Definition and Meaning

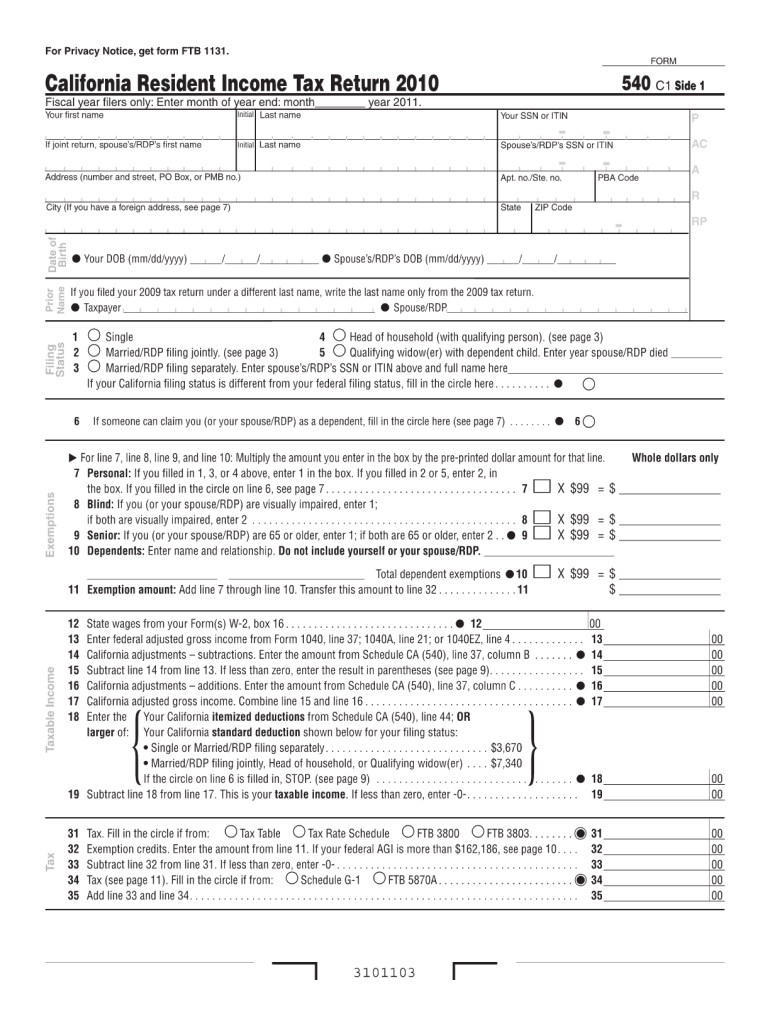

Form 540 from the year 2010 is known as the California Resident Income Tax Return. This document is used by residents of California to report their income, calculate their state income tax obligations, and identify any tax credits for the given tax year. Form 540 serves as the primary tax document for individual taxpayers residing in California, ensuring compliance with state tax laws and requirements. It is a pivotal element in documenting yearly tax computations and submitting necessary details to the California Franchise Tax Board (FTB).

How to Use the 540 Form 2010

To effectively utilize the Form 540 for filing purposes, a taxpayer needs to follow a series of steps that include gathering necessary financial documentation, accurately filling out each section such as personal information, income details, deductions, and tax credits, and confirming calculations to ensure correct tax liability. Here's an outline of its utilization:

- Gather Financial Documents: Collect relevant documents like W-2s, 1099s, and records of deductions.

- Enter Personal Information: Fill out sections with your name, Social Security Number, and address.

- Calculate Income: List all sources of income to provide a total taxable income.

- Identify Deductions: Deduct applicable expenses (e.g., student loan interest, mortgage interest) to reduce tax owed.

- Apply Credits: Utilize eligible tax credits to decrease the tax obligation.

- Verify Calculations: Double-check all figures to ensure accuracy before submission.

Important Terms Related to 540 Form 2010

Understanding specific terminology associated with Form 540 can aid taxpayers in correctly filling out the document and ensuring accurate tax reporting. Key terms include:

- Taxable Income: The portion of your gross income subject to state tax, after deductions.

- Exemptions: Allowances that reduce the amount of taxable income, such as personal or dependent exemptions.

- Tax Credit: A direct reduction in tax liability, which can be specific to clients, such as educational credits.

- California Adjusted Gross Income (CAGI): A taxpayer's total income adjusted specifically for California tax codes and regulations.

Steps to Complete the 540 Form 2010

Completing the form requires careful attention to detail and an understanding of the information required for each section. The steps include:

- Enter Basic Personal Information: Begin with your full name, address, and taxpayer identification.

- Filing Status: Choose the appropriate status—single, married filing jointly, married filing separately, etc.

- Income and Wages: Report total income as documented on your W-2 or 1099 forms.

- Adjustments and Deductions: Complete sections that allow adjustments to gross income and list deductions.

- Calculate Tax: Using the provided tax tables or software, calculate the state income tax due.

- Credits and Overpayments: Apply any eligible credits to decrease liabilities and note any overpayments for refunds.

Eligibility for Using the 540 Form 2010

Eligibility to file Form 540 hinges on several criteria. It's essential to know if you meet requirements to file accurately:

- Residency Requirement: Primarily for full-year residents of California.

- Income Thresholds: Must pass specific income levels necessitating tax returns.

- Age and Dependent Status: Considerations vary for dependents or taxpayers of specific age categories.

- Filing Status: Must be aligned with IRS filing status, including details like dependents and marital status.

Examples of Using the 540 Form 2010

Real-world applications demonstrate various scenarios in which Form 540 is utilized:

- Married Residents: A couple living in California might utilize joint filing to maximize their exemption benefits and tax credits, helping to reduce their taxable income.

- Self-Employed Individuals: Such individuals can deduct legitimate business expenses, reporting these on the form to lower tax dues.

- Retired Californians: Utilize specific tax credits if residing permanently in California, with considerations on interest from state-issued bonds which might remain non-taxable.

Filing Deadlines and Important Dates

Timely filing of Form 540 is necessary to avoid penalties. Key dates include:

- April 15: Standard deadline for submission, mirroring the federal tax deadline.

- Extensions: While no automatic federal extensions apply, California permits extension requests to October 15.

- Quarterly Payments: Specific individuals may be required to submit estimated taxes quarterly.

Penalties for Non-Compliance

Failure to comply or submit Form 540 on time results in consequences:

- Late Filing Penalties: A percentage of owed taxes plus interest applied for each month past the deadline.

- Fraudulent Filing Penalties: Severe penalties for willful deceit in reporting taxable income.

- Interest on Late Payments: Accrual of interest charges on tax owed if payment deadlines are missed.

By adhering to these sections, one ensures comprehensive understanding and correct filing of the Form 540 for the year 2010, adhering to tax regulations and requirements set forth by California state law.