Definition and Meaning

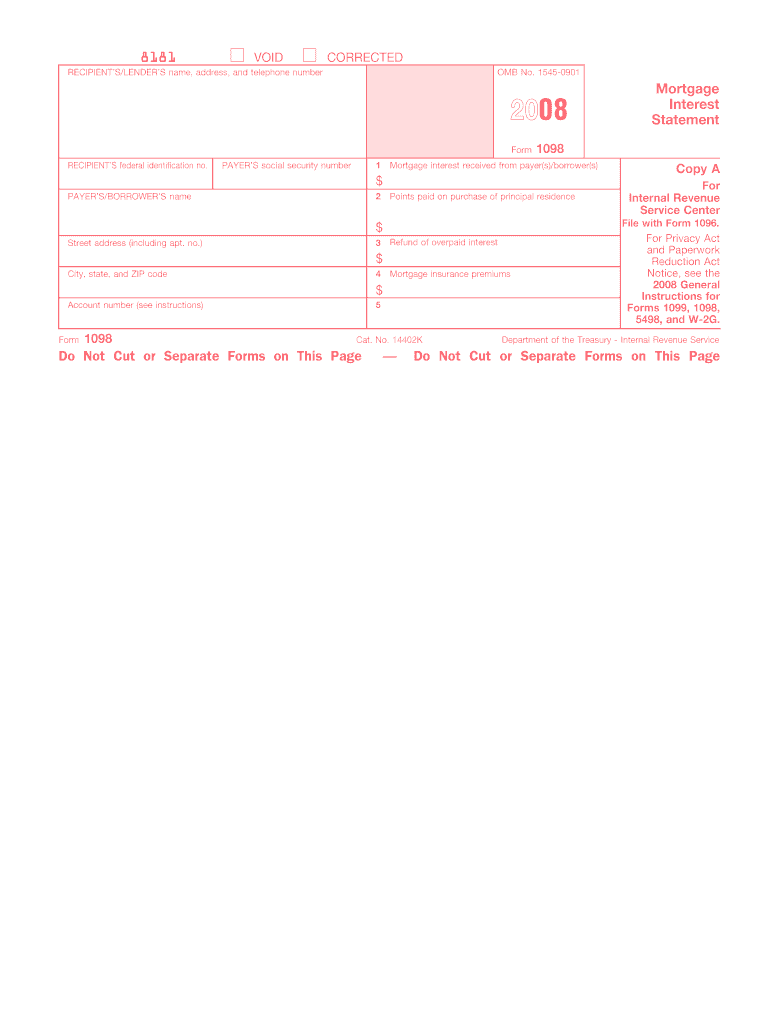

The 2008 Form 1098, titled the "Mortgage Interest Statement," is a crucial document used in the United States tax system. Lenders utilize this form to report the amount of mortgage interest received from borrowers over the tax year. This form serves as an essential record for both lenders and borrowers, detailing mortgage interest, points paid during the purchase of a primary residence, any refunds of overpaid interest, and mortgage insurance premiums. These details are necessary for tax purposes, primarily to assist borrowers in claiming deductions on their federal tax returns.

How to Use the 2008 Form 1098 Mortgage Interest

The form plays a vital role in tax preparation for both lenders and borrowers. For borrowers, the information contained within the form is used to determine the amount of mortgage interest they can deduct on their tax return. Deductibility is based on the interest and points reported, potentially providing significant tax savings. Borrowers should include the amounts reported on Form 1098 when completing their Schedule A for their individual income tax return, especially when itemizing deductions. Lenders must ensure accuracy in the details reported to avoid discrepancies that might trigger audits or questions from the IRS.

How to Obtain the 2008 Form 1098 Mortgage Interest

Typically, lenders are responsible for issuing Form 1098 to borrowers by the end of January following the tax year in question. Borrowers do not generally need to request the form, as lenders must automatically provide it. However, if you haven’t received your Form 1098, contact your mortgage lender to request it. In some cases, lenders might offer digital copies through their online accounts systems, allowing easier access and retrieval without waiting for mail delivery.

Steps to Complete the 2008 Form 1098 Mortgage Interest

Completing this form accurately is primarily the responsibility of the lender. The form comprises several sections requiring detailed information. Here is an outline of the essential steps for completing the form:

- Identification Details: Include the lender's name, address, and taxpayer identification number (TIN).

- Borrower's Information: Enter the borrower's name, address, and TIN.

- Mortgage Details: Provide the mortgage account number, matching your records with borrower documentation.

- Interest Paid: Record the total interest received over the calendar year.

- Points Paid: Specify any points received on purchase loans, relevant to the primary residence.

- Refunds: Note any refunds of overpaid interest or similar adjustments.

- Mortgage Insurance Premiums: Include any premiums paid for mortgage insurance if applicable.

Who Typically Uses the 2008 Form 1098 Mortgage Interest

This form is predominantly used by taxpayers who have paid interest on a mortgage for their primary home. The primary users include homeowners who have opted to itemize their deductions on their tax return, allowing them to claim any relevant interest paid as a deduction, reducing their taxable income. For lenders and mortgage holders, this form is a required report to the IRS, ensuring that the tax implications of interest payments are accounted for.

Key Elements of the 2008 Form 1098 Mortgage Interest

Understanding the key components of the form is crucial for both lenders and borrowers:

- Box 1: States the amount of mortgage interest received.

- Box 2: Reflects the total principal amount of the mortgage as of the beginning of the year.

- Box 3: Contains information about mortgage origination date if originated after 2022.

- Box 4: Details any refunds for overpaid interest.

- Box 5: Shows premiums paid for mortgage insurance.

- Box 6: Other points specifically related to the loan.

Legal Use of the 2008 Form 1098 Mortgage Interest

Legally, this form facilitates transparency and accuracy in tax reporting for mortgage payments. Both borrowers and lenders must ensure that the figures reported on this form align with the actual transactions made during the tax year. The integrity of this data is critical for compliance with IRS requirements, serving as a documentation basis for potential audits and reviews by tax authorities. The ESIGN Act governs the electronic submission and signature processes to maintain legality in digital document handling.

IRS Guidelines

The Internal Revenue Service (IRS) provides specific instructions regarding the Form 1098, emphasizing the importance of correct filing and reporting. Lenders are required to submit a copy of all issued Form 1098 to the IRS, ensuring consistency and accuracy between the taxpayer's claim and what's reported. IRS guidelines also determine how deductions from this form influence a taxpayer's final owed amount. It’s critical for taxpayers to keep detailed records that match the reported mortgage interest and any other related financial activity to ensure accuracy and compliance.

Filing Deadlines and Important Dates

The filing deadlines for the Form 1098 are stringent, primarily focusing on accuracy for the tax year. Issuers need to deliver the form to borrowers by January 31 of the following year to ensure borrowers have sufficient time to prepare their tax returns. Additionally, lenders must file the form with the IRS by the final day of February if filing by mail or by March 31 if filing electronically. These deadlines are designed to maintain a smooth tax reporting process and to minimize the potential for errors or delays.