Definition and Meaning of Form 1098 for 2017

Form 1098, also known as the Mortgage Interest Statement, is issued by lenders to report the amount of mortgage interest received from borrowers during a tax year. For 2017, the form details any mortgage interest paid by individuals, which can be deducted on their tax return under the Home Mortgage Interest Deduction. This form is critical for taxpayers, as it helps reduce taxable income, potentially lowering their overall tax liability. Understanding the components of Form 1098 is essential for accurate tax reporting and financial planning.

How to Use Form 1098 for 2017

Utilizing Form 1098 for the 2017 tax year involves accurately reporting mortgage interest to take advantage of potential deductions. Taxpayers should cross-reference the information reported on the form with their own records to ensure accuracy. The mortgage interest reported by lenders is typically entered on Schedule A of the individual’s tax return if itemizing deductions. Importantly, Form 1098 should be retained as part of one’s tax documentation, as it serves as proof of the claimed deduction in case of an audit by the IRS.

How to Obtain Form 1098 for 2017

Taxpayers can obtain Form 1098 for 2017 through their mortgage lender or servicer, who are responsible for providing these forms by January 31 of the following year. Most lenders send out forms either by mail or electronically, if the borrower has opted for digital delivery. It is advisable to contact the lender’s customer service if the form has not been received by mid-February. Additionally, some online banking services may provide downloadable versions of Form 1098 through their platforms.

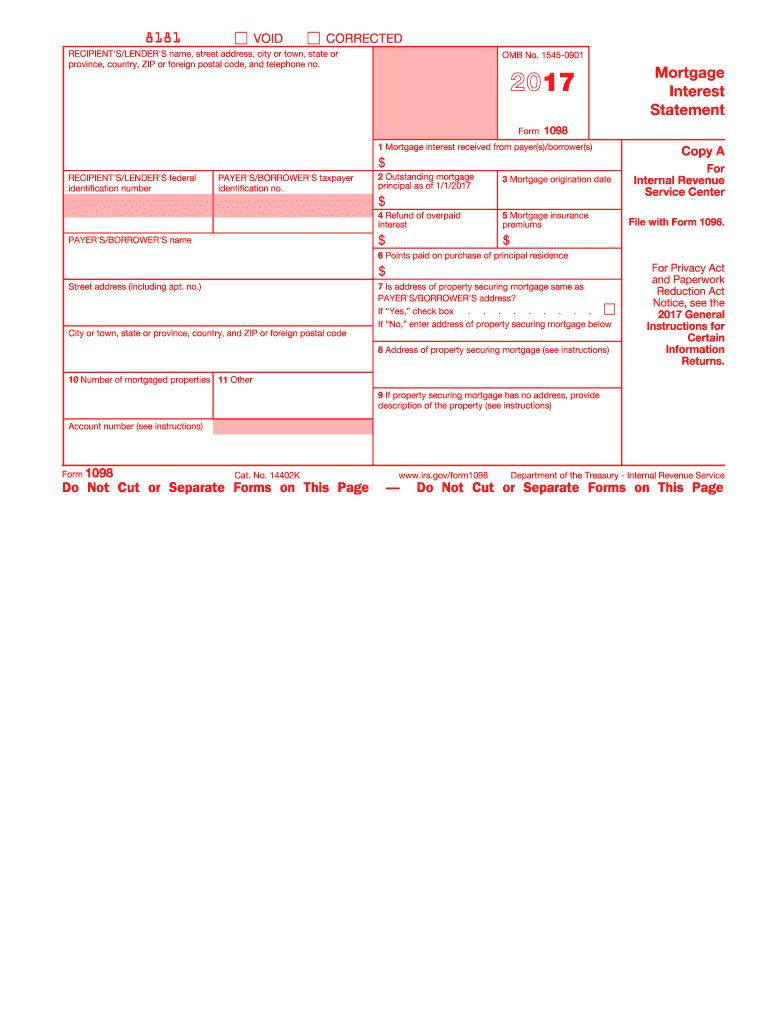

Steps to Complete Form 1098 for 2017

Though borrowers receive Form 1098 completed by their lenders, understanding the entries is crucial. Lenders must fill in several key fields:

- Box 1: Reports the total mortgage interest received during 2017.

- Box 2: Potentially includes the outstanding mortgage principal as of January 1, 2017.

- Box 3: Reflects the date of the mortgage origination.

- Box 5: Provides the number of properties securing the mortgage.

- Additional boxes may include points paid on the purchase of the home, if applicable.

Borrowers should verify the accuracy of these entries against their own payments and records.

Filing Deadlines and Important Dates for 2017

The deadline for lenders to send Form 1098 to borrowers is January 31, 2018. Borrowers should aim to have their tax filings completed by the April 15, 2018 deadline if aiming to claim deductions for mortgage interest. Maintaining clear records and ensuring the receipt of Form 1098 ahead of these deadlines helps avoid last-minute complications.

Key Elements of Form 1098 for 2017

Critical fields in the 2017 Form 1098 include:

- Mortgage Interest Received: Central to determining deduction eligibility.

- Outstanding Mortgage Principal: Useful for confirming loan balances.

- Mortgage Origination Date: Helps verify the length of mortgage payments.

- Points Paid: Potentially deductible if used to lower the loan's interest rate.

Understanding these elements ensures that taxpayers fully leverage available deductions and maintain accuracy in their tax reporting.

IRS Guidelines for Form 1098

The IRS provides specific guidelines for the reporting of mortgage interest on Form 1098. Lenders must furnish this form for any individual from whom $600 or more in mortgage interest was received during the tax year. Adherence to IRS guidelines ensures compliance with federal tax regulations and helps avoid penalties for misreporting or underreporting.

Penalties for Non-Compliance with Form 1098

Failing to properly report or file Form 1098 for 2017 can lead to penalties from the IRS. Lenders who neglect to issue proper documentation are subject to fines for non-compliance. Likewise, individuals who misreport mortgage interest or fail to include it in their tax filings may face penalties and interest charges on any underpaid tax amount. Accurate filing ensures compliance and aids in the avoidance of these potential repercussions.

Eligibility Criteria for Using Form 1098 for 2017

Eligibility to receive or use Form 1098 primarily depends on being an individual who has paid mortgage interest to a lender. The form is applicable to most homeowners with mortgage agreements and interest payments meeting or exceeding $600 in a tax year. Understanding eligibility is vital for determining whether deductions via Form 1098 can be leveraged in tax filings.

Variants and Alternatives to Form 1098 for 2017

While the Form 1098 is central to mortgage interest reporting, there may be other variations or related forms used in different contexts, such as Form 1099 for reporting other income types or Form 1098-T for education-related expenses. These forms serve various purposes, but only Form 1098 directly relates to mortgage interest and related deductions for tax purposes during 2017. Understanding these distinctions ensures the accurate application of tax forms related to specific income and deduction types.