information: Enter all necessary employer information, including the name, address, and employer identification number (EIN).

- Enter Plan Information: Provide details about the pension plan, including type and establishment date.

- Calculate Credit: Determine the eligible credit amount by calculating 50% of the incurred startup costs, ensuring it does not exceed $500 per year.

- Fill in Tax Calculation: Enter the calculated credit amount into the correct section of the form.

- Review for Accuracy: Double-check all information to ensure accuracy and completeness.

Each step ensures that you correctly apply for the available credit without errors that could delay processing or result in non-compliance.

Eligibility Criteria

To qualify for the credit offered by Form 8881, certain eligibility criteria must be met:

- Small Employer Status: The employer must have had no more than 100 employees who received at least $5,000 in compensation in the preceding year.

- Qualified Startup Costs: Only expenses for establishing or administering a qualified employer plan are eligible.

- New Plan Requirement: The credit is specifically for new plans that have not been established before by the employer.

- Three-Year Window: The credit is available for expenses incurred within the first three years of establishing the plan.

Meeting these criteria is essential to ensure a successful claim of the tax credit, allowing employers to reduce financial burdens associated with starting a pension plan.

Key Elements of the Form 8881

Form 8881 consists of several important elements that require careful attention:

- Section for Employer Details: Captures basic information about the employer.

- Plan Information Section: Contains specifics about the pension plan, including the type and date of establishment.

- Credit Calculation: Specifically focused on computing the allowed credit based on startup costs incurred.

- Tax Information Integration: Includes where to integrate the credit information into the larger business tax return components.

Each section of the form has a particular focus and contributes to accurately determining the eligible credit sum for qualifying employers.

IRS Guidelines

The Internal Revenue Service (IRS) provides specific guidelines for completing and submitting Form 8881:

- Documentation Requirements: Maintain thorough records of all startup costs and documentation of plan establishment.

- Filing Protocols: The form should be filed alongside the entity's tax return, ensuring all figures are reflected accurately in the tax filing.

- Amendments and Corrections: If errors are discovered after submission, the IRS guidelines provide specific protocols for amendments.

Compliance with these guidelines is crucial for ensuring the credit application is processed without issues and within the regulatory framework.

Who Typically Uses the Form 8881

The primary users of Form 8881 are small business employers seeking to offer retirement benefits to their employees. Companies that fall into the following categories often use this form:

- Startups: New businesses launching pension plans for the first time.

- Small Enterprises: Organizations with limited employee numbers looking to enhance employee benefits.

- Businesses Introducing New Plans: Employers previously without retirement plan offerings wishing to establish new systems.

Each of these business types uses the form to alleviate the financial impact of setting up retirement plans, demonstrating the form's broad applicability within the small business sector.

Penalties for Non-Compliance

There are potential penalties for not adhering to Form 8881's compliance requirements:

- Loss of Credit: Incorrect or fraudulent filing may result in the disqualification of the credit claim.

- IRS Penalties: Financial penalties may be imposed for inaccuracies or late submissions.

- Audit Risks: Non-compliance could trigger audits or further scrutiny by the IRS.

Understanding and avoiding these penalties is vital, and ensuring accurate and timely submission of the form helps in safeguarding against such consequences.

Required Documents

When preparing to submit Form 8881, certain documents are typically required to substantiate claims:

- Proof of Startup Costs: Receipts or invoices concerning the setup or administration of the pension plan.

- Pension Plan Documentation: Official documents detailing the plan’s terms and conditions.

- Employer Eligibility Proof: Documentation showing compliance with small employer criteria.

These documents ensure that claims are anchored in verifiable evidence, thus facilitating a smooth submission process and claiming of credits.