Definition and Meaning

The 2010 Schedule D Form, commonly known within the tax context, is part of the IRS Form 1040 series used to report capital gains and losses. This document is crucial for individual taxpayers who have engaged in transactions involving the sales or exchanges of capital assets. The form provides specific sections to record both short-term (assets held for one year or less) and long-term (assets held for more than one year) capital gains and losses. By facilitating an accurate calculation of net capital gains or losses, the 2010 Schedule D Form plays an integral role in determining an individual's tax liability.

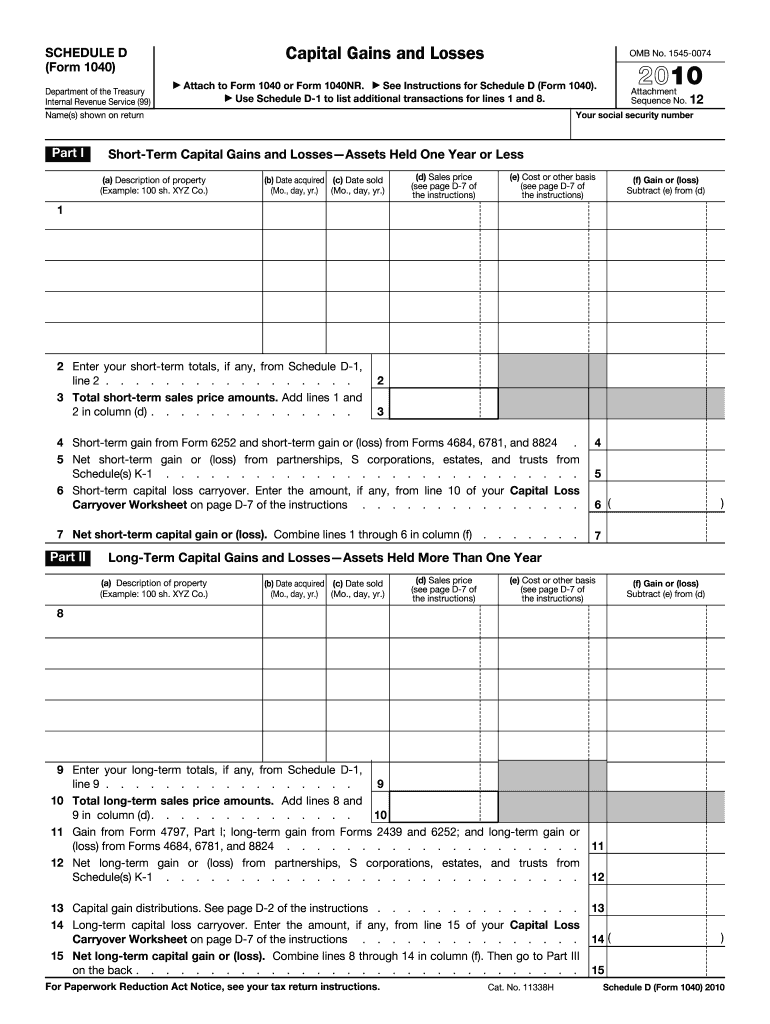

How to Use the 2010 Schedule D Form

To effectively use the 2010 Schedule D Form, you must first gather all relevant information regarding any capital asset transactions you participated in during the tax year. This includes sales of stocks, bonds, and property or any securities that resulted in a gain or loss. Follow these steps to complete the form:

- List Transactions: Record each transaction involving capital assets, specifying whether it was short- or long-term.

- Calculate Gains and Losses: For each asset, calculate the difference between the selling price and the purchase price.

- Total the Results: Sum all short-term gains and losses separately from long-term gains and losses.

- Net Gains and Losses: Combine these totals to compute your net capital gain or loss, which affects your taxable income.

It is essential to carefully follow the IRS instructions included with the form to ensure that it is filled out accurately.

Steps to Complete the 2010 Schedule D Form

Completing the 2010 Schedule D Form requires meticulous attention to detail to accurately report financial transactions:

- Obtain Necessary Documents: Gather forms 1099-B or 1099-S, brokerage statements, and any other records showing transaction details.

- Fill in Part I: Report all short-term capital gains and losses, using the transaction details from your documentation.

- Complete Part II: Report all long-term gains and losses, similarly ensuring all transactions are documented properly.

- Total and Transfer Figures: Calculate totals for each section and transfer them to Form 1040 to determine overall tax liability.

- Review and Attach: Carefully review the completed form for accuracy and attach it to your Form 1040 when filing.

Required Documents for the 2010 Schedule D Form

To accurately complete the 2010 Schedule D Form, it's important to prepare these documents:

- Form 1099-B: Reports proceeds from broker-managed sales.

- Form 1099-S: For sales of real estate transactions.

- Receipts and Records: Details of purchase prices and sale prices for each transaction.

- Brokerage Statements: Provide a summary of your trading activity and help track gains or losses accurately.

Having these records on hand will facilitate the accurate completion of the form.

IRS Guidelines for the 2010 Schedule D Form

The IRS provides specific guidelines on completing the 2010 Schedule D Form, ensuring that taxpayers adhere to proper reporting practices. Key points include:

- Tax Rates: Different capital gains tax rates apply depending on the holding period, impacting your overall tax liability.

- Exception Management: Certain exceptions apply, such as the exclusion of certain collectibles, qualified small business stock, and section 1202 gains.

- Carrying Losses Forward: Instruction on how to carry forward losses to offset future gains, which can lower taxable income in subsequent years.

Adhering to these detailed guidelines ensures compliance and minimizes errors or penalties.

Penalties for Non-Compliance with the 2010 Schedule D Form

Failing to properly complete or file the 2010 Schedule D Form may result in penalties or interest charges. The IRS imposes penalties in cases of:

- Omission or Underreporting: Not reporting taxable gains or improperly deducting losses.

- Late Filing: Failing to include the form with your income tax return by the due date.

- Inaccuracies and Misrepresentations: Deliberate or reckless inaccuracies could lead to audits or legal actions.

Understanding these potential penalties is key to maintaining compliance with IRS filing requirements.

Digital vs. Paper Version

The 2010 Schedule D Form is available as both a digital and paper version, each providing distinct benefits:

- Digital Version: Offers convenience as it can be completed and filed electronically using tax preparation software. This version reduces errors through automated calculations and formatting.

- Paper Version: Suitable for those who prefer traditional filing methods. While it involves more manual effort, it provides a tangible copy of your records.

Choosing between digital and paper versions depends on personal preference and access to technology.

Examples of Using the 2010 Schedule D Form

Several scenarios illustrate the application of the 2010 Schedule D Form:

- Individual Stock Sale: An investor sells stock purchased ten months prior, resulting in a short-term gain, and uses Schedule D to calculate taxes owed.

- Home Sale: A homeowner sells a residence held for five years, reporting a profit as a long-term capital gain. Entry into Schedule D facilitates appropriate tax calculations.

- Inheritance Sales: Assets inherited and sold are evaluated using special considerations on Schedule D for their unique tax implications.

By demonstrating how these diverse situations interact with the form, users can better understand their reporting duties.