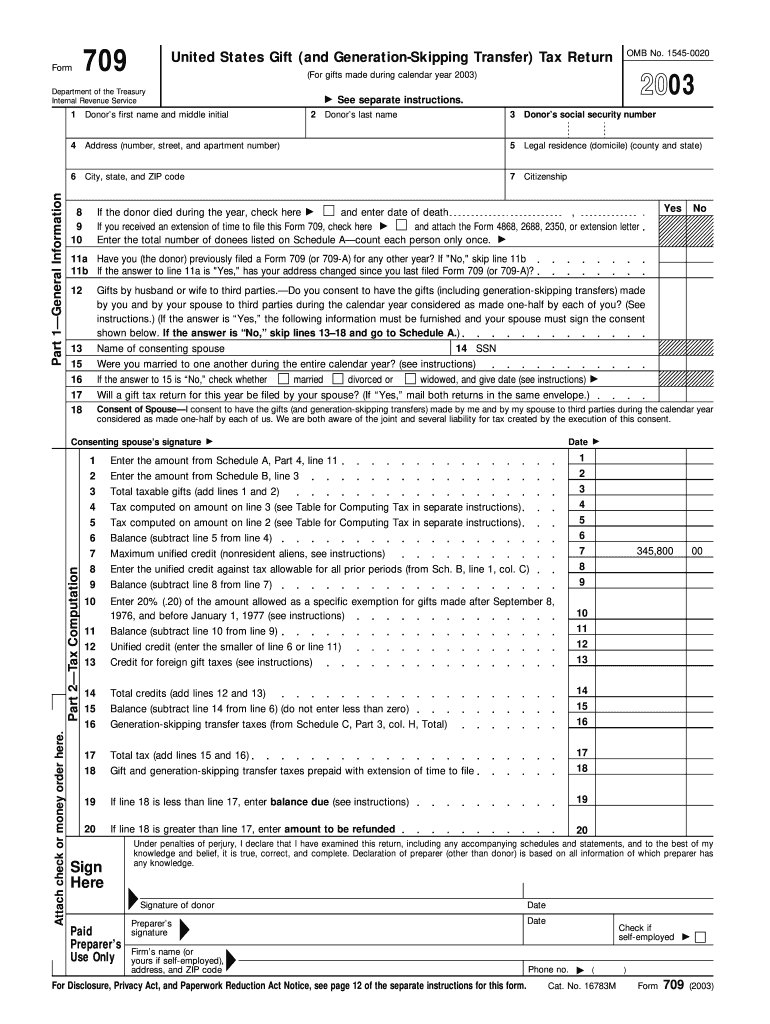

Definition and Purpose of the 2003 Form 709

The 2003 Form 709 is the United States Gift (and Generation-Skipping Transfer) Tax Return. It is used by individuals who have made gifts during the year to report these transfers and calculate any applicable gift taxes. This form also allows donors to claim deductions or credits related to their gifts. The information recorded includes general details about the donor, specifics regarding the amounts gifted, computations for the assessed tax, and schedules for taxable and generation-skipping transfers. Understanding its purpose is essential for ensuring compliance with U.S. tax laws, especially for taxpayers making significant or numerous gifts.

Who Typically Uses the 2003 Form 709

Typically, the 2003 Form 709 is used by individuals in the U.S. who have gifted more than the federal annual exclusion amount in a calendar year. These individuals may include:

- Wealthy individuals who engage in estate planning.

- Parents gifting sums to children that exceed exclusion limits.

- Business owners transferring significant shares of business interests.

- Grandparents who skip generations in their bequests.

By properly filing Form 709, these taxpayers can ensure transparency in their financial transactions and adherence to tax obligations.

How to Obtain the 2003 Form 709

Form 709 for the year 2003 can be obtained through several methods:

- IRS Website: Forms from previous years, including 2003, are often available on the IRS website under historical forms.

- Tax Software: Many tax preparation software offers the capability to download historical forms as part of their service package.

- Professional Tax Advisors: Accountants or tax attorneys can often provide needed forms and assist with filing.

These resources ensure accessibility for those who need to file past years' returns or review historical forms for educational purposes.

Steps to Complete the 2003 Form 709

Completing the 2003 Form 709 involves a series of detailed steps focused on accurate data entry and calculation:

- Enter Personal Information: Begin by supplying the donor's personal identification details.

- List Gifts Made: Input specifics about each gift exceeding the annual exclusion amount.

- Perform Tax Calculations: Calculate any gift taxes owed by referencing provided IRS schedules.

- Complete Schedules: Fill out additional schedules for taxable gifts and generation-skipping transfers.

- Review and Double-Check: Ensure all information is accurate and check the forms for omissions.

- Submit: File the completed form with the IRS, either electronically or via mail, depending on personal preference or advisement.

Legal Use of the 2003 Form 709

Form 709 is legally required for reporting gifts exceeding annual exclusions to avoid or minimize estate tax liabilities. It’s regarded as a legal document that substantiates:

- The donor’s intent and amount of gifts.

- Tax calculations in line with IRS rules.

- Any applicable generation-skipping transfer taxes.

Misreporting or failing to file can result in penalties, making legal compliance crucial.

Key Elements of the 2003 Form 709

Several key elements comprise the 2003 Form 709, ensuring comprehensive reporting:

- Donor Information: Includes name, Social Security number, and address.

- Summary of Gifts: A detailed account of each gift value exceeding the exclusion threshold.

- Tax Calculations: Sections dedicated to calculating any owed taxes based on aggregated gift values.

- Schedules: Additional schedules for detailed information on taxable gifts and any generation-skipping transfers.

Proper completion of these elements is necessary for legally valid and complete tax return documentation.

Filing Deadlines for the 2003 Form 709

The due date for the 2003 Form 709 was typically April 15, 2004, coinciding with the individual tax return deadline. If extended filing was necessary, the deadline moved to October of the same year. Missing these crucial deadlines could result in financial penalties or interest charges, emphasizing the importance of timely compliance.

Examples of Using the 2003 Form 709

Practical examples of when to use Form 709 include:

- A parent gifting their adult child $50,000 to buy a home—exceeding the annual exclusion.

- A business owner transferring a significant portion of company shares to a non-spouse family member.

- Grandparents providing funds directly to grandchildren's education funds, surpassing exclusion limits.

Each scenario requires documentation to ensure compliance and transparency with federal tax regulations.