Definition & Purpose of Form 1098 for 2015

Form 1098, known as the Mortgage Interest Statement, is a critical tax document used by lenders to report mortgage interest of $600 or more received from borrowers in a single tax year. The 2015 version of this form serves the same purpose and is essential for taxpayers who have paid mortgage interest to potentially claim a deduction on their federal income tax returns. The document benefits homeowners by providing the necessary information to reduce their taxable income, resulting in potential tax savings.

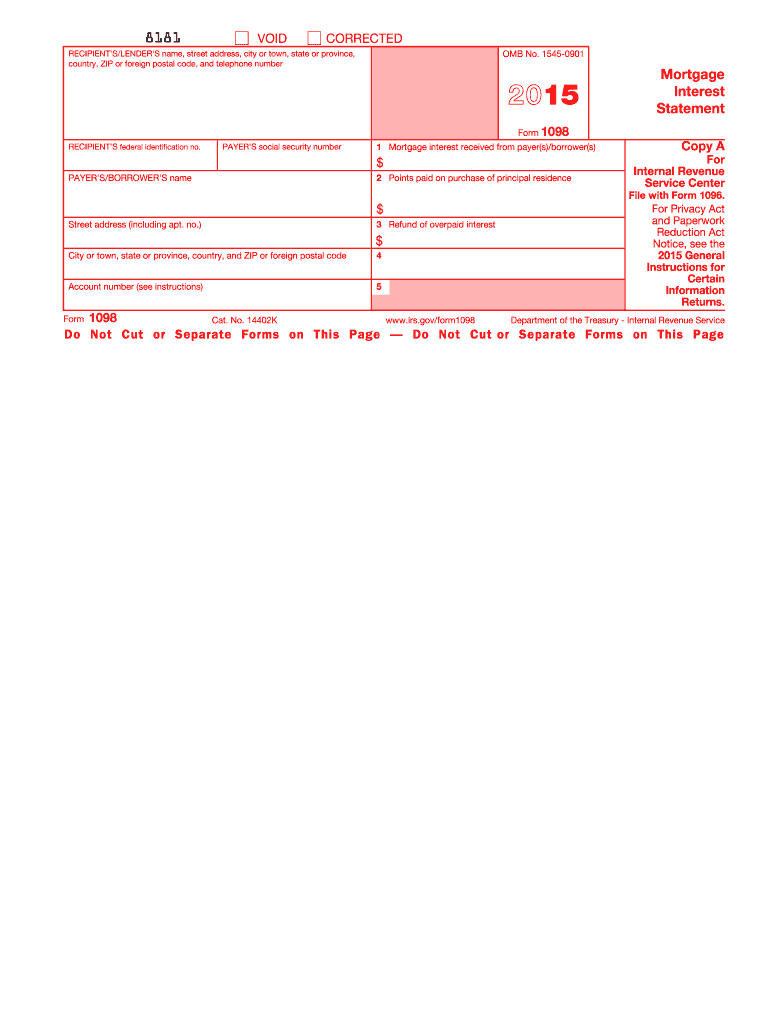

Important Components of Form 1098

The 1098 form includes several key elements that outline the transactions between lenders and borrowers. It details:

- Paying lender's name, address, and taxpayer identification number (TIN).

- Borrower's name, address, and TIN.

- Mortgage interest received from the borrower.

- Points paid on the purchase of the principal residence.

- Mortgage insurance premiums paid. This information is pivotal for both the payer and the recipient to accurately report financial data on their respective tax returns.

Steps to Complete the 1098 Form 2015

Completing Form 1098 for the 2015 tax year requires careful attention to specific sections to ensure accuracy. The process involves:

- Gathering necessary information, including mortgage details and personal identification numbers.

- Filling in the payer and borrower information precisely.

- Recording the total mortgage interest received in the corresponding box.

- Noting any points paid, especially if they are part of a refinancing process.

- Including any pre-paid insurance premiums.

Each step demands accuracy since errors could result in discrepancies that may trigger IRS inquiries or penalties.

How to Obtain the 1098 Form 2015

Receiving the 1098 form is relatively straightforward, as lenders are required to issue it to borrowers by the end of January following the tax year. Borrowers typically get the form by mail or through secure online portals provided by their mortgage companies or banks. For those who have not received their form by the expected date, contacting the lender directly or accessing their online account may provide solutions.

Alternative Access Methods

- Direct Download: Many financial institutions offer downloadable versions from their websites.

- Customer Service: Borrowers can request a mailed copy directly from customer service if the form was not received.

- IRS Resources: Occasionally, the IRS website might have fillable forms available for use. However, these are usually unsigned and intended for information purposes rather than formal submission.

Why You Need to Use Form 1098 for 2015

The primary reason for utilizing the 1098 form in tax calculations is to leverage the mortgage interest deduction. Homeowners who itemize their deductions instead of taking the standard deduction can reduce their taxable income dollar-for-dollar by the amount of qualifying mortgage interest paid during the year.

Benefits of Reporting Mortgage Interest

- Tax Reduction: Lower taxable income results in decreasing overall tax liabilities.

- Accurate Tax Records: Maintaining meticulous financial records with a 1098 form ensures compliance and clarity in tax filings.

- Financial Planning: Understanding annual interest payments can aid homeowners in forecasting future financial commitments and obligations.

Who Typically Uses the 1098 Form 2015

The 1098 form is primarily utilized by individuals and entities paying mortgage interest. The primary users include:

- Homeowners: Those who have financed or refinanced their homes through standard mortgage loans.

- Real Estate Investors: Individuals holding properties for investment purposes also report using the 1098.

- Financial Institutions: Lenders issuing the form are legally mandated to provide this documentation to borrowers and the IRS.

In some instances, borrowers with alternative financing arrangements or who pay significant amounts in mortgage interest without formal documentation may also seek to use the 1098.

IRS Guidelines and Penalties for Non-Compliance

The IRS requires lenders to issue Form 1098 to both the borrower and the IRS, providing a record of mortgage interest transactions. Failure to submit the form or inaccuracies can lead to penalties including:

- Fines for Late Filing: Delays in issuing or filing the form can result in monetary penalties.

- Accuracy Penalties: Incorrect or absent information may lead to fines for negligence or fraud.

Adhering to IRS guidelines minimizes chances of audits and enhances compliance with federal tax laws.

Form Submission Methods: Digital vs. Paper

Form 1098 for 2015 can be submitted through either digital or paper methods depending on the preferences and capabilities of the lender. Electronic filing is encouraged by the IRS for its accuracy and speed advantages. Lenders with numerous forms to submit often opt for this method via IRS-approved electronic filing systems. Paper forms, while still accepted, necessitate additional processing time and may be subject to higher error margins.

Comparisons

- Digital Submission: Faster processing, reduced error rates, and direct acknowledgment from the IRS.

- Paper Submission: Traditional method that may incur delays due to manual handling and postal services. By understanding these options, both lenders and borrowers can align their submissions with available resources for efficiency and compliance.

State-Specific Rules and Variations

While the 1098 form is federally standardized, state-specific regulations may influence the use and reporting of mortgage interest. Several states may have additional reporting requirements or offer specific incentives for utilizing Form 1098 in tax submissions. Understanding these nuances ensures alignment with both federal and state tax obligations, especially for taxpayers who own properties across multiple states.

State Considerations

- Deductions Limits: Some states mirror federal limits while others have different caps.

- Additional Documentation: States may require extra paperwork or validation in certain cases.

- Property Location: Rules may differ for properties held in-state versus out-of-state. Staying informed of these distinctions is crucial for taxpayers to avoid dual reporting errors and capitalize on potential tax benefits.