Definition & Meaning

Schedule D (Form 1040) is an essential document for taxpayers to report capital gains and losses incurred from the sale of assets. It is attached to the primary tax form, Form 1040, or Form 1040NR for non-residents, and helps determine the tax implications of these transactions. This form categorizes gains and losses into short-term and long-term, based on the duration for which assets were held. The distinction is critical as it affects the tax rates applied.

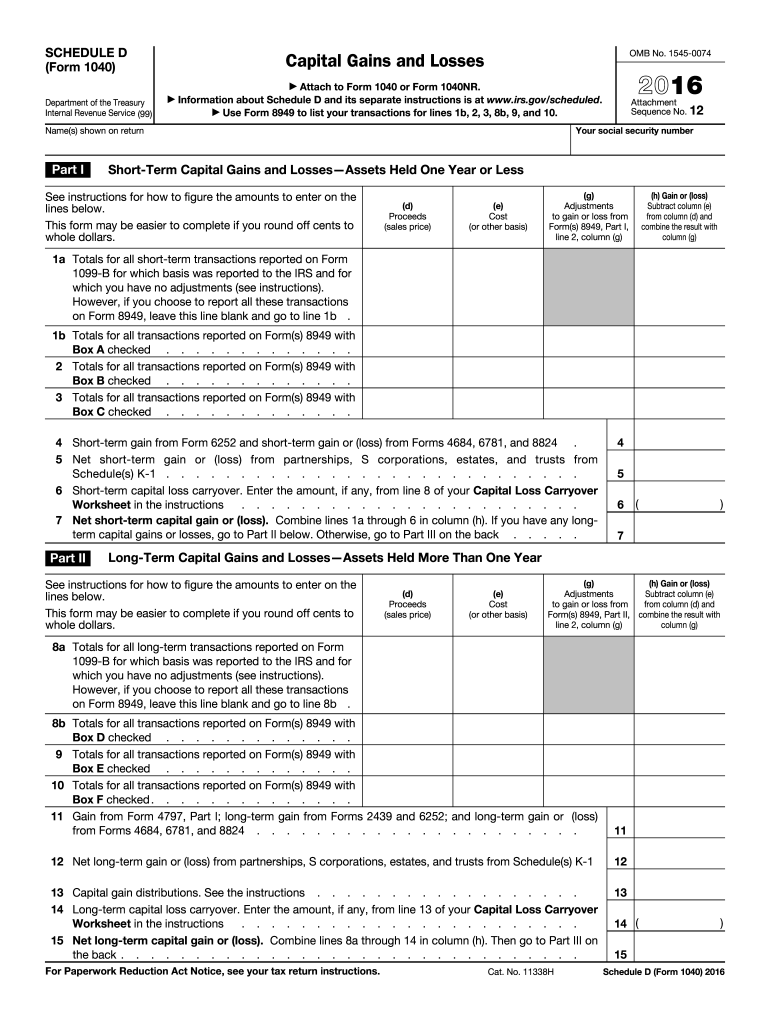

How to Use the Schedule D 2016 Form

To use the Schedule D 2016 form effectively, taxpayers must first gather relevant information about their asset transactions during the tax year. This includes dates of acquisition and sale, cost basis, and proceeds from the sale of assets. The form requires details of these transactions to calculate the gain or loss realized. Taxpayers then transfer these results to specific lines on their Form 1040, which integrates the outcomes into their overall tax computation. Utilizing form instructions can greatly aid in accurate completion and compliance.

Steps to Complete the Schedule D 2016 Form

- Collect Transaction Data: Gather all necessary records, including purchase and sale dates, and financial amounts associated with each asset.

- Classify Transactions: Divide the transactions into short-term and long-term categories.

- Calculate Gains and Losses: Enter the cost basis and sale proceeds for each asset to compute your gains or losses.

- Complete Form Sections: Fill out respective sections for each type of transaction, referencing instructions if needed.

- Transfer Figure to Tax Forms: Total your gains and losses and carry these amounts to the relevant sections of Form 1040.

Important Terms Related to Schedule D 2016 Form

- Capital Gain: The profit from the sale of a capital asset, subject to taxation.

- Capital Loss: The loss incurred from selling an asset for less than its cost basis.

- Cost Basis: The original value of an asset, representing its purchase price plus any associated costs.

- Short-term Transaction: A transaction involving an asset held for one year or less.

- Long-term Transaction: A transaction involving an asset held for more than one year.

IRS Guidelines

The IRS provides explicit guidelines for completing Schedule D, outlining the requirements for reporting transactions and any exceptions or special conditions. These guidelines also explain the various types of capital gains and losses, applicable tax rates, and potential implications for underreporting. Taxpayers should refer to the IRS instructions for detailed clarifications regarding more complex scenarios, like wash sales, and ensuring all transactions comply with federal requirements.

Filing Deadlines / Important Dates

The filing deadline for submitting Schedule D along with Form 1040 typically aligns with the federal tax filing deadline, usually by April 15th of the following calendar year. If the deadline falls on a weekend or holiday, it is extended to the next business day. Taxpayers can request an extension but should be aware that this only extends the time to file, not to pay any taxes owed.

Required Documents

To accurately complete Schedule D, taxpayers need several key documents, including:

- 1099-B Forms: Issued by brokers or barter exchanges, outlining proceeds from sales.

- Purchase Receipts: Documentation of original asset purchases to establish cost basis.

- Any Related Tax Documentation: Such as Form 1099-DIV for dividend income attributed to capital gains.

Penalties for Non-Compliance

Failing to properly complete and submit Schedule D on time can result in significant penalties. Non-compliance may lead to interest charges on overdue amounts, as well as financial penalties assessed based on the degree of negligence or fraud. Inaccurate or incomplete reporting can also trigger an IRS audit. Taxpayers should ensure all details are accurate and seek professional advice if uncertain about any part of the process.

Digital vs. Paper Version

Both digital and paper versions of Schedule D are available for taxpayers, offering flexibility in how the form is completed and submitted. Digital submissions provide a streamlined process with potential integration with tax software, which can reduce errors and save time. Meanwhile, paper submissions still offer a traditional approach for those who prefer a physical form or have limited access to technology. However, electronic filing is generally recommended for quicker processing and verification.