Definition and Meaning of Schedule D 2012 Form

The Schedule D (Form 1040) for the year 2012 is primarily used by individuals to report capital gains and losses derived from the sale of assets such as stocks, bonds, and real estate. This form helps taxpayers determine the difference between their gains and losses, organizing them into short-term and long-term categories. This differentiation is crucial because short-term gains are taxed at the individual's ordinary income tax rate, while long-term gains generally benefit from lower tax rates. Proper completion of Schedule D is essential for taxpayers seeking to ensure their net taxable income reflects all necessary gains and losses, accurately impacting their total tax liability.

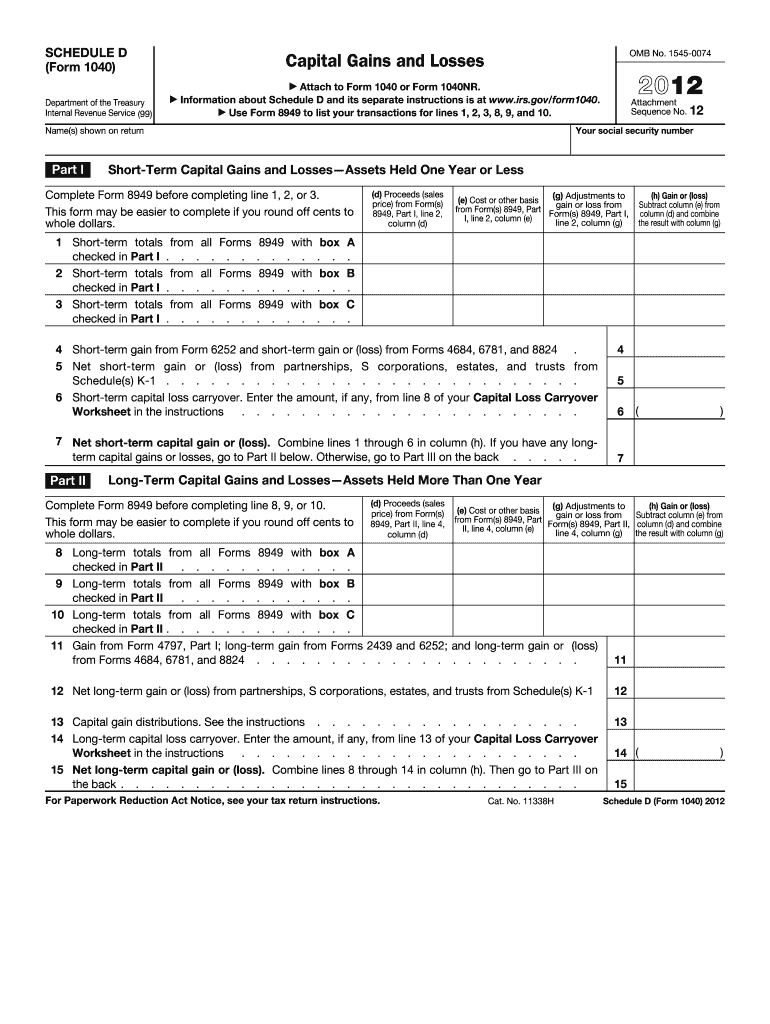

How to Use the Schedule D 2012 Form

To effectively use the Schedule D 2012 form, taxpayers need to follow specific instructions:

-

Gather Necessary Documentation: Collect all records related to the sale or exchange of capital assets. This includes purchase price, sale price, and dates for each transaction.

-

Complete Form 8949: Use Form 8949 to list detailed transaction information. This form serves as a worksheet where each sale or exchange transaction is documented, showing individual gains or losses.

-

Transfer Totals to Schedule D: After completing Form 8949, transfer the summary totals for both short-term and long-term transactions to Schedule D. These totals assist in calculating the net capital gain or loss.

-

Calculate Net Gain or Loss: Deduct any losses from gains to find the net capital gain or loss. If total losses exceed gains, up to $3,000 of the excess can be deducted from ordinary income.

-

Report on Tax Return: The calculated net gain or loss is then reported on the IRS Form 1040, influencing your overall taxable income and tax liability.

Steps to Complete the Schedule D 2012 Form

Completing Schedule D involves several steps:

-

Identify Transactions: Begin by identifying all financial transactions that have resulted in a capital gain or loss during the year. Documentation of each asset's purchase and selling prices, along with dates, will be required.

-

Classify Transactions: Categorize each transaction as either short-term or long-term. Short-term transactions involve assets held for one year or less, while long-term transactions involve assets held for over one year.

-

Enter Data in Form 8949: Form 8949 is divided into multiple sections to account for various reporting needs. Enter each transaction in the applicable part, detailing any necessary adjustments.

-

Compute Totals: Calculate the total amounts of short-term and long-term gains or losses. Form 8949 provides the groundwork for these computations.

-

Complete Schedule D: Transfer totals from Form 8949 to Schedule D. Utilize this form to consolidate the overall gain or loss for the year, distinguishing between taxable and non-taxable amounts.

-

Apply Capital Loss Deduction Limits: If the total capital loss exceeds capital gains, calculate the deductible amount under IRS regulations, allowing specific loss offsets against other income.

Key Elements of the Schedule D 2012 Form

Several key elements are involved in properly using Schedule D:

-

Short-term Gains or Losses: Reflects transactions where assets were held for one year or less. These gains are taxed at ordinary income tax rates.

-

Long-term Gains or Losses: Represents transactions with assets held longer than one year. These gains are eligible for preferential tax rates, typically lower than ordinary income tax rates.

-

Net Capital Gain or Loss: The final figure representing the sum total of all gains and losses, influencing the taxpayer's taxable income.

-

Adjustments and Carryovers: Allows for adjustments for previous losses carried over from prior years, impacting current tax year results.

Who Typically Uses the Schedule D 2012 Form

The Schedule D 2012 form is usually utilized by:

-

Individual Taxpayers: Most commonly used by individuals who have sold investments like stocks, bonds, and real estate and need to report gains or losses.

-

Small Business Owners: Entrepreneurs selling business assets may need Schedule D to report any resulting capital gains or losses.

-

Investors: Frequent stock and real estate investors must report their transactions to ensure compliance with IRS tax regulations.

Required Documents for Completing Schedule D 2012 Form

When preparing the Schedule D 2012 form, taxpayers should have:

-

Purchase Records: Documentation that verifies each asset's purchase price and purchase date.

-

Sale Records: Details of the sale, including sale price and sale date.

-

Broker Statements: Year-end summaries from financial institutions or brokers that document detailed transaction activity for the year.

-

Previous Year Tax Returns: Useful for referencing any capital loss carryovers from prior years.

Filing Deadlines and Important Dates

For the tax year 2012, the filing deadline for Schedule D along with Form 1040 is April 15, 2013. If an extension is required, it must be filed by this date to avoid penalties. If granted an extension, the deadline extends to October 15, 2013, but estimated taxes should still be paid by the original April deadline to avoid interest.

IRS Guidelines for the Schedule D 2012 Form

The IRS provides explicit guidelines to ensure accurate completion:

-

Accuracy: Ensure all lines and entries are completed accurately to prevent errors that could lead to tax discrepancies.

-

Proper Attachment: Attach all required forms, such as Form 8949, to Schedule D, confirming detailed transaction reporting.

-

Adherence to Tax Law: Understand the tax implications and legal requirements for capital gains and losses, following the IRS's established practices and standards.

These comprehensive guidelines and insights into the Schedule D 2012 form provide taxpayers with an essential framework for effectively managing and reporting their capital gains and losses, safeguarding compliance with IRS regulations and ensuring accurate tax filings.