Definition and Purpose of Form 1098

Form 1098, known as the Mortgage Interest Statement, is utilized by lenders to report mortgage interest received from borrowers. This form is crucial in the United States, as it plays a significant role in the tax reporting process for both lenders and borrowers. From a borrower's perspective, the information provided on a Form 1098 can potentially qualify them for tax deductions, specifically on the interest paid on their mortgage loans. It is pertinent for lenders to ensure that all details are accurately recorded to comply with IRS guidelines and facilitate a smooth tax filing process for borrowers.

How to Use Form 1098 Effectively

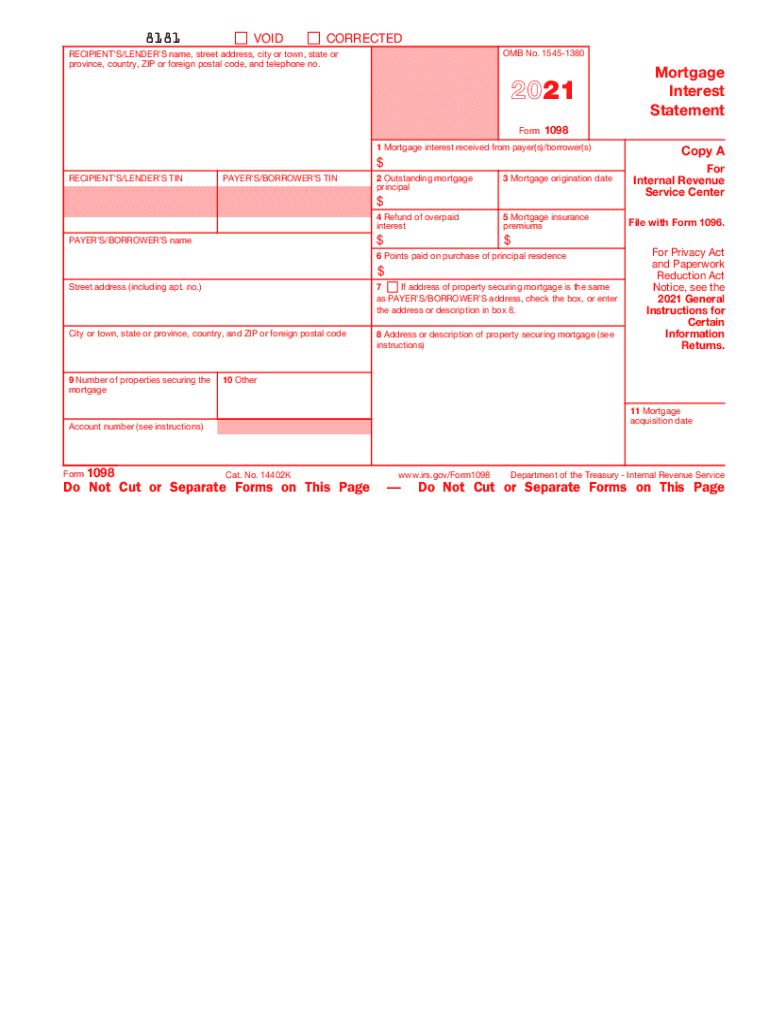

Using Form 1098 effectively requires understanding its layout and the information it contains. The form includes details such as the borrower's name, address, and taxpayer identification number, as well as the lender's information. Crucially, it specifies the mortgage interest received in the calendar year, points on the principal residence, and any mortgage insurance premiums. Borrowers should utilize these entries to verify the interest deduction on their tax returns, while lenders must ensure the information aligns with IRS regulations to avoid potential discrepancies and penalties.

Step-by-Step Completion Process

- Verify Lender Information: Ensure the lender’s name, address, and taxpayer identification number are correct.

- Borrower Details: Check the borrower's information for accuracy, including name, address, and TIN.

- Mortgage Interest: Accurately record the total mortgage interest received during the year.

- Points on Principal Residence: Detail any points paid that are not reported elsewhere.

- Adjustments and Corrections: Document any necessary adjustments or corrections for the tax year.

How to Obtain Form 1098

Lenders are responsible for issuing Form 1098 to borrowers, typically by January 31 of the year following the tax period. This process involves compiling all necessary mortgage interest data for each borrower. Forms are usually sent via mail or electronically, depending on the lender’s policy. Borrowers receiving a Form 1098 should review it carefully for any discrepancies and contact the lender for corrections if needed. It's advisable for borrowers to retain a copy for their personal records and tax filing needs.

Key Elements of Form 1098

Understanding the core components of Form 1098 is vital for accurate completion and reporting. The form must include the mortgage interest amount, points paid on the purchase of the borrower's principal residence, and mortgage insurance premiums, if applicable. Each section should be filled with precision to ensure compliance with IRS requirements. Any omitted or incorrect fields can lead to issues in the borrower’s ability to claim deductions, highlighting the need for thoroughness in form completion.

IRS Guidelines for Reporting

The IRS requires precise reporting on all 1098 forms submitted by lenders. This includes meeting filing deadlines, accurately reflecting interest amounts, and maintaining clear records. Compliance with these guidelines ensures avoidance of penalties and supports the borrower's deduction claims. The IRS scrutinizes these forms to ensure taxes are assessed properly, making adherence to guidelines mandatory for lenders.

Filing Deadlines and Important Dates

- January 31: Deadline for lenders to furnish Form 1098 to borrowers.

- February 28: Deadline for paper filing with the IRS.

- March 31: Deadline for electronic filing with the IRS.

Legal Obligations and Compliance

Lenders are legally obligated to issue Form 1098 to any borrower who has paid over $600 in mortgage interest during the tax year. This obligation is rooted in ensuring the federal government accurately tracks income and deductions. Non-compliance, such as failure to issue the form or incorrect reporting, can result in substantial legal and financial penalties for lenders.

Penalties for Non-Compliance

Non-compliance with Form 1098 requirements can lead to significant penalties for lenders. Common issues include late filing, filing incorrect information, or failing to provide a copy to borrowers. The IRS may impose fines, which can accumulate quickly, depending on the severity and frequency of the violations. Therefore, diligence in completing and submitting Form 1098 is crucial.

Examples of Using Form 1098

Case Study: Self-Employed Borrower

A self-employed individual uses their Form 1098 to accurately report mortgage interest paid on their home office. The form's clarity aids in maximizing their deductions, illustrating the form's value in varying tax scenarios. This example underlines the importance of transparency and accuracy in Form 1098 for different taxpayer profiles.

State-Specific Considerations

While Form 1098 is a federal requirement, some states may have additional deductions or benefits not reflected federally. Borrowers should consult with tax professionals familiar with state-specific tax regulations to ensure they leverage all potential benefits. An understanding of regional differences can be particularly beneficial for maximizing tax advantages associated with mortgage interest deductions.