Definition & Purpose of Schedule D

Schedule D (Form 1040) is a critical tax document used by individuals in the United States to report capital gains and losses derived from investment activities throughout the year. This form aids taxpayers in calculating the net gain or loss from sales or exchanges of capital assets, influencing the overall taxable income declared on federal income tax returns. The distinction between short-term and long-term capital transactions is pivotal, as it affects the applicable tax rates. It's essential for individuals who engage in frequent trading of stocks, bonds, real estate, or other investment avenues, providing a comprehensive framework for reporting these activities.

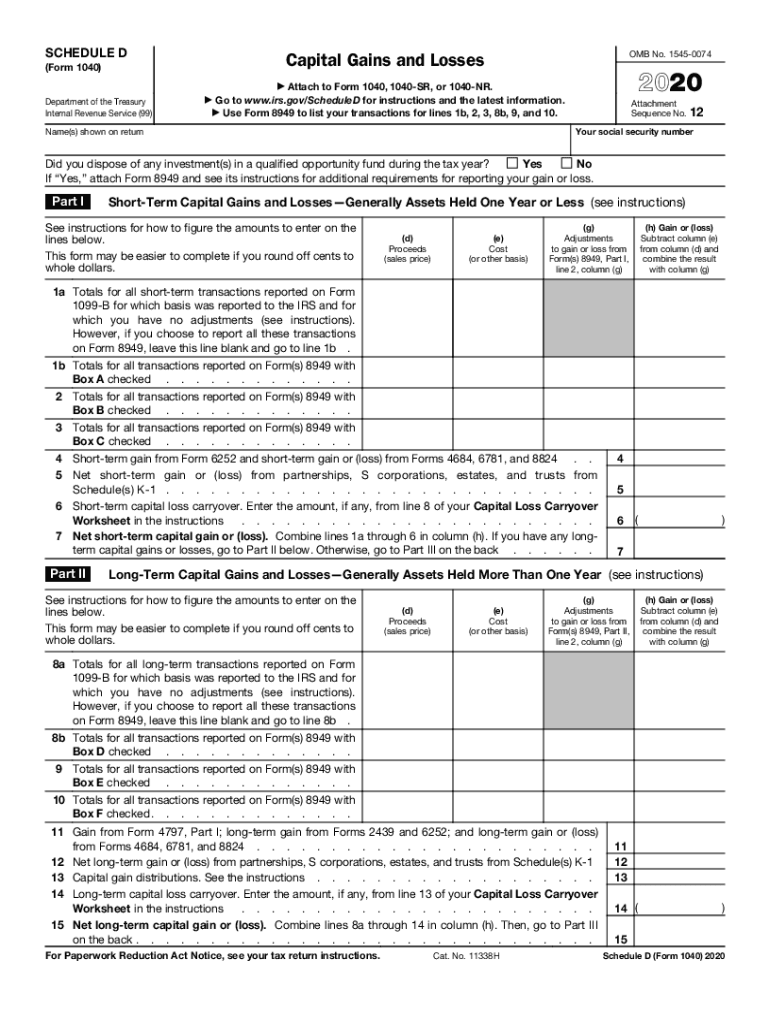

Key Elements of Schedule D

Schedule D is organized into several sections, each dedicated to different aspects of capital gains and losses:

- Part I: Short-term capital gains and losses – tracks transactions involving assets held for one year or less.

- Part II: Long-term gains and losses – involves assets held for more than one year.

- Part III: Summary of gains and losses from previous parts, tax calculation, and integration with Form 1040.

Each section requires detailed data entry, including dates of purchase and sale, acquisition and selling prices, and any adjustments. These details help ensure the accurate reporting of taxable income from investments.

Steps to Complete Schedule D

-

Gather Documentation: Collect all relevant financial documents, including brokerage statements, sale receipts, and acquisition records. These are essential to accurately report each transaction's cost basis, dates, and sale prices.

-

Report Short-term Transactions (Part I):

- List each short-term transaction.

- Enter the purchase and sale dates, along with the relevant amounts.

- Calculate gains or losses for each transaction.

-

Report Long-term Transactions (Part II):

- Detail each long-term transaction similarly to Part I.

- Ensure to differentiate between ordinary income and capital gains when applicable.

-

Complete the Summary (Part III):

- Total the gains and losses from Parts I and II.

- Follow IRS guidelines to determine the applicable tax rate.

-

Review and Confirm Accuracy: Double-check all entries for accuracy and ensure they adhere to the form's instructions.

-

Integrate with Form 1040: Carry over the calculated figures to the appropriate schedule on the Form 1040.

How to Obtain Schedule D

Schedule D is readily accessible through several avenues:

- IRS Website: Downloadable directly from the IRS website as a printable pdf.

- Tax Software: Integrated within most commercial tax preparation software, facilitating digital completion.

- Tax Professionals: Professionals typically have print or digital versions available for client use.

Ensure the downloaded form corresponds to the correct tax year, as changes may occur annually.

IRS Guidelines for Schedule D

The IRS publishes comprehensive instructions alongside Schedule D to guide taxpayers through the form's completion. These guidelines include:

- Definition of capital assets and nuanced rules.

- Instructions for calculating gains and losses.

- Clarifications on offsetting capital losses against gains.

- Details on carrying forward losses to future tax years.

Taxpayers should review these instructions thoroughly before completing the form to ensure adherence to tax laws and minimize errors.

Important Terms Related to Schedule D

Understanding the terminology on Schedule D is crucial for accurate reporting:

- Capital Asset: Broadly encompasses property owned and used for personal or investment purposes.

- Cost Basis: The original value of a capital asset, adjusted for stock splits, dividends, and return of capital distributions.

- Realized Gain/Loss: The amount received from the sale of a capital asset, subtracting the basis, expenses, and any previous depreciation.

- Net Capital Gain: Total gains after losses are subtracted; taxable.

Filing Deadlines / Important Dates

For most taxpayers, Schedule D is due on the same date as Form 1040. The typical deadline is April 15 each year, allowing for extensions under certain conditions. Ensuring timely filing prevents penalties and interest on unpaid taxes.

Penalties for Non-Compliance

Failure to comply with Schedule D reporting can result in:

- Failure-to-file penalty: Charged at five percent of the unpaid tax each month, up to a maximum of 25 percent.

- Failure-to-pay penalty: Typically 0.5 percent per month of unpaid taxes.

- Interest: Accumulates on underpayments and late payments until full settlement.

Accurate completion and timely submission of Schedule D are essential to avoid these financial penalties.

Software Compatibility for Schedule D

Compatibility with tax preparation software like TurboTax and QuickBooks simplifies the completion of Schedule D. These platforms offer guided inputs for each line of the form, error checks, and automatic calculations, reducing the likelihood of mistakes. Software typically updates to reflect changes in tax laws, aiding users in staying current with IRS requirements.

Practical Examples and Scenarios

Schedule D becomes necessary in various scenarios, such as:

- Individual Investors: Individuals with stock trading activities need to report gains and losses through Schedule D.

- Real Estate Transactions: Sales of real estate properties, unless exempt under the primary residence rules.

- Inherited Assets: Special considerations for stepped-up basis calculations.

These examples illustrate the diverse applications and compliance scenarios for Schedule D, emphasizing its importance in individual tax reporting.