Definition & Meaning

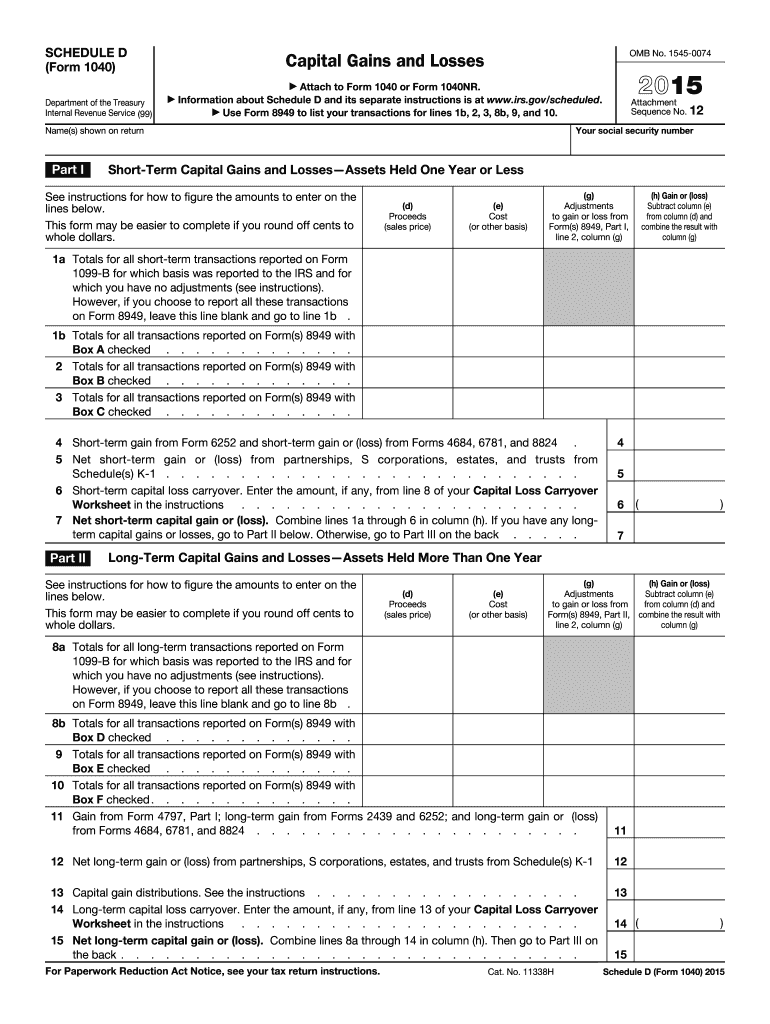

The 2015 Schedule D form is part of the federal tax filing process in the United States. It is used to report capital gains and losses incurred by individuals, partnerships, and corporations from the sale or exchange of assets. The form helps taxpayers compute their total capital gain or loss, which ultimately affects the amount of tax owed or refunded.

Types of Assets Covered

- Stocks and Bonds: Transactions involving the sale of stocks and bonds.

- Real Estate: Sale or exchange of real property.

- Personal Assets: Includes collectibles, art, or other long-term holdings.

Importance of Accurate Reporting

Accurate completion of Schedule D is essential, as incorrect reporting can lead to penalties or affect your tax liability. It details both short-term capital gains or losses (assets held for one year or less) and long-term transactions (assets held for more than one year).

How to Use the 2015 Schedule D Form

To use the Schedule D form effectively, follow a series of steps designed to ensure accuracy and compliance with IRS regulations.

Step-by-Step Instructions

- Gather All Transaction Records: Collect documentation for every asset sale or exchange, such as purchase price, sale price, and related expenses.

- Enter Short-Term Transactions: For each asset held for a year or less, report the sale on Part I of Schedule D.

- Enter Long-Term Transactions: For assets held for more than a year, complete Part II with relevant transaction details.

- Calculate Totals: Compute net short-term gains or losses and net long-term gains or losses.

- Transfer Totals to Form 1040: Input finalized amounts from Schedule D to the corresponding sections in your main tax return, Form 1040.

Practical Example

An example might include selling shares purchased last year, reporting the gain or loss under Part I, while a home sold after several years is accounted for under Part II of Schedule D.

Steps to Complete the 2015 Schedule D Form

Completing the Schedule D form involves organizing your financial information and following the IRS guidelines set for 2015.

Required Details

- Personal Information: Name, Social Security Number, and tax filing period.

- Asset Sale Information: Sale price, purchase price, and date of sale.

- Capital Gains or Losses: Calculate using the formula: sale price - purchase price.

Comprehensive Breakdown

- Capital Gain Tax Calculation: The tax rate may differ for short-term versus long-term gains. Short-term gains are taxed at ordinary income tax rates, whereas long-term gains might benefit from reduced tax rates.

- Carrying Losses Forward: If capital losses exceed capital gains, the excess amount might be carried forward to offset future gains.

Important Terms Related to 2015 Schedule D Form

Understanding key terms can simplify the process of filling out the form and ensure compliance.

Glossary of Terms

- Capital Gain: The profit from selling an asset.

- Capital Loss: The loss incurred when an asset sells for less than its purchase price.

- Basis: The original cost or investment in the property.

- Capital Gain Tax Rate: The tax percentage charged on a capital gain, varying based on income level and type of gain.

Examples in Context

- Short-Term vs. Long-Term: Classifying an asset held for six months as short-term, unlike an heirloom kept for 20 years, which would be long-term.

Filing Deadlines / Important Dates

Recognizing the critical deadlines for filing the 2015 Schedule D form ensures timely compliance.

Annual Filing Date

- April 15, 2016: Standard deadline for individual tax filing.

- Extensions: Filing Form 4868 can provide additional time until October.

Impact of Late Filing

Missing the deadline without an extension can lead to interest and penalties on unpaid tax amounts, emphasizing the importance of timely submission.

Required Documents

Collecting all necessary documentation is crucial for accuracy and thoroughness.

Document Checklist

- 1099-B Forms: Provided by brokers or barter exchanges, detailing completed transactions.

- Form 8949: To reconcile transactions and discrepancies.

- Receipts: Original purchase and sale receipts.

- Cost Basis Records: Documentation evidencing the original purchase price of assets.

Document Insights

Keeping records organized simplifies the review process and supports the accuracy of tax reporting, especially during audits or reviews by the IRS.

Who Typically Uses the 2015 Schedule D Form

The form is predominantly used by individuals dealing with numerous types of capital asset transactions.

Common User Profiles

- Investors: Frequently buy and sell stocks or other investments.

- Retirees: May liquidate assets to fund retirement accounts.

- Business Owners: Selling business assets and reporting profits or losses.

Real-World Scenarios

- An individual who sells off multiple stock shares during the year would need to document each transaction and report cumulative results in the prescribed manner.

IRS Guidelines

The IRS places importance on providing taxpayers with comprehensive guidelines to ensure proper completion of Schedule D.

Compliance Requirements

- Instructions for Schedule D: IRS documents offer explicit instructions, which should accompany the form during preparation.

- Form 8949 Integration: Utilize for detailed asset disposition records and error corrections.

Importance of Adherence

Following established guidelines minimizes errors and reduces the chances of audits or penalties, ensuring a smoother tax filing experience.