Introduction to 1996 Form 709

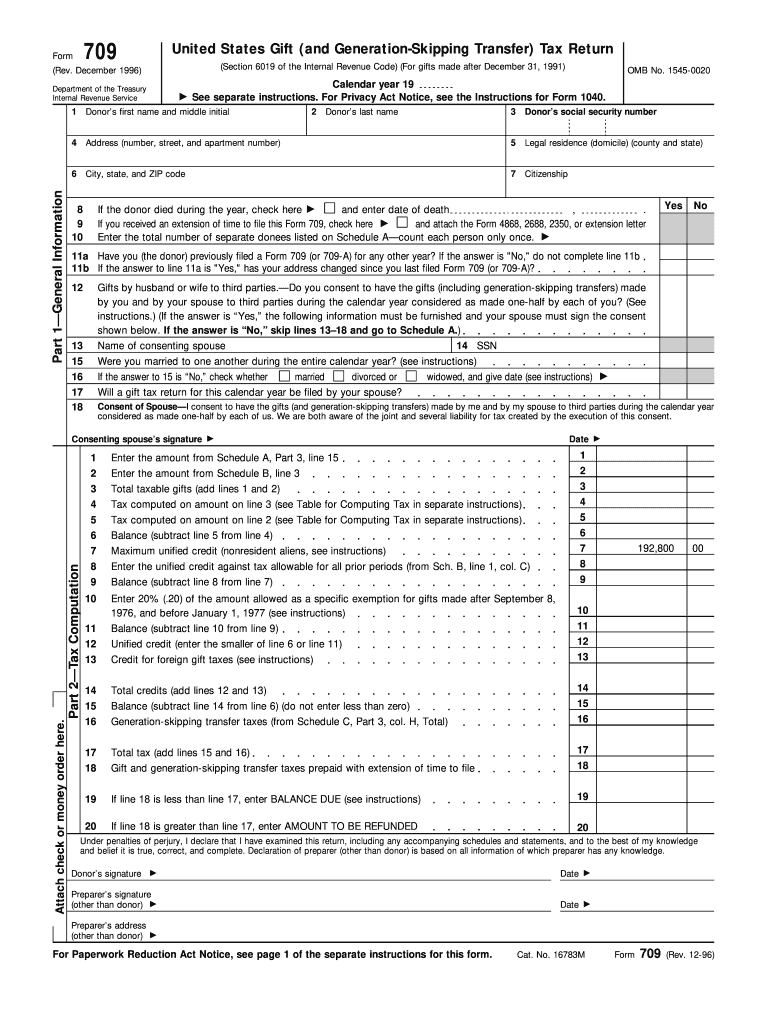

1996 Form 709 is crucial for documenting the giving of gifts and handling Generation-Skipping Transfer (GST) taxes in the United States. This form is officially known as the United States Gift (and Generation-Skipping Transfer) Tax Return. Individuals who have made significant gifts after December 31, 1991, typically need to fill out this form for proper reporting to the IRS. It covers specific sections such as the donor's information, details of gifts given, and tax computations related to taxable gifts.

How to Use the 1996 Form 709

To effectively use the 1996 Form 709, it is necessary to gather detailed information regarding any gifts that have been made throughout the year. The form requires documentation about the recipients (donees), the value of the gifted assets, and applicable deductions or credits. Accurately filling out each section ensures compliance with IRS guidelines and helps in tax computations for any applicable gift or GST taxes.

Step-by-Step Process

- Collect Donor Information: Begin by entering details such as name, address, and Social Security Number. This establishes the foundation of the filing.

- Document Gift Details: List out each gift's description, value, and the transferred date to ensure complete transparency.

- Compute Taxable Gifts: Calculate the total value of gifts that are subject to taxation after considering exclusions and deductions.

- GST Tax Consideration: If applicable, record details of any GST taxes incurred alongside the gifted items and assign appropriate tax rates and credits.

- Finalize and Review: Double-check all details, ensuring accuracy throughout before submitting the form.

How to Obtain the 1996 Form 709

The 1996 Form 709 can be accessed through various means such as direct download from the IRS website, requesting a copy via mail, or obtaining it physically from an IRS office. Securing this form through reliable methods ensures you have the correct version that aligns with legal regulations for the specific year.

Important Terms Related to 1996 Form 709

Donor

- The individual who gives the gift and must fill out the form to document the transaction.

Donee

- The recipient of the gift, whose details are integral for providing necessary insights into the gift transfer.

Unified Credit

- A significant factor in gift taxation that limits the donor's obligation to pay taxes on gifts, reducing taxable amounts based on predefined thresholds.

Filing Deadlines and Important Dates

The deadline to file the 1996 Form 709 aligns with the annual tax return due date, which typically falls on April 15th of the following year. Filing extensions are available upon request, although they require adherence to specified procedures and limits. Timely submission of this form helps to avert potential penalties or complications.

Key Elements of the 1996 Form 709

Several critical components make up the 1996 Form 709, each demanding attention for accurate completion:

- Donor Identification: Essential to establish the identity of the individual gifting the assets.

- Gift Details: Full disclosure of each gift's nature and value.

- Exclusions and Deductions: Areas where permissible reductions in taxable amounts are applied.

- Tax Computations: Sections designating how gift taxes are calculated based on reported information and current IRS tax rates.

- Signature and Authentication: Final section where the donor confirms the accuracy of reported information.

Legal Use of the 1996 Form 709

The legal framework surrounding the 1996 Form 709 involves strictly adhering to federal tax regulations regarding gift reporting and payment of applicable taxes. Utilization of the form must comply with IRS standards to prevent any legal infringement or penalties. Proper use guarantees the taxpayer meets all federal guidelines and avoids missteps that could lead to audits or legal consequences.

Examples of Using the 1996 Form 709

Case Study Scenarios

- Individuals Giving Large Monetary Gifts: Donors who transferred money exceeding per-year exclusions must use the form to document the details.

- Inheritance and Estate Planning: Cases where gifts form a part of early inheritance strategies necessitate the use of this form to address possible gift and GST taxes.

- Parental Gifts to Children: Parents providing substantial gifts to children for education or property purchase must account for these transfers fiscally.

IRS Guidelines for Form 709

Adhering to IRS guidelines is crucial for the successful completion and submission of Form 709. These guidelines dictate how to calculate exclusions, apply the unified credit, and document gifts accurately to ensure compliance. The IRS provides comprehensive instructions for filling out the form, thereby reducing potential errors and facilitating accurate tax reporting.

Penalties for Non-Compliance

Failure to file Form 709 when required can lead to substantial penalties, including fines and interest on owed taxes. Misreporting or underreporting the amounts can result in legal scrutiny and additional charges. Maintaining adherence to submission guidelines helps in mitigating risks of legal issues or financial repercussions from the IRS.