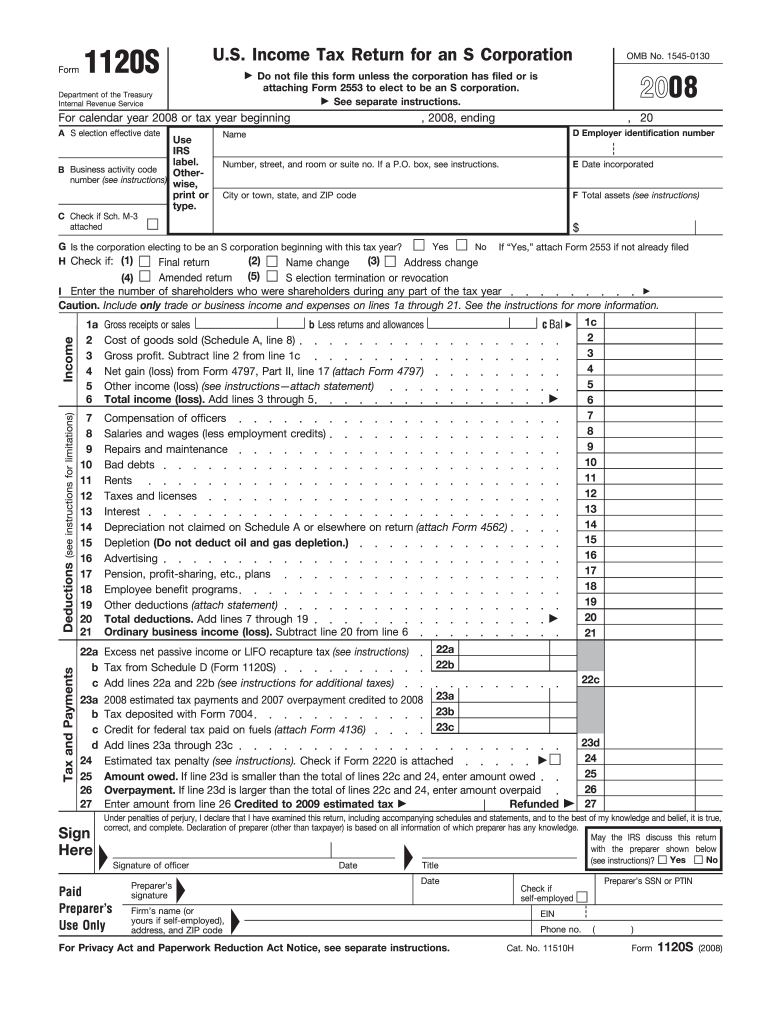

Definition and Purpose of the 2008 Form 1120S

The 2008 Form 1120S is specifically designed for S corporations in the United States to report their income, deductions, and financial activities to the Internal Revenue Service (IRS). It is essential for S corporations that have elected to be taxed as pass-through entities, allowing income to flow directly to shareholders without facing corporate taxes. This form simplifies tax responsibilities while ensuring compliance with federal tax regulations.

Key Features

- Financial Reporting: The form collects detailed financial statements, including income, deductions, and credits, to adequately assess a corporation’s tax liabilities.

- Schedule K-1: Distributed to shareholders, this schedule reports each shareholder's share of income, deductions, and credits, impacting their individual tax returns.

- Election of S Corporation Status: Only corporations that have filed Form 2553 can use Form 1120S, crucial for tax strategy.

Steps to Complete the 2008 Form 1120S

Filing the 1120S involves detailed steps to ensure accuracy. Below is a general guide for completing the form:

- Gather Necessary Information, including prior year tax returns, financial statements, and details of any loans or shareholders' equity investment.

- Complete Corporate Information: Fill out the corporation’s name, address, and Employer Identification Number (EIN) on the form.

- Report Income and Deductions: Accurately disclose all sources of income and applicable business expenses.

- Schedule K and K-1: Utilize these sections to detail each shareholder’s share of income, deductions, and credits.

- Review and Submit: Thoroughly review the form for accuracy prior to submission to prevent delays or amendments.

Example Scenarios

- Newly Converted S Corporation: New S corporations should compare previous C corporation filing requirements with 1120S requirements to align tax obligations.

- Multi-State Operations: Companies operating in multiple states need to ensure adherence to state tax obligations.

Important Terms Associated with the 2008 Form 1120S

Understanding the key terminology is vital for accurate completion and compliance:

- Accrual Method: A method of accounting whereby income and expenses are recorded when they are earned or incurred.

- Pass-Through Entity: An entity whose income is passed on to shareholders without being subject to corporate tax.

- Shareholder Basis: Represents each shareholder’s investment in the company, impacting their distribution limitations.

- Distribution: Disbursements made to shareholders that are not taxed as long as they do not exceed the shareholder’s stock basis.

Legal Compliance and Use of the 2008 Form 1120S

The legal use of Form 1120S is defined under IRS S corporation regulations. Corporations must have valid S corporation status, abide by operational limitations, such as a maximum of 100 shareholders, and adhere to the requirement that all shareholders be U.S. residents.

Legal Guidelines

- ESIGN Act Compliance: Electronic signatures submitted with the form should adhere to the ESIGN Act to ensure legal binding and acceptance by the IRS.

- Recordkeeping: Maintain supporting documentation for at least seven years to document tax positions taken on filed returns.

IRS Guidelines for the 2008 Form 1120S

The IRS provides specific guidelines tailored to the reporting requirements of S corporations:

- Correct Year Reporting: Ensure that all financial data pertains to the 2008 fiscal year for proper analysis and historical accuracy.

- Record Adjustments: Include any end-of-year adjustments or corrections to income or deductions from previous filings.

- Audit Preparedness: Ensure that full documentation is readily available should the IRS require proof to support filed positions.

Filing Deadlines and Important Dates

Adhering to deadlines is critical to avoid penalties:

- Regular Filing Deadline: March 15, following the end of the tax year, unless an extension (Form 7004) is filed, allowing a six-month extension.

- Extended Deadlines: September 15 for those that have successfully filed for an extension.

Exception Handling

- Natural Disaster Extensions: Extensions can be granted in case of natural disasters impacting business operations or submitting capabilities.

Submission Methods for the 2008 Form 1120S

Corporations can use multiple methods for submitting Form 1120S, depending on their needs and preferences:

- Electronic Filing (E-file): The IRS encourages e-filing for speed and efficiency. E-filings must be submitted via approved IRS software.

- Mail Submissions: Completed forms can also be mailed to the IRS processing center. Check for the most current mailing address on the IRS website.

- Professional Services: Tax professionals or services like TurboTax and QuickBooks streamline the preparation and submission processes.

Penalties for Non-Compliance with the 2008 Form 1120S

Failure to comply with filing requirements can result in significant penalties:

- Late Filing Penalties: Corporations may face fines for formal lateness, calculated per late month, multiplied by the number of shareholders.

- Incorrect Information: Providing inaccurate information can result in additional assessments and penalties.

- Failure to File K-1s: Each late or missing Schedule K-1 may incur separate penalties, emphasizing the importance of complete and accurate reporting.

By inferring the Forms' specific filing requisites and understanding the essential aspects of compliance, corporations can better ensure they meet their 2008 Form 1120S responsibilities accurately and on time.