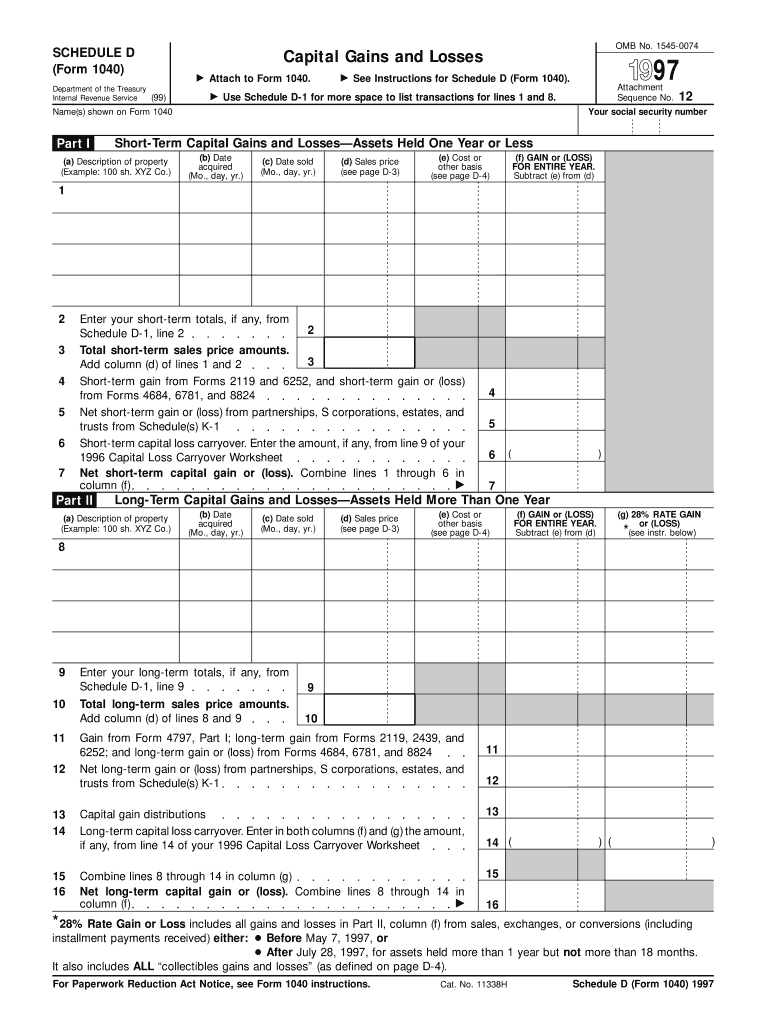

Definition and Purpose of the 1997 Form 1040 (Schedule D)

The 1997 Form 1040 (Schedule D) is a tax form used predominantly by individuals in the United States to report capital gains and losses from the sale of capital assets. These assets can include stocks, bonds, real estate, and other investment securities. The purpose of this form is to help taxpayers calculate their taxable capital gains or deductible capital losses, which ultimately affect their overall tax liability. Schedule D makes it easier to differentiate between short-term and long-term gains or losses, which are subject to different tax rates.

Key Components

- Short-Term Gains/Losses: Results from assets held for one year or less.

- Long-Term Gains/Losses: Results from assets held for more than one year.

- Net Gain/Loss Calculation: Determines the difference between total gains and losses, affecting taxable income.

How to Use the 1997 Form 1040 (Schedule D)

Using the 1997 Form 1040 (Schedule D) requires careful input of financial information to ensure accurate reporting of capital gains and losses. To correctly fill out this form, follow these steps:

- Gather Financial Documents: Collect all necessary documents, including brokerage statements, purchase and sale records, and any supporting documentation for deductible expenses.

- Fill Out Required Sections: Carefully document each transaction, detailing the type of asset, acquisition and sale dates, purchase cost, and sales price.

- Calculate Gains or Losses: For each item, compute the gain or loss by subtracting the cost basis from the sales price, determining whether the result is a gain or loss.

- Determine Holding Period: Classify the gains and losses as short-term or long-term based on the holding period.

- Calculate Net Gains/Losses: Summarize the totals to find your overall net capital gain or loss, which affects your tax liability.

Steps to Complete the 1997 Form 1040 (Schedule D)

The following procedural steps are necessary to accurately complete the 1997 Schedule D:

- Begin with Part I: Enter details of short-term capital gains and losses.

- Proceed to Part II: Document long-term capital transactions.

- Net the Results in Part III: Consolidate results to determine overall capital gain or loss.

- Use the Capital Loss Limitation: If applicable, apply limits on deductible capital losses.

- Double-Check All Entries: Ensure accuracy before transferring totals to Form 1040.

Tips for Accuracy

- Cross-reference entries with original documentation.

- Re-calculate specific entries if numbers do not align.

- Seek guidance if the form instructions are unclear or complex transactions exist.

Key Elements of the 1997 Form 1040 (Schedule D)

Schedule D consists of several crucial elements that taxpayers must understand:

- Transaction Types: Covers various asset transactions, from stocks to real estate sales.

- Date Fields: Accurate acquisition and sale dates are essential for determining tax implications.

- Expense Adjustments: Permits deductions for related expenses like brokerage fees.

Considerations for Complex Situations

- Inherited Assets: Special rules may apply to capital gains on inherited properties.

- Corporate Dividends: Understanding forms of more complex investment income is crucial.

IRS Guidelines for Form 1040 (Schedule D)

The Internal Revenue Service (IRS) outlines specific guidelines to assist taxpayers in completing Schedule D accurately:

- Follow the Instructions: Consult the IRS guidelines provided with the form to avoid missteps.

- Seek Professional Advice: Use certified tax professionals for complex situations to ensure compliance.

- Keep Consistent Records: Regularly update records for clear and accurate transaction reporting.

Adherence to IRS Regulations

- Be aware of the potential for audits and ensure documentation is comprehensive.

- Ensure timely filing to avoid penalties.

Form Submission Methods: Digital and Paper Options

Schedule D allows for both electronic and paper submissions, offering flexibility in the filing process:

- Online Filing: Utilize IRS-sanctioned electronic filing systems for fast and efficient processing.

- Mail Submission: Send completed forms to the designated IRS address, ensuring all entries are precise.

Benefits of Electronic Filing

- Faster processing times and reduced risk of errors.

- Instant confirmation upon receipt by the IRS.

Penalties for Non-Compliance

Failure to properly complete and submit the 1997 Form 1040 (Schedule D) can lead to severe penalties:

- Late Filing Fines: Missing the filing deadline results in compounded penalty fees.

- Inaccurate Reporting: Deliberate inaccuracies may lead to audits or more severe legal consequences.

Taxpayer Scenarios and Use Cases

Different taxpayers, including individuals and businesses, may have unique scenarios when using Schedule D:

- Self-Employed Individuals: Often have diverse portfolios necessitating detailed transaction tracking.

- Retired Persons: May rely heavily on investment returns requiring precise reporting of capital transactions.

Considerations for Businesses

- Limited Liability Companies (LLCs): These businesses need to report capital transactions specific to their entity type.

- Partnerships: Often require careful coordination in capital gain/loss allocations among partners.

By following these guidelines and understanding the details of the 1997 Form 1040 (Schedule D), taxpayers can ensure accurate reporting and compliance with U.S. tax laws, effectively managing their capital gains and losses.