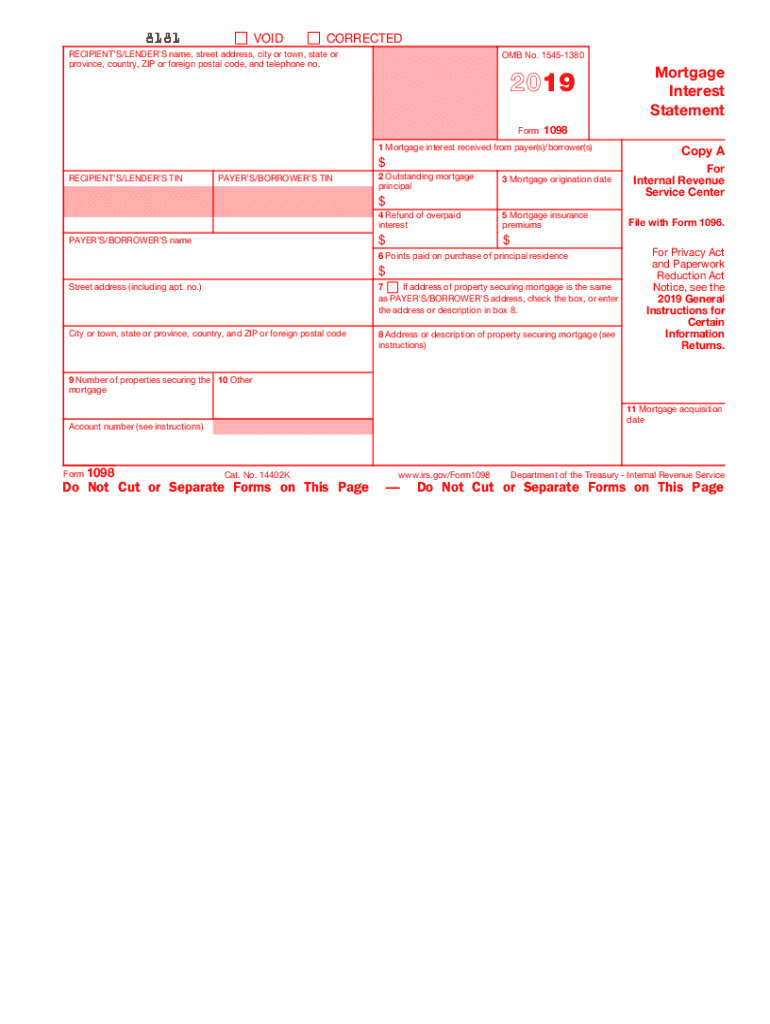

Definition & Meaning

The IRS Form 1098, also known as the Mortgage Interest Statement, is a crucial tax form used in the United States for reporting mortgage interest payments. When taxpayers, especially homeowners, pay $600 or more in mortgage interest to a singular lender over a year, the lender will send them a Form 1098 to report the interest paid. This form is pivotal for borrowers because it can often facilitate the deduction of mortgage interest from their taxable income, leading to potential tax savings. By scheduling IRS Form 1098, lenders and borrowers properly coordinate the timely reporting and documentation of mortgage-related financial activities, ensuring tax compliance.

How to Use the Schedule A IRS Form 1098

Utilizing IRS Form 1098 requires careful data entry and verification to maximize tax benefits and ensure compliance. Here's how to effectively use the form:

- Reviewing the Form: Examine all sections, including mortgage interest, loan origination fees, and any refunds of overpaid interest.

- Cross-Verification: Compare reported data with personal records, such as year-end mortgage statements, to ensure accuracy.

- Utilizing for Tax Deductions: Document interest paid as a deduction on Schedule A during tax return filing, providing all necessary substantiation.

- Record Keeping: Retain copies of completed forms and associated documents for future references or audits.

How to Obtain the Schedule A IRS Form 1098

Acquiring IRS Form 1098 is generally straightforward, especially for borrowers who have paid substantial mortgage interest:

- From Your Lender: Typically, lenders automatically send Form 1098 to borrowers by January 31 of the calendar year.

- Online Access: Many lenders provide electronic access to tax documents via their online banking platforms.

- Request Copies: If the form is not received, directly contact the lender or financial institution and request a duplicate.

- IRS Resources: The IRS website offers resources and guidance for form retrieval and completion queries.

Steps to Complete the Schedule A IRS Form 1098

Filling out Form 1098 accurately is essential to ensure compliance and benefit from potential tax deductions:

- Gather Your Documentation: Accumulate all relevant financial documents from the tax year, including mortgage statements and financial transactions.

- Enter Personal Information: Fill in identifying information for both the borrower and lender.

- Detail the Interest Paid: Accurately record total mortgage interest paid within the year.

- Submit Filing: Ensure all entries are complete and correct before filing as part of your tax return, retaining copies for personal records.

Why Should You Schedule a IRS Form 1098

Scheduling IRS Form 1098 is essential for proper tax management and compliance. Doing so ensures:

- Accurate Reporting: Facilitates precise tracking and reporting of mortgage interest payments.

- Tax Deduction Optimization: Enables the potential reduction of taxable income through interest deductions.

- Organized Record-Keeping: Provides a systematic approach to document management and retrieval, simplifying the tax filing process.

Who Typically Uses the Schedule A IRS Form 1098

IRS Form 1098 is widely used by individuals and entities involved in mortgage transactions, including:

- Homeowners: Taxpayers paying significant mortgage interest.

- Lenders: Financial entities facilitating mortgage agreements.

- Tax Professionals: Accountants and advisors assisting clients in financial management and tax planning.

Key Elements of the Schedule A IRS Form 1098

Understanding the critical components of Form 1098 enhances accurate filling and reporting:

- Borrower Information: Must include the taxpayer’s identifying data, such as name and taxpayer identification number.

- Lender Information: Details about the lender or financial institution issuing the mortgage.

- Mortgage Interest and Points Paid: Specific fields dedicated to the amounts paid within the tax year.

- Loan Origination Fees and Refunds: Documentation of any fees or refunded amounts impacting the total interest paid.

IRS Guidelines

The IRS outlines precise regulations governing the usage and submission of Form 1098, including:

- Filing Requirements: Lenders must submit the form for borrowers paying $600 or more in interest.

- Use of Originals: Copy A must adhere to IRS guidelines, while other copies may be used for recipients.

- Deadline Adherence: Specific filing and delivery deadlines are enforced to ensure timely processing and penalty avoidance.

Filing Deadlines / Important Dates

The timing for submitting Form 1098 is critical in maintaining compliance:

- Form Distribution: By January 31, borrowers must receive the form from the lender.

- Electronic Filing: IRS requires forms to be submitted electronically by February 28.

- Tax Filing Inclusion: Utilize form details within annual tax returns, adhering to IRS timelines for submissions.

Penalties for Non-Compliance

Failing to comply with IRS requirements for Form 1098 can lead to significant financial penalties:

- Inaccurate Reporting: Incorrect or fraudulent form details may incur penalties or audits.

- Late Submissions: Delayed filings either by lenders or on personal tax returns result in fines.

- Missing Filings: A failure to provide the necessary forms altogether draws substantial penalties from the IRS.

Examples of Using the Schedule A IRS Form 1098

Understanding the practical aspects of Form 1098 use helps clarify its role in financial strategies:

- Home Purchase: Recording mortgage interest for newly acquired properties to capitalize on tax relief.

- Refinancing: Use subsequent Form 1098 submissions for interest deductions on refinanced mortgages.

- Investment Properties: Often involved in reporting for tax purposes concerning rental income and expenses.

This comprehensive structure ensures that users are well-informed about the integral components and uses of Schedule A IRS Form 1098, facilitating better understanding and accurate completion.